Ingenico Elite 510, Elite 730, Elite 770, Elite 780, 510 Supplementary Manual

THE VALUE OF OPEN

BANKCARD PROCESSING

Introducing the merchant bankcard industry to the value of an

open bankcard processing environment.

INTRODUCTION 2

THE MERCHANT BANKCARD INDUSTRY TODAY 3

MARKET TRENDS 3

TECHNOLOGY TRENDS 3

WHY AN OPEN BANKCARD PROCESSING ENVIRONMENT

IS NEEDED 4

COMPONENTS OF AN OPEN BANKCARD PROCESSING

ENVIRONMENT 5

PAYMENT AND WEB-ENABLED TERMINALS 5

IN-STORE TRANSACTION PAYMENT AND VALUE-ADDED

SERVICES 6

AN INDUSTRY STANDARD NETWORK USING PROTOCOLS

SUCH AS TCP/IP 6

THE NEED FOR HIGH SPEED COMMUNICATIONS 7

SUPPORTING THE HOST-LEVEL TRANSACTION AUTHORIZATION,

SETTLEMENT,VALUE-ADDED SERVICES AND FINANCIAL

SERVICES OF PROCESSORS AND FINANCIAL INSTITUTIONS 7

NETWORK SERVICES 8

TERMINAL ASSET MANAGEMENT 8

RECEIPT, SIGNATURE AND IMAGE MANAGEMENT 9

LOYALTY AND GIFT CARDS 9

TOUCH SCREEN AND WEB-BASED TECHNOLOGY 10

PAYMENT AND VALUE-ADDED CUSTOMER SERVICES 10

WHY TOUCH SCREEN TECHNOLOGY 11

AN INTUITIVE USER INTERFACE 11

REDUCES HELP DESK COSTS 11

REDUCES COST OF SALES 11

WEB-BASED THIN CLIENT TECHNOLOGY 12

WHY USE THIN CLIENT TECHNOLOGY 12

A DEVELOPMENT ENVIRONMENT TO SUPPORT AN OPEN

BANKCARD PROCESSING ENVIRONMENT 12

DEVELOPMENT ENVIRONMENT COMPONENTS 12

DEVELOPMENT ENVIRONMENT ATTRIBUTES 13

DEVELOPMENT ENVIRONMENT BENEFITS 13

EMV 13

WHY IS A SMART CARD STANDARD NEEDED? 14

INGENICO IS THE LEADER IN EMV APPROVALS 15

ABOUT INGENICO 16

THE INGENICO VALUE PROPOSITION 16

THE VALUE OF OPEN BANKCARD PROCESSING

Introducing the merchant bankcard industry to the value of an open

bankcard processing environment

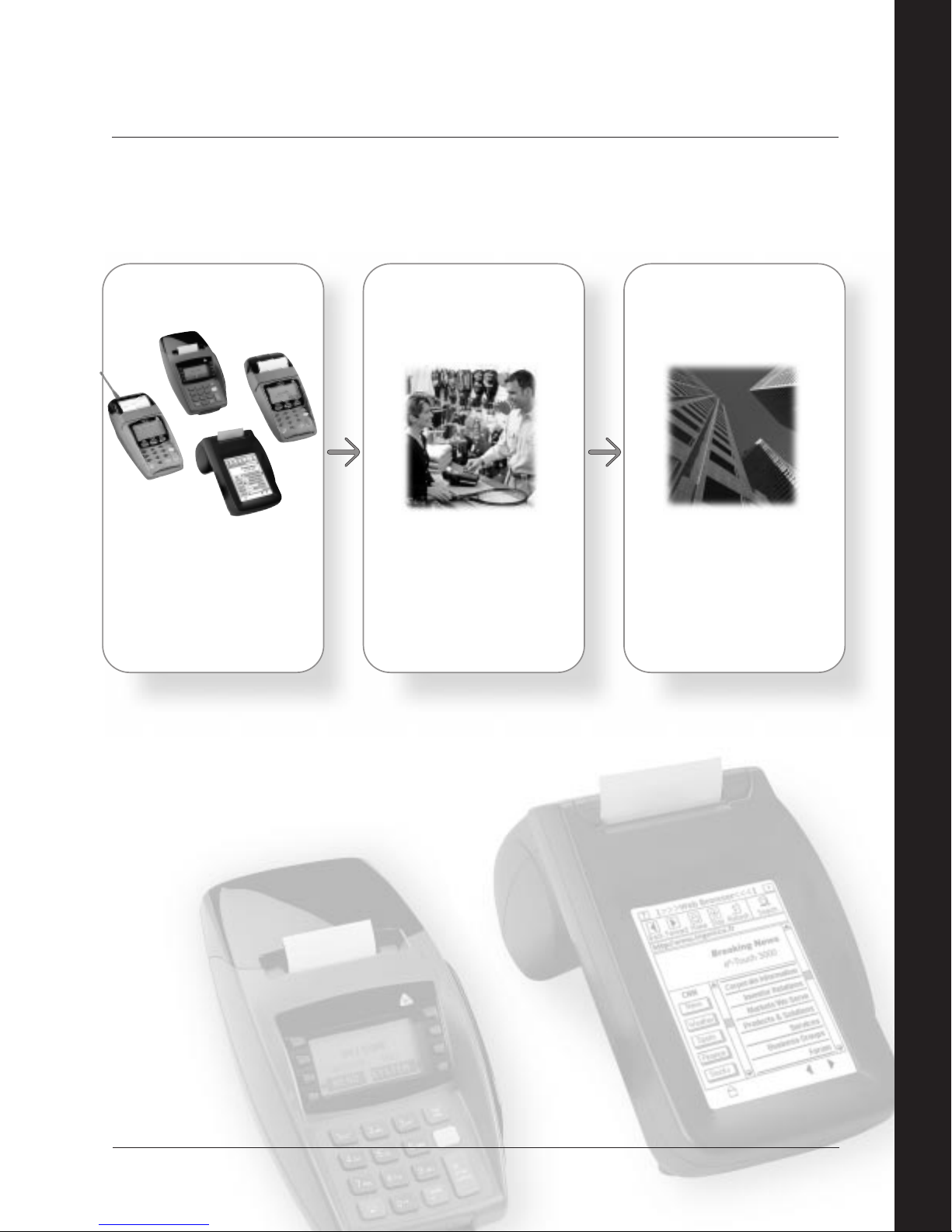

1.

Payment & web-enabled

terminals and readers

In-store payment

transaction management

and value-added services

delivery

➥

Thin Client technology

➥

Application portability

➥

Core application

➥

Secure multi-application support

➥

Comprehensive development

environment

➥

Open platform

➥

Debit card conversion

➥

Check conversion

➥

Loyalty and gift cards

➥

Network services and tools

➥

Terminal asset management

➥

Loyalty and gift cards

➥

Receipt, signature and image

management

CREDIT

DEBIT

CHECK

EBT

ACH

INGENICO

We are applying our leadership in secure transaction technology, open

systems, connectivity, multi-application support, multi-lane payment technology

and value-added services to provide proven and robust solutions for the

merchant bankcard industry. We deliver the systems you need today while

positioning for tomorrow’s trends and technologies.

Supporting the transaction

authorization, settlement,

value-added service and

financial service offerings

of our customers

INTRODUCTION

This paper introduces the merchant bankcard

industry to the attributes and value of an open

bankcard processing environment. An open

bankcard processing environment provides

significant benefits to financial institutions,

processors, ISOs and merchants:

• Lowers processor, financial institution and ISO

support and operational costs by standardizing

EFT POS terminal application support and

development.

• Provides the ability to seamlessly integrate new

payment types and terminal technologies into

your merchant terminal offerings.

• Provides the ability to leverage existing

solutions to open new market opportunities for

enterprising processors, financial institutions

and ISOs.

• Provides the ability to introduce and effectively

market value-added solutions to your merchant

base that drive incremental revenue and

customer loyalty for the merchant and recurring

revenue to you.

• Supports and enhances the payment function

at the point of service – faster customer

service, improved ease of use, security and

management of the terminal asset.

This paper presents the components of an

open bankcard processing environment while

also discussing how touch screen, TCP/IP and thin

client technologies can provide added benefit to

financial institutions, processors, ISOs and

merchants. It is brought to you by the leader in

secure transaction solutions, Ingenico.

INGENICO

2.

3.

THE MERCHANT BANKCARD

INDUSTRY TODAY

Market Trends

• Small merchants have the same requirements as

large merchants – the need to operate efficiently,

the need to serve customers quickly, the need to

lower the cost of payment and the need to avoid

fraud.

• Small merchants need customer relationship

management tools to effectively compete against

other small merchants as well as the large

national retail chains.

• Merchant attrition is a tremendous issue for

financial institutions, processors and ISOs.

Retailers have been “conditioned” to look for

the best price and trouble free service. When a

provider fails to give trouble free service, the

retailer will switch networks very quickly. As a

result, financial institutions and processors lack

the ability to differentiate themselves with other

than price and “issue avoidance”.

• Price competition is the primary means of

winning new business, however, pricing is never

a sustainable competitive advantage.

• Processors, financial institutions and ISOs lack

the means to keep in frequent contact with their

merchant customers.

• The primary objective of an EFT POS terminal is

to support the payment process – anything that

delineates from serving the customer will not be

accepted by merchants or those whom directly

support the merchant. However, value-added

services such as messaging, frequency, electronic

gift certificates that complement the payment

processor are positioned for market success.

• Retailers are looking towards their payment

processing provider to update technology for

payment, settlement, and reporting. This includes

Internet access for transaction histories, chargeback requests and other information that a

retailer would like “on demand”.

• Retailers are beginning to request a single image,

regardless of whether the customer shops online

or in the store - integration of the store front and

web based commerce is key.

Technology Trends

• Retailers with integrated payment are slowly

migrating to open systems and industry

standard components such as are used by cell

phones, pagers, palm pilots, ECRs and PCs.

This will lead to adoption of open systems and

industry standards by smaller merchants with

dial payment.

• Proprietary programming languages and

development platforms are giving way to open

environments for EFT POS terminals.

• Smart cards are soon going to make an impact in

our industry – not for stored value as previously

marketed – but for credit and debit transactions

as well as value-added services such as electronic

gift certificate, loyalty and frequency.

• Terminal manufacturers will need to update their

EFT POS terminal offerings to include EMV

approvals if they are going to do business in the

next few years. The leading card associations

will require EMV level I and II approval.

• Terminal manufacturers are examining

technologies such as Bluetooth, USB, touch

screen and TCP/IP – these technologies will

enable processors to implement exciting new

and innovative solutions that help ISOs,

processors and financial institutions churn

the market.

• Processors are going to begin updating

their networks from 1200 and 2400 bps

communication speeds and move away from

outdated protocols to “PC like” speeds and

implement connectivity through DSL and

cable modems.

• Processors will update their communication’s

infrastructure to leverage the power and

capabilities of the Internet in a controlled and

orderly manner that adds value to their merchant

relationship and supports the payment function.

INGENICO

4.

WHY AN OPEN BANKCARD

PROCESSING ENVIRONMENT

IS NEEDED

• An open bankcard processing environment

is built upon open systems and industry

standard components, allowing it to be

upgraded and enhanced without concern for

proprietary and legacy elements. This also

reduces the operational and investment costs

for those providing network services.

• An open bankcard processing environment

positions financial institutions and processors

for today’s and tomorrow’s payments, making

it much easier to implement emerging

tender types.

• An open bankcard processing environment

allows the user to quickly introduce new

services and products or to quickly enhance

existing ones with new features.

• An open bankcard processing environment

positions financial institutions and processors

to seamlessly support multiple vendor

terminals.

• An open bankcard processing environment

allows manufacturers to quickly adapt

technology that has been proven in other

industries.

• An open bankcard processing environment

is simpler to implement, operate and support

than a proprietary network.

• Industry standard technologies lower a

manufacturer’s cost of bringing product to

market while ensuring the ability to upgrade

their systems later as new features are made

available.

• Industry standard technologies and open

development platforms enable processors,

financial institutions and ISOs to apply EFT POS

solutions to other markets that have similar

needs, thus opening new markets and revenue

opportunities.

• An open bankcard processing environment

provides ISOs, processor and financial

institutions with the ability to differentiate

themselves by leveraging industry standard

development systems and tools to enhance

their systems and services.

Open Platforms

Open Platforms is a committee that is part of

GlobalPlatforms and STIP consortiums. The group’s charter is

to develop standards for applications that are interoperatable

between EFT POS terminals, cell phones, PDA, vending machine

card readers and any other device in which a transaction occurs.

Ingenico chairs this committee.

Loading...

Loading...