Financial Derivatives

Toolbox

For Use with MATLAB

Computation

Visualization

®

User’s Guide

Version 2

Programming

How to Contact The MathWorks:

www.mathworks.com Web

comp.soft-sys.matlab Newsgroup

support@mathworks.com Technical support

suggest@mathworks.com Product enhancement suggestions

bugs@mathworks.com Bug reports

doc@mathworks.com Documentation error reports

service@mathworks.com Order status, license renewals, passcodes

info@mathworks.com Sales, pricing, and general information

508-647-7000 Phone

508-647-7001 Fax

The MathWorks, Inc. Mail

3 Apple Hill Drive

Natick, MA 01760-2098

For contact information about worldwide offices, see the MathWorks Web site.

Financial Derivatives Toolbox User’s Guide

COPYRIGHT 2000 - 2001 by The MathWorks, Inc.

The software described in this document is furnished under a license agreement. The software may be used

or copied only under the terms of the license agreement. No part of this manual may be photocopied or reproduced in any form without prior written consent from The MathWorks, Inc.

FEDERAL ACQUISITION: This provision applies to all acquisitions of the Program and Documentation by

or for the federal government of the United States. By accepting delivery of the Program, the government

hereby agrees that this software qualifies as "commercial" computer software within the meaning of FAR

Part 12.212, DFARS Part 227.7202-1, DFARS Part 227.7202-3, DFARS Part 252.227-7013, and DFARS Part

252.227-7014. The terms and conditions of The MathWorks, Inc. Software License Agreement shall pertain

to the government’s use and disclosure of the Program and Documentation, and shall supersede any

conflicting contractual terms or conditions. If this license fails to meet the government’s minimum needs or

is inconsistent in any respect with federal procurement law, the government agrees to return the Program

and Documentation, unused, to MathWorks.

MATLAB, Simulink, Stateflow, Handle Graphics, and Real-Time Workshop are registered trademarks, and

Target Language Compiler is a trademark of The MathWorks, Inc.

Other product or brand names are trademarks or registered trademarks of their respective holders.

Printing History: June 2000 First printing New for Version 1 (Release 12)

Sept. 2001 Second printing Updated for Version 2 (Release 12.1)

Preface

About This Book . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . x

Organization of the Document . . . . . . . . . . . . . . . . . . . . . . . . . . . . x

Typographical Conventions . . . . . . . . . . . . . . . . . . . . . . . . . . . . xi

Related Products . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xii

Background Reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xiv

Black-Derman-Toy (BDT) Modeling . . . . . . . . . . . . . . . . . . . . . . xiv

Heath-Jarrow-Morton (HJM) Modeling . . . . . . . . . . . . . . . . . . . xiv

Financial Derivatives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xiv

Contents

Getting Started

1

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-2

Interest Rate Models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-2

Trees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-2

Financial Instruments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-4

Hedging . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-5

Creating and Managing Instrument Portfolios . . . . . . . . . . 1-6

Portfolio Creation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-6

Portfolio Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-9

i

Using Financial Derivatives

2

Interest Rate Environment . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2-3

Interest Rates vs. Discount Factors . . . . . . . . . . . . . . . . . . . . . . 2-3

Interest Rate Term Conversions . . . . . . . . . . . . . . . . . . . . . . . . . 2-8

Interest Rate Term Structure . . . . . . . . . . . . . . . . . . . . . . . . . . 2-12

Pricing and Sensitivity from

Interest Rate Term Structure . . . . . . . . . . . . . . . . . . . . . . . . .

Pricing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2-18

Sensitivity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2-20

Heath-Jarrow-Morton (HJM) Model . . . . . . . . . . . . . . . . . . . 2-22

Building an HJM Forward Rate Tree . . . . . . . . . . . . . . . . . . . . 2-22

Using HJM Trees in MATLAB . . . . . . . . . . . . . . . . . . . . . . . . . 2-28

Pricing and Sensitivity from HJM . . . . . . . . . . . . . . . . . . . . . 2-35

Pricing and the Price Tree . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2-35

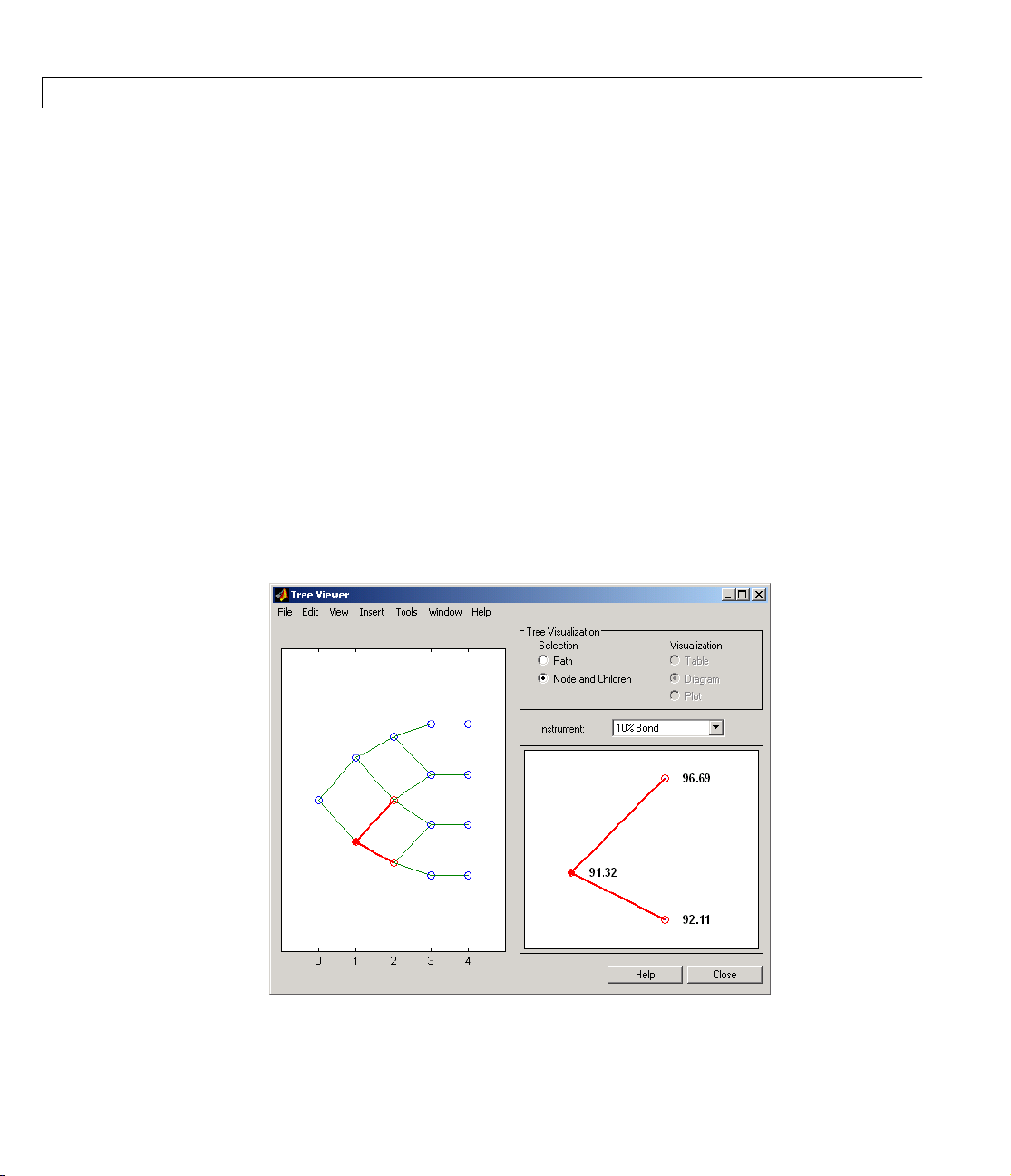

Using treeviewer to View Instrument Prices Through Time . 2-40

HJM Pricing Options Structure . . . . . . . . . . . . . . . . . . . . . . . . 2-44

Calculating Prices and Sensitivities . . . . . . . . . . . . . . . . . . . . . 2-50

2-17

ii Contents

Black-Derman-Toy Model (BDT) . . . . . . . . . . . . . . . . . . . . . . . 2-53

Building a BDT Interest Rate Tree . . . . . . . . . . . . . . . . . . . . . . 2-53

Using BDT Trees in MATLAB . . . . . . . . . . . . . . . . . . . . . . . . . 2-58

Pricing and Sensitivity from BDT . . . . . . . . . . . . . . . . . . . . . 2-63

Pricing and the Price Tree . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2-63

BDT Pricing Options Structure . . . . . . . . . . . . . . . . . . . . . . . . . 2-71

Calculating Prices and Sensitivities . . . . . . . . . . . . . . . . . . . . . 2-71

Hedging Portfolios

3

Hedging . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-2

Hedging Functions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-3

Hedging with hedgeopt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-3

Self-Financing Hedges (hedgeslf) . . . . . . . . . . . . . . . . . . . . . . 3-12

Specifying Constraints with ConSet . . . . . . . . . . . . . . . . . . . 3-16

Setting Constraints . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-16

Portfolio Rebalancing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3-18

Hedging with Constrained Portfolios . . . . . . . . . . . . . . . . . . 3-21

Example: Fully Hedged Portfolio . . . . . . . . . . . . . . . . . . . . . . . 3-21

Example: Minimize Portfolio Sensitivities . . . . . . . . . . . . . . . . 3-23

Example: Under-Determined System . . . . . . . . . . . . . . . . . . . . 3-25

Portfolio Constraints with hedgeslf . . . . . . . . . . . . . . . . . . . . . 3-26

Function Reference

4

Functions by Category . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-2

Alphabetical List of Functions

bdtprice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

bdtsens . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-12

bdttimespec . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-15

bdttree . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-17

bdtvolspec . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-19

bondbybdt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-20

bondbyhjm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-23

bondbyzero . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-26

bushpath . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-29

bushshape . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-31

capbybdt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-34

4-9

iii

capbyhjm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-37

cfbybdt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-39

cfbyhjm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-41

cfbyzero . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-43

classfin . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-45

date2time . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-47

datedisp . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-49

derivget . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-50

derivset . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-51

disc2rate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-53

fixedbybdt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-55

fixedbyhjm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-57

fixedbyzero . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-59

floatbybdt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-61

floatbyhjm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-63

floatbyzero . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-65

floorbybdt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-67

floorbyhjm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-70

hedgeopt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-72

hedgeslf . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-75

hjmprice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-79

hjmsens . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-82

hjmtimespec . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-85

hjmtree . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-87

hjmvolspec . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-89

instadd . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-92

instaddfield . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-94

instbond . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-98

instcap . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-100

instcf . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-102

instdelete . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-104

instdisp . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-106

instfields . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-108

instfind . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-111

instfixed . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-114

instfloat . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-116

instfloor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-118

instget . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-120

instgetcell . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-124

instlength . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-129

iv Contents

instoptbnd . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-130

instselect . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-132

instsetfield . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-135

instswap . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-139

insttypes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-141

intenvget . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-143

intenvprice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-145

intenvsens . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-147

intenvset . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-149

isafin . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-153

mkbush . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-154

mktree . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-156

mmktbybdt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-157

mmktbyhjm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-158

optbndbybdt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-159

optbndbyhjm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-163

rate2disc . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-166

ratetimes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-170

swapbybdt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-174

swapbyhjm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-179

swapbyzero . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-184

treepath . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-187

treeshape . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-189

treeviewer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-191

A

Glossary

v

vi Contents

Preface

About This Book . . . . . . . . . . . . . . . . . . . x

Organization of the Document . . . . . . . . . . . . . . x

Typographical Conventions . . . . . . . . . . . . . . xi

Related Products . . . . . . . . . . . . . . . . . . .xii

Background Reading . . . . . . . . . . . . . . . . xiv

Black-Derman-Toy (BDT) Modeling . . . . . . . . . . . xiv

Heath-Jarrow-Morton (HJM) Modeling . . . . . . . . . . xiv

Financial Derivatives . . . . . . . . . . . . . . . . . xiv

Preface

About This Book

This book describes the Financial Derivatives Toolbox for MATLAB, a

collection of tools for analyzing individual financial derivative instruments and

portfolios of instruments.

Organization of the Document

Chapter Description

“Getting Started” Describes interest rate models, bushy and

recombinent trees, instrument types, and

instrument portfolio construction.

“Using Financial

Derivatives”

“Hedging Portfolios” Describes functions that minimize the cost of

“Function

Reference”

Describes techniques for computing prices and

sensitivities based upon the interest rate term

structure, the Heath-Jarrow-Morton (HJM) model

of forward rates, and the Black-Derman-Toy (BDT)

interest rate model.

hedging a portfolio given a set of target

sensitivities, or minimize portfolio sensitivities for

a given set of maximum target costs.

Describes the functions used for interest rate

environment computations, instrument portfolio

construction and manipulation, and for

Heath-Jarrow-Morton and Black-Derman-Toy

modeling.

x

Typographical Conventions

Typographical Conventions

This manual uses some or all of these conventions.

Item Convention Used Example

Example code Monospace font To assign the value 5 to A,

enter

A = 5

Function names/syntax Monospace font The cos function finds the

cosine of each array element.

Syntax line example is

MLGetVar ML_var_name

Keys Boldface with an initial capital

Press the Enter key.

letter

Literal strings (in syntax

Monospace bold for literals

f = freqspace(n,'whole')

descriptions in reference

chapters)

Mathematical

expressions

MATLAB output

Menu titles, menu items,

dialog boxes, and controls

Italics for variables

Standard text font for functions,

operators, and constants

Monospace font MATLAB responds with

Boldface with an initial capital

letter

This vector represents the

polynomial

2

p = x

+ 2x + 3

A =

5

Choose the File menu.

New terms Italics An array is an ordered

collection of information.

Omitted input arguments (...) ellipsis denotes all of the

[c,ia,ib] = union(...)

input/output arguments from

preceding syntaxes.

String variables (from a

Monospace italics sysc = d2c(sysd,'method')

finite list)

xi

Preface

Related Products

The MathWorks provides several products relevant to the tasks you can

perform with the Financial Derivatives Toolbox.

For more information about any of these products, see either:

• The online documentation for that product, if it is installed or if you are

reading the documentation from the CD

• The MathWorks Web site, at

section.

Note The toolboxes listed below all include functions that extend the

capabilities of MATLAB.

Product Description

http://www.mathworks.com; see the “products”

xii

Database Toolbox Tool for connecting to, and interacting with,

most ODBC/JDBC databases from within

MATLAB

Datafeed Toolbox MATLAB functions for integrating the

numerical, computational, and graphical

capabilities of MATLAB with financial data

providers

Excel Link Tool that integrates MATLAB capabilities with

Microsoft Excel for Windows

Financial Time Series

Toolbox

Financial Toolbox MATLAB functions for quantitative financial

Tool for analyzing time series data in the

financial markets

modeling and analytic prototyping

Related Products

Product Description

GARCH Toolbox MATLAB functions for univariate Generalized

Autoregressive Conditional Heteroskedasticity

(GARCH) volatility modeling

MATLAB Integrated technical computing environment

that combines numeric computation, advanced

graphics and visualization, and a high-level

programming language

MATLAB Compiler Compiler for automatically converting

MATLAB M-files to C and C++ code

MATLAB Report

Generator

MATLAB Runtime

Server

Tool for documenting information in MATLAB

in multiple output formats

MATLAB environment in which you can take

an existing MATLAB application and turn it

into a stand-alone product that is easy and

cost-effective to package and distribute. Users

access only the features that you provide via

your application’s graphical user interface

(GUI). They do not have access to your code or

the MATLAB command line.

Optimization Toolbox Tool for general and large-scale optimization of

nonlinear problems, as well as for linear

programming, quadratic programming,

nonlinear least squares, and solving nonlinear

equations

Spline Toolbox Tool for the construction and use of piecewise

polynomial functions

Statistics Toolbox Tool for analyzing historical data, modeling

systems, developing statistical algorithms, and

learning and teaching statistics

xiii

Preface

Background Reading

Black-Derman-Toy (BDT) Modeling

A description of the Black-Derman-Toy interest rate model can be found in:

Black, Fischer, Emanuel Derman, and William Toy, “A One Factor Model of

Interest Rates and its Application to Treasury Bond Options,” Financial

Analysts Journal, January - February 1990.

Heath-Jarrow-Morton (HJM) Modeling

An introduction to Heath-Jarrow-Morton modeling, used extensively in the

Financial Derivatives Toolbox, can be found in:

Jarrow, Robert A., Modelling Fixed Income Securities and Interest Rate

Options, McGraw-Hill, 1996, ISBN 0-07-912253-1.

Financial Derivatives

Information on the creation of financial derivatives and their role in the

marketplace can be found in numerous sources. Among those consulted in the

development of the Financial Derivatives toolbox are:

xiv

Chance, Don. M., An Introduction to Derivatives, The Dryden Press, 1998,

ISBN 0-030-024483-8

Fabozzi, Frank J., Treasury Securities and Derivatives, Frank J. Fabozzi

Associates, 1998, ISBN 1-883249-23-6

Hull, John C., Options, Futures, and Other Derivatives, Prentice-Hall, 1997,

ISBN 0-13-186479-3

Wilmott, Paul, Derivatives: The Theory and Practice of Financial Engineering,

John Wiley and Sons, 1998, ISBN 0-471-983-89-6

Getting Started

Introduction . . . . . . . . . . . . . . . . . . . . 1-2

Interest Rate Models . . . . . . . . . . . . . . . . . 1-2

Trees . . . . . . . . . . . . . . . . . . . . . . . 1-2

Financial Instruments . . . . . . . . . . . . . . . . 1-4

Hedging . . . . . . . . . . . . . . . . . . . . . . 1-5

Creating and Managing Instrument Portfolios . . . . 1-6

Portfolio Creation . . . . . . . . . . . . . . . . . . 1-6

Portfolio Management . . . . . . . . . . . . . . . . 1-9

1

1 Getting Started

Introduction

The Financial Derivatives Toolbox extends the Financial Toolbox in the areas

of fixed income derivatives and of securities contingent upon interest rates. The

toolbox provides components for analyzing individual financial derivative

instruments and portfolios. Specifically, it provides the necessary functions for

calculating prices and sensitivities, for hedging, and for visualizing results.

Interest Rate Models

The Financial Derivatives Toolbox computes pricing and sensitivities of

interest rate contingent claims based upon:

• The interest rate term structure (sets of zero coupon bonds)

• The Heath-Jarrow-Morton (HJM) model of the interest rate term structure.

This model considers a given initial term structure of interest rates and a

specification of the volatility of forward rates to build a tree representing the

evolution of the interest rates, based upon a statistical process.

• The Black-Derman-Toy (BDT) model for pricing interest rate derivatives. In

the BDT model all security prices and rates depend upon the short rate

(annualized one-period interest rate). The model uses long rates and their

volatilities to construct a tree of possible future short rates. It then

determines the value of interest rate sensitive securities from this tree.

1-2

For information, see:

• “Pricing and Sensitivity from Interest Rate Term Structure” on page 2-17 for

a discussion of price and sensitivity based upon portfolios of zero coupon

bonds.

• “Pricing and Sensitivity from HJM” on page 2-35 for a discussion of price and

sensitivity based upon the HJM model.

• “Pricing and Sensitivity from BDT” on page 2-63 for a discussion of price and

sensitivity based upon the BDT model.

Trees

The Heath-Jarrow-Morton model works with a type of interest rate tree called

a bushy tree. A bushy tree is a tree in which the number of branches increases

exponentially relative to observation times; branches never recombine.

Introduction

The Black-Derman-Toy model, on the other hand, works with a recombining

tree. A recombining tree is the opposite of a bushy tree. A recombining tree has

branches that recombine over time. From any given node, the node reached by

taking the path up-down is the same node reached by taking the path down-up.

A bushy and a recombining tree are illustrated below.

Bushy Tree

Recombining Tree

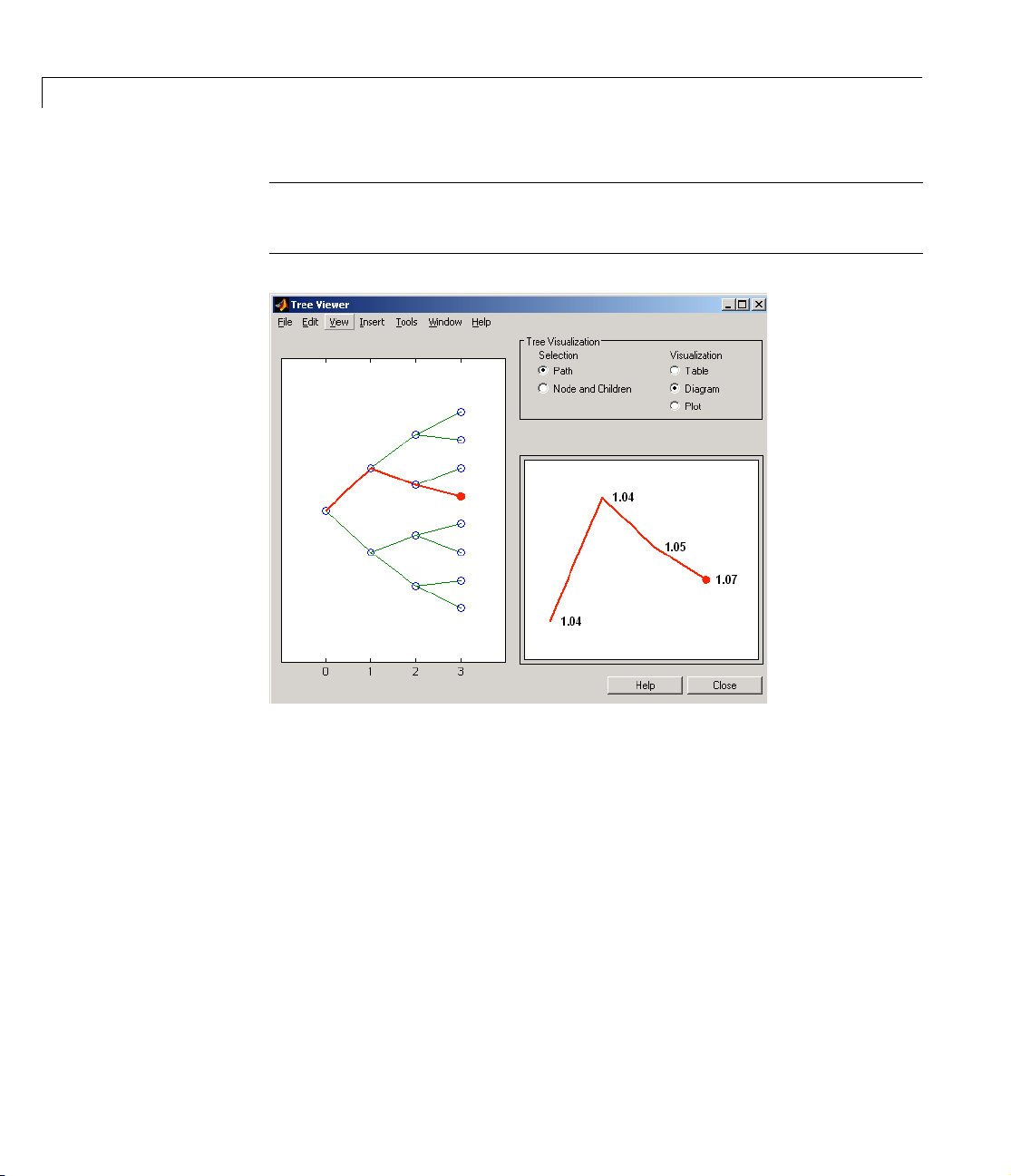

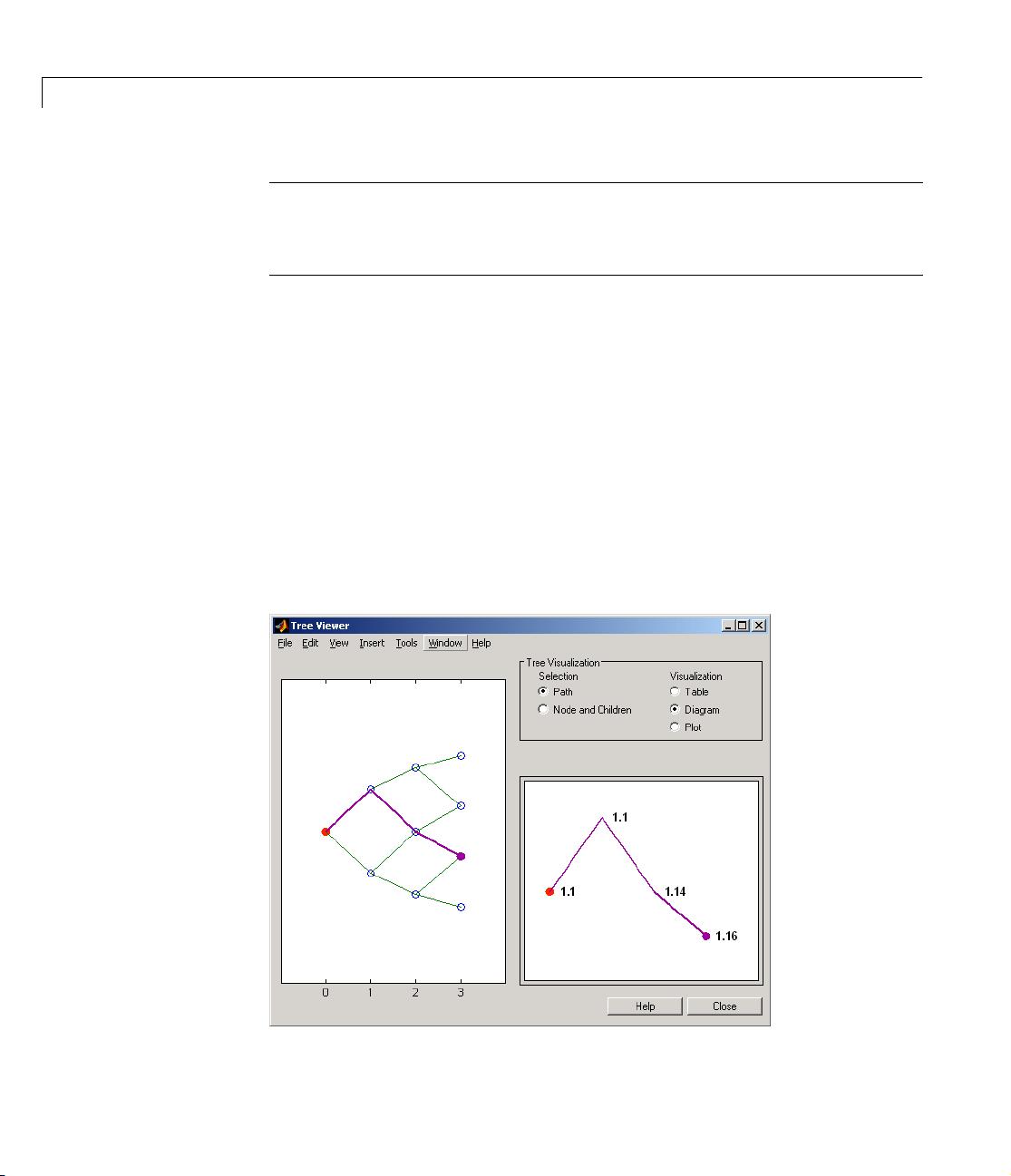

This toolbox provides the data file

a bushy tree, and

treeviewer function, which graphically displays the shape and data of price,

BDTTree, a recombining tree. The toolbox also provides the

interest rate, and cash flow trees. Viewed with

deriv.mat that contains two trees, HJMTree,

treeviewer, the bushy shape of

an HJM tree and the recombining shape of a BDT tree are apparent.

1-3

1 Getting Started

HJMTree (bushy)

BDTTree (recombining)

Financial Instruments

The toolbox provides a set of functions that perform computations upon

portfolios containing up to seven types of financial instruments.

Bond. A long-term debt security with preset interest rate and maturity, by

which the principal and interest must be paid.

Bond Options. Puts and calls on portfolios of bonds.

Fixed Rate Note. A long-term debt security with preset interest rate and

maturity, by which the interest must be paid. The principal may or may not be

paid at maturity. In this version of the Financial Derivatives Toolbox, the

principal is always paid at maturity.

Floating Rate Note. A security similar to a bond, but in which the note’s interest

rate is reset periodically, relative to a reference index rate, to reflect

fluctuations in market interest rates.

Cap. A contract which includes a guarantee that sets the maximum interest

rate to be paid by the holder, based upon an otherwise floating interest rate.

Floor. A contract which includes a guarantee setting the minimum interest rate

to be received by the holder, based upon an otherwise floating interest rate.

1-4

Introduction

Swap. A contract between two parties obligating the parties to exchange future

cash flows. This version of the Financial Derivatives Toolbox handles only the

vanilla swap, which is composed of a floating rate leg and a fixed rate leg.

Additionally, the toolbox provides functions for the creation and pricing of

arbitrary cash flow instruments based upon zero coupon bonds or upon the BDT

or HJM models.

Hedging

The Financial Derivatives Toolbox also includes hedging functionality,

allowing the rebalancing of portfolios to reach target costs or target

sensitivities, which may be set to zero for a neutral-sensitivity portfolio.

Optionally, the rebalancing process can be self-financing or directed by a set of

user-supplied constraints. For information, see:

• “Hedging” on page 3-2 for a discussion of the hedging process.

• “hedgeopt” on page 4-72 for a description of the function that allocates an

optimal hedge.

• “hedgeslf” on page 4-75 for a description of the function that allocates a

self-financing hedge.

1-5

1 Getting Started

Creating and Managing Instrument Portfolios

The Financial Derivatives Toolbox provides components for analyzing

individual derivative instruments and portfolios containing several types of

financial instruments. The toolbox provides functionality that supports the

creation and management of these instruments:

• Bonds

• Bond Options

• Fixed Rate Notes

• Floating Rate Notes

• Caps

• Floors

• Swaps

Additionally, the toolbox provides functions for the creation of arbitrary cash

flow instruments.

The toolbox also provides pricing and sensitivity routines for these

instruments. (See “Pricing and Sensitivity from Interest Rate Term Structure”

on page 2-17, “Pricing and Sensitivity from HJM” on page 2-35, or “Pricing and

Sensitivity from BDT” on page 2-63 for information.)

1-6

Portfolio Creation

The instadd function creates a set of instruments (portfolio) or adds

instruments to an existing instrument collection. The

specifies the type of the investment instrument:

'CashFlow', 'Fixed', 'Float', 'Cap', 'Floor', or 'Swap'. The input

arguments following

instrument. Thus, the

of the input arguments is interpreted.

For example,

instruments

InstSet = instadd('Bond', CouponRate, Settle, Maturity, Period,

Basis, EndMonthRule, IssueDate, FirstCouponDate, LastCouponDate,

StartDate, Face)

instadd with the type string 'Bond' creates a portfolio of bond

TypeString are specific to the type of investment

TypeString argument determines how the remainder

TypeString argument

'Bond', 'OptBond',

Creating and Managing Instrument Portfolios

In a similar manner, instadd can create portfolios of other types of investment

instruments:

• Bond option

InstSet = instadd('OptBond', BondIndex, OptSpec, Strike,

ExerciseDates, AmericanOpt)

• Arbitrary cash flow instrument

InstSet = instadd('CashFlow', CFlowAmounts, CFlowDates, Settle,

Basis)

• Fixed rate note instrument

InstSet = instadd('Fixed', CouponRate, Settle, Maturity,

FixedReset, Basis, Principal)

• Floating rate note instrument

InstSet = instadd('Float', Spread, Settle, Maturity, FloatReset,

Basis, Principal)

• Cap instrument

InstSet = instadd('Cap', Strike, Settle, Maturity, CapReset,

Basis, Principal)

• Floor instrument

InstSet = instadd('Floor', Strike, Settle, Maturity, FloorReset,

Basis, Principal)

• Swap instrument

InstSet = instadd('Swap', LegRate, Settle, Maturity, LegReset,

Basis, Principal, LegType)

To use the instadd function to add additional instruments to an existing

instrument portfolio, provide the name of an existing portfolio as the first

argument to the

instadd function.

1-7

1 Getting Started

Consider, for example, a portfolio containing two cap instruments only.

Strike = [0.06; 0.07];

Settle = '08-Feb-2000';

Maturity = '15-Jan-2003';

Port_1 = instadd('Cap', Strike, Settle, Maturity);

These commands create a portfolio containing two cap instruments with the

same settlement and maturity dates, but with different strikes. In general, the

input arguments describing an instrument can be either a scalar, or a number

of instruments (

NumInst)-by-1 vector in which each element corresponds to an

instrument. Using a scalar assigns the same value to all instruments passed in

the call to

instadd.

Use the

Index Type Strike Settle Maturity CapReset Basis Principal

1 Cap 0.06 08-Feb-2000 15-Jan-2003 NaN NaN NaN

2 Cap 0.07 08-Feb-2000 15-Jan-2003 NaN NaN NaN

instdisp command to display the contents of the instrument set.

instdisp(Port_1)

Now add a single bond instrument to Port_1. The bond has a 4.0% coupon and

the same settlement and maturity dates as the cap instruments.

CouponRate = 0.04;

Port_1 = instadd(Port_1, 'Bond', CouponRate, Settle, Maturity);

Use instdisp again to see the resulting instrument set.

instdisp(Port_1)

Index Type Strike Settle Maturity CapReset Basis Principal

1 Cap 0.06 08-Feb-2000 15-Jan-2003 NaN NaN NaN

2 Cap 0.07 08-Feb-2000 15-Jan-2003 NaN NaN NaN

Index Type CouponRate Settle Maturity Period Basis ...

3 Bond 0.04 08-Feb-2000 15-Jan-2003 NaN NaN ...

1-8

Creating and Managing Instrument Portfolios

Portfolio Management

The portfolio management capabilities provided by the Financial Derivatives

toolbox include:

• Constructors for the most common financial instruments. (See “Instrument

Constructors” on page 1-9.)

• The ability to create new instruments or to add new fields to existing

instruments. (See “Creating New Instruments or Properties” on page 1-10.)

• The ability to search or subset a portfolio. See “Searching or Subsetting a

Portfolio” on page 1-12.)

Instrument Constructors

The toolbox provides constructors for the most common financial instruments.

Note A constructor is a function that builds a structure dedicated to a certain

type of object; in this toolbox, an object is a type of market instrument.

The instruments and their constructors in this toolbox are listed below.

Instrument Constructor

Bond

Bond option

Arbitrary cash flow

Fixed rate note

Floating rate note

Cap

Floor

Swap

instbond

instoptbnd

instcf

instfixed

instfloat

instcap

instfloor

instswap

Each instrument has parameters (fields) that describe the instrument. The

toolbox functions enable you to:

1-9

1 Getting Started

• Create an instrument or portfolio of instruments

• Enumerate stored instrument types and information fields

• Enumerate instrument field data

• Search and select instruments

The instrument structure consists of various fields according to instrument

type. A field is an element of data associated with the instrument. For example,

a bond instrument contains the fields

CouponRate, Settle, Maturity, etc.

Additionally, each instrument has a field that identifies the investment type

(bond, cap, floor, etc.).

In reality the set of parameters for each instrument is not fixed. Users have the

ability to add additional parameters. These additional fields will be ignored by

the toolbox functions. They may be used to attach additional information to

each instrument, such as an internal code describing the bond.

Parameters not specified when creating an instrument default to

NaN, which,

in general, means that the functions using the instrument set (such as

intenvprice or hjmprice) will use default values. At the time of pricing, an

error occurs if any of the required fields is missing, such as

the

CouponRate in a bond.

Strike in a cap, or

Creating New Instruments or Properties

Use the instaddfield function to create a new kind of instrument or to add

new properties to the instruments in an existing instrument collection.

To create a new kind of instrument with

three arguments:

the new instrument, for example,

'Type', 'FieldName', and 'Data'. 'Type' defines the type of

Future. 'FieldName' names the fields

uniquely associated with the new type of instrument.

for the fields of the new instrument.

An optional fourth parameter is

'ClassList'. 'ClassList' specifies the data

types of the contents of each unique field for the new instrument.

Here are the syntaxes to create a new kind of instrument using

InstSet = instaddfield('FieldName', FieldList, 'Data', DataList,

'Type', TypeString)

InstSet = instaddfield('FieldName', FieldList, 'FieldClass',

ClassList, 'Data' , DataList, 'Type', TypeString)

instaddfield, you need to specify

'Data' contains the data

instaddfield.

1-10

Creating and Managing Instrument Portfolios

To add new instruments to an existing set, use

InstSetNew = instaddfield(InstSetOld, 'FieldName', FieldList,

'Data', DataList, 'Type', TypeString)

As an example, consider a futures contract with a delivery date of July 15,

2000, and a quoted price of $104.40. Since the Financial Derivatives Toolbox

does not directly support this instrument, you must create it using the function

instaddfield. The parameters used for the creation of the instruments are:

• Type: Future

• Field names: Delivery and Price

• Data: Delivery is July 15, 2000, and Price is $104.40.

Enter the data into MATLAB.

Type = 'Future';

FieldName = {'Delivery', 'Price'};

Data = {'Jul-15-2000', 104.4};

Optionally, you can also specify the data types of the data cell array by creating

another cell array containing this information.

FieldClass = {'date','dble'};

Finally, create the portfolio with a single instrument.

Port = instaddfield('Type', Type, 'FieldName', FieldName,...

'FieldClass', FieldClass, 'Data', Data);

Now use the function instdisp to examine the resulting single-instrument

portfolio.

instdisp(Port)

Index Type Delivery Price

1 Future 15-Jul-2000 104.4

Because your portfolio Port has the same structure as those created using the

function

portfolios created using

instruments to

instadd, you can combine portfolios created using instadd with

instaddfield. For example, you can now add two cap

Port with instadd.

1-11

1 Getting Started

Strike = [0.06; 0.07];

Settle = '08-Feb-2000';

Maturity = '15-Jan-2003';

Port = instadd(Port, 'Cap', Strike, Settle, Maturity);

View the resulting portfolio using instdisp.

instdisp(Port)

Index Type Delivery Price

1 Future 15-Jul-2000 104.4

Index Type Strike Settle Maturity CapReset Basis Pricipal

2 Cap 0.06 08-Feb-2000 15-Jan-2003 NaN NaN NaN

3 Cap 0.07 08-Feb-2000 15-Jan-2003 NaN NaN NaN

Searching or Subsetting a Portfolio

The Financial Derivatives Toolbox provides functions that enable you to:

1-12

• Find specific instruments within a portfolio

• Create a subset portfolio consisting of instruments selected from a larger

portfolio

The

instfind function finds instruments with a specific parameter value; it

returns an instrument index (position) in a large instrument set. The

instselect function, on the other hand, subsets a large instrument set into a

portfolio of instruments with designated parameter values; it returns an

instrument set (portfolio) rather than an index.

instfind. The general syntax for instfind is

IndexMatch = instfind(InstSet, 'FieldName', FieldList, 'Data',

DataList, 'Index', IndexSet, 'Type', TypeList)

InstSet

is the instrument set to search. Within InstSet instruments are

categorized by type, and each type can have different data fields. The stored

data field is a row vector or string for each instrument.

The

FieldList, DataList, and TypeList arguments indicate values to search

for in the

FieldList is a cell array of field name(s) specific to the instruments. DataList

'FieldName', 'Data', and 'Type' data fields of the instrument set.

Creating and Managing Instrument Portfolios

is a cell array or matrix of acceptable values for the parameter(s) specified in

FieldList. 'FieldName' and 'Data' (consequently, FieldList and DataList)

parameters must appear together or not at all.

IndexSet is a vector of integer index(es) designating positions of instruments

in the instrument set to check for matches; the default is all indices available

in the instrument set.

instruments to match one of the

'TypeList' is a string or cell array of strings restricting

'TypeList' types; the default is all types in

the instrument set.

IndexMatch is a vector of positions of instruments matching the input criteria.

Instruments are returned in

'Index', and 'Type' conditions are met. An instrument meets an individual

field condition if the stored

the

DataList for that FieldName.

instfind Examples. The examples use the provided MAT-file deriv.mat.

IndexMatch if all the 'FieldName', 'Data',

'FieldName' data matches any of the rows listed in

The MAT-file contains an instrument set,

HJMInstSet, that contains eight

instruments of seven types.

load deriv.mat

instdisp(HJMInstSet)

Index Type CouponRate Settle Maturity Period Basis ......... Name Quantity

1 Bond 0.04 01-Jan-2000 01-Jan-2003 1 NaN......... 4% bond 100

2 Bond 0.04 01-Jan-2000 01-Jan-2004 2 NaN......... 4% bond 50

Index Type UnderInd OptSpec Strike ExerciseDates AmericanOpt Name Quantity

3 OptBond 2 call 101 01-Jan-2003 NaN Option 101 -50

Index Type CouponRate Settle Maturity FixedReset Basis Principal Name Quantity

4 Fixed 0.04 01-Jan-2000 01-Jan-2003 1 NaN NaN 4% Fixed 80

Index Type Spread Settle Maturity FloatReset Basis Principal Name Quantity

5 Float 20 01-Jan-2000 01-Jan-2003 1 NaN NaN 20BP Float 8

Index Type Strike Settle Maturity CapReset Basis Principal Name Quantity

6 Cap 0.03 01-Jan-2000 01-Jan-2004 1 NaN NaN 3% Cap 30

Index Type Strike Settle Maturity FloorReset Basis Principal Name Quantity

7 Floor 0.03 01-Jan-2000 01-Jan-2004 1 NaN NaN 3% Floor 40

Index Type LegRate Settle Maturity LegReset Basis Principal LegType Name Quantity

8 Swap [0.06 20] 01-Jan-2000 01-Jan-2003 [1 1] NaN NaN [NaN] 6%/20BP Swap 10

1-13

1 Getting Started

Find all instruments with a maturity date of January 01, 2003.

Mat2003 = ...

instfind(HJMInstSet,'FieldName','Maturity','Data','01-Jan-2003')

Mat2003 =

1

4

5

8

Find all cap and floor instruments with a maturity date of January 01, 2004.

CapFloor = instfind(HJMInstSet,...

'FieldName','Maturity','Data','01-Jan-2004', 'Type',...

{'Cap';'Floor'})

CapFloor =

6

7

1-14

Find all instruments where the portfolio is long or short a quantity of 50.

Pos50 = instfind(HJMInstSet,'FieldName',...

'Quantity','Data',{'50';'-50'})

Pos50 =

2

3

instselect.

instfind. instselect returns a full portfolio instead of indexes into the

The syntax for instselect is exactly the same syntax as for

original portfolio. Compare the values returned by both functions by calling

them equivalently.

Previously you used

instfind to find all instruments in HJMInstSet with a

maturity date of January 01, 2003.

Creating and Managing Instrument Portfolios

Mat2003 = ...

instfind(HJMInstSet,'FieldName','Maturity','Data','01-Jan-2003')

Mat2003 =

1

4

5

8

Now use the same instrument set as a starting point, but execute the

instselect function instead, to produce a new instrument set matching the

identical search criteria.

Select2003 = ...

instselect(HJMInstSet,'FieldName','Maturity','Data',...

'01-Jan-2003')

instdisp(Select2003)

Index Type CouponRate Settle Maturity Period Basis ......... Name Quantity

1 Bond 0.04 01-Jan-2000 01-Jan-2003 1 NaN......... 4% bond 100

Index Type CouponRate Settle Maturity FixedReset Basis Principal Name Quantity

2 Fixed 0.04 01-Jan-2000 01-Jan-2003 1 NaN NaN 4% Fixed 80

Index Type Spread Settle Maturity FloatReset Basis Principal Name Quantity

3 Float 20 01-Jan-2000 01-Jan-2003 1 NaN NaN 20BP Float 8

Index Type LegRate Settle Maturity LegReset Basis Principal LegType Name Quantity

4 Swap [0.04 20] 01-Jan-2000 01-Jan-2003 [1 1] NaN NaN [NaN] 4%/20BP Swap 10

1-15

1 Getting Started

instselect Examples. These examples use the portfolio ExampleInst provided with

the MAT-file

load InstSetExamples.mat

instdisp(ExampleInst)

Index Type Strike Price Opt Contracts

1 Option 95 12.2 Call 0

2 Option 100 9.2 Call 0

3 Option 105 6.8 Call 1000

Index Type Delivery F Contracts

4 Futures 01-Jul-1999 104.4 -1000

Index Type Strike Price Opt Contracts

5 Option 105 7.4 Put -1000

6 Option 95 2.9 Put 0

Index Type Price Maturity Contracts

7 TBill 99 01-Jul-1999 6

InstSetExamples.mat.

1-16

The instrument set contains three instrument types: 'Option', 'Futures',

and

'TBill'. Use instselect to make a new instrument set containing only

options struck at

Strike and with the data value for that field equal to 95.

InstSet = instselect(ExampleInst,'FieldName','Strike','Data',95)

instdisp(InstSet)

Index Type Strike Price Opt Contracts

1 Option 95 12.2 Call 0

2 Option 95 2.9 Put 0

95. In other words, select all instruments containing the field

You can use all the various forms of instselect and instfind to locate specific

instruments within this instrument set.

Using Financial Derivatives

Interest Rate Environment . . . . . . . . . . . . . 2-3

Interest Rates vs. Discount Factors . . . . . . . . . . . 2-3

Interest Rate Term Conversions . . . . . . . . . . . . 2-8

Interest Rate Term Structure . . . . . . . . . . . . . 2-12

Pricing and Sensitivity from

Interest Rate Term Structure . . . . . . . . . . 2-17

Pricing . . . . . . . . . . . . . . . . . . . . . . . 2-18

Sensitivity . . . . . . . . . . . . . . . . . . . . . 2-20

Heath-Jarrow-Morton (HJM) Model . . . . . . . . . 2-22

Building an HJM Forward Rate Tree . . . . . . . . . . 2-22

Using HJM Trees in MATLAB . . . . . . . . . . . . . 2-28

2

Pricing and Sensitivity from HJM . . . . . . . . . . 2-35

Pricing and the Price Tree . . . . . . . . . . . . . . . 2-35

Using treeviewer to View Instrument Prices Through Time . 2-40

HJM Pricing Options Structure . . . . . . . . . . . . . 2-44

Calculating Prices and Sensitivities . . . . . . . . . . . 2-50

Black-Derman-Toy Model (BDT) . . . . . . . . . . . 2-53

Building a BDT Interest Rate Tree . . . . . . . . . . . 2-53

Using BDT Trees in MATLAB . . . . . . . . . . . . . 2-57

Pricing and Sensitivity from BDT . . . . . . . . . . 2-63

Pricing and the Price Tree . . . . . . . . . . . . . . . 2-63

BDT Pricing Options Structure . . . . . . . . . . . . . 2-71

Calculating Prices and Sensitivities . . . . . . . . . . . 2-71

2 Using Financial Derivatives

The Financial Derivatives Toolbox provides functions for computing the price

and sensitivities of interest rate dependent securities based upon three distinct

models for representing interest rates:

• A set of interest rate curves computed from zero coupon bonds. (See the

sections “Interest Rate Environment” on page 2-3 and “Pricing and

Sensitivity from Interest Rate Term Structure” on page 2-17.)

• The Heath-Jarrow-Morton interest rate model. (See the sections

“Heath-Jarrow-Morton (HJM) Model” on page 2-22 and “Pricing and

Sensitivity from HJM” on page 2-35.)

• The Black-Derman-Toy interest rate model. (See the sections

“Black-Derman-Toy Model (BDT)” on page 2-53 and “Pricing and Sensitivity

from BDT” on page 2-63.)

2-2

Interest Rate Environment

The interest rate term structure is the representation of the evolution of interest

rates through time. In MATLAB, the interest rate environment is

encapsulated in a structure called

holds all information needed to identify completely the evolution of interest

rates. Several functions included in the Financial Derivatives Toolbox are

dedicated to the creation and management of the

others take this structure as an input argument representing the evolution of

interest rates.

Interest Rate Environment

RateSpec (rate specification). This structure

RateSpec structure. Many

Before looking further at the

provide key functionality for working with interest rates:

opposite,

rate2disc, and ratetimes. The first two functions map between

discount rates and interest rates. The third function,

RateSpec structure, examine three functions that

disc2rate, its

ratetimes, calculates the

effect of term changes on the interest rates.

Interest Rates vs. Discount Factors

Discount factors are coefficients commonly used to find the present value of

future cash flows. As such, there is a direct mapping between the rate

applicable to a period of time, and the corresponding discount factor. The

function

interest rates. The function

rates applicable to a given term (period) into the corresponding discount rates.

Calculating Discount Factors from Rates

As an example, consider these annualized zero coupon bond rates.

From To Rate

15 Feb 2000 15 Aug 2000 0.05

15 Feb 2000 15 Feb 2001 0.056

15 Feb 2000 15 Aug 2001 0.06

15 Feb 2000 15 Feb 2002 0.065

disc2rate converts discount rates for a given term (period) into

rate2disc does the opposite; it converts interest

15 Feb 2000 15 Aug 2002 0.075

2-3

2 Using Financial Derivatives

To calculate the discount factors corresponding to these interest rates, call

rate2disc using the syntax

Disc = rate2disc(Compounding, Rates, EndDates, StartDates,

ValuationDate)

where:

Compounding represents the frequency at which the zero rates are

•

compounded when annualized. For this example, assume this value to be 2.

Rates is a vector of annualized percentage rates representing the interest

•

rate applicable to each time interval.

•

EndDates is a vector of dates representing the end of each interest rate term

(period).

•

StartDates is a vector of dates representing the beginning of each interest

rate term.

ValuationDate is the date of observation for which the discount factors are

•

calculated. In this particular example, use February 15, 2000 as the

beginning date for all interest rate terms.

2-4

Set the variables in MATLAB.

StartDates = ['15-Feb-2000'];

EndDates = ['15-Aug-2000'; '15-Feb-2001'; '15-Aug-2001';...

'15-Feb-2002'; '15-Aug-2002'];

Compounding = 2;

ValuationDate = ['15-Feb-2000'];

Rates = [0.05; 0.056; 0.06; 0.065; 0.075];

Disc = rate2disc(Compounding, Rates, EndDates, StartDates,...

ValuationDate)

Disc =

0.9756

0.9463

0.9151

0.8799

0.8319

Interest Rate Environment

By adding a fourth column to the above rates table to include the corresponding

discounts, you can see the evolution of the discount rates.

From To Rate Discount

15 Feb 2000 15 Aug 2000 0.05 0.9756

15 Feb 2000 15 Feb 2001 0.056 0.9463

15 Feb 2000 15 Aug 2001 0.06 0.9151

15 Feb 2000 15 Feb 2002 0.065 0.8799

15 Feb 2000 15 Aug 2002 0.075 0.8319

Optional Time Factor Outputs

The function rate2disc optionally returns two additional output arguments:

EndTimes and StartTimes. These vectors of time factors represent the start

dates and end dates in discount periodic units. The scale of these units is

determined by the value of the input variable

To examine the time factor outputs, find the corresponding values in the

previous example.

Compounding.

[Disc, EndTimes, StartTimes] = rate2disc(Compounding, Rates,...

EndDates, StartDates, ValuationDate);

Arrange the two vectors into a single array for easier visualization.

Times = [StartTimes, EndTimes]

Times =

0 1

0 2

0 3

0 4

05

Because the valuation date is equal to the start date for all periods, the

StartTimes vector is composed of zeros. Also, since the value of Compounding is

2, the rates are compounded semiannually, which sets the units of periodic

discount to six months. The vector

EndDates is composed of dates separated by

2-5

2 Using Financial Derivatives

intervals of six months from the valuation date. This explains why the

EndTimes vector is a progression of integers from one to five.

Alternative Syntax (rate2disc)

The function rate2disc also accommodates an alternative syntax that uses

periodic discount units instead of dates. Since the relationship between

discount factors and interest rates is based on time periods and not on absolute

dates, this form of

this mode, the valuation date corresponds to zero, and the vectors

and

EndTimes are used as input arguments instead of their date equivalents,

StartDates and EndDates. This syntax for rate2disc is

Disc = rate2disc(Compounding, Rates, EndTimes, StartTimes)

Using as input the StartTimes and EndTimes vectors computed previously, you

should obtain the previous results for the discount factors.

Disc = rate2disc(Compounding, Rates, EndTimes, StartTimes)

Disc =

rate2disc allows you to work directly with time periods. In

StartTimes

2-6

0.9756

0.9463

0.9151

0.8799

0.8319

Calculating Rates from Discounts

The function disc2rate is the complement to rate2disc. It finds the rates

applicable to a set of compounding periods, given the discount factor in those

periods. The syntax for calling this function is

Rates = disc2rate(Compounding, Disc, EndDates, StartDates,

ValuationDate)

Each argument to this function has the same meaning as in rate2disc. Use the

results found in the previous example to return the rate values you started

with.

Rates = disc2rate(Compounding, Disc, EndDates, StartDates,...

ValuationDate)

Interest Rate Environment

Rates =

0.0500

0.0560

0.0600

0.0650

0.0750

Alternative Syntax (disc2rate)

As in the case of rate2disc, disc2rate optionally returns StartTimes and

EndTimes vectors representing the start and end times measured in discount

periodic units. Again, working with the same values as before, you should

obtain the same numbers.

[Rates, EndTimes, StartTimes] = disc2rate(Compounding, Disc,...

EndDates, StartDates, ValuationDate);

Arrange the results in a matrix convenient to display.

Result = [StartTimes, EndTimes, Rates]

Result =

0 1.0000 0.0500

0 2.0000 0.0560

0 3.0000 0.0600

0 4.0000 0.0650

0 5.0000 0.0750

As with rate2disc, the relationship between rates and discount factors is

determined by time periods and not by absolute dates. Consequently, the

alternate syntax for

disc2rate uses time vectors instead of dates, and it

assumes that the valuation date corresponds to time = 0. The times-based

calling syntax is

Rates = disc2rate(Compounding, Disc, EndTimes, StartTimes);

Using this syntax, we again obtain the original values for the interest rates.

2-7

2 Using Financial Derivatives

Rates = disc2rate(Compounding, Disc, EndTimes, StartTimes)

Rates =

0.0500

0.0560

0.0600

0.0650

0.0750

Interest Rate Term Conversions

Interest rate evolution is typically represented by a set of interest rates,

including the beginning and end of the periods the rates apply to. For zero

rates, the start dates are typically at the valuation date, with the rates

extending from that valuation date until their respective maturity dates.

Calculating Rates Applicable to Different Periods

Frequently, given a set of rates including their start and end dates, you may be

interested in finding the rates applicable to different terms (periods). This

problem is addressed by the function

interest rates given a change in the original terms. The syntax for calling

ratetimes is

ratetimes. This function interpolates the

2-8

[Rates, EndTimes, StartTimes] = ratetimes(Compounding, RefRates,

RefEndDates, RefStartDates, EndDates, StartDates, ValuationDate);

where:

•

Compounding represents the frequency at which the zero rates are

compounded when annualized.

•

RefRates is a vector of initial interest rates representing the interest rates

applicable to the initial time intervals.

•

RefEndDates is a vector of dates representing the end of the interest rate

terms (period) applicable to

•

RefStartDates is a vector of dates representing the beginning of the interest

rate terms applicable to

•

EndDates represent the maturity dates for which the interest rates are

RefRates.

RefRates.

interpolated.

Interest Rate Environment

• StartDates represent the starting dates for which the interest rates are

interpolated.

•

ValuationDate is the date of observation, from which the StartTimes and

EndTimes are calculated. This date represents time = 0.

The input arguments to this function can be separated into two groups:

• The initial or reference interest rates, including the terms for which they are

valid

• Terms for which the new interest rates are calculated

As an example, consider the rate table specified earlier.

From To Rate

15 Feb 2000 15 Aug 2000 0.05

15 Feb 2000 15 Feb 2001 0.056

15 Feb 2000 15 Aug 2001 0.06

15 Feb 2000 15 Feb 2002 0.065

15 Feb 2000 15 Aug 2002 0.075

Assuming that the valuation date is February 15, 2000, these rates represent

zero coupon bond rates with maturities specified in the second column. Use the

function

ratetimes to calculate the spot rates at the beginning of all periods

implied in the table. Assume a compounding value of 2.

% Reference Rates.

RefStartDates = ['15-Feb-2000'];

RefEndDates = ['15-Aug-2000'; '15-Feb-2001'; '15-Aug-2001';...

'15-Feb-2002'; '15-Aug-2002'];

Compounding = 2;

ValuationDate = ['15-Feb-2000'];

RefRates = [0.05; 0.056; 0.06; 0.065; 0.075];

% New Terms.

StartDates = ['15-Feb-2000'; '15-Aug-2000'; '15-Feb-2001';...

'15-Aug-2001'; '15-Feb-2002'];

EndDates = ['15-Aug-2000'; '15-Feb-2001'; '15-Aug-2001';...

'15-Feb-2002'; '15-Aug-2002'];

2-9

2 Using Financial Derivatives

% Find the new rates.

[Rates, EndTimes, StartTimes] = ratetimes(Compounding, ...

RefRates, RefEndDates, RefStartDates, EndDates, StartDates,...

ValuationDate);

Rates =

0.0500

0.0620

0.0680

0.0801

0.1155

Place these values in a table similar to the one above. Observe the evolution of

the spot rates based on the initial zero coupon rates.

From To Rate

15 Feb 2000 15 Aug 2000 0.0500

15 Aug 2000 15 Feb 2001 0.0620

2-10

15 Feb 2001 15 Aug 2001 0.0680

15 Aug 2001 15 Feb 2002 0.0801

15 Feb 2002 15 Aug 2002 0.1155

Alternative Syntax (ratetimes)

The additional output arguments StartTimes and EndTimes represent the time

factor equivalents to the

functions

disc2rate and rate2disc, ratetimes uses time factors for

interpolating the rates. These time factors are calculated from the start and

end dates, and the valuation date, which are passed as input arguments.

ratetimes also has an alternate syntax that uses time factors directly, and

assumes time = 0 as the valuation date. This alternate syntax is

[Rates, EndTimes, StartTimes] = ratetimes(Compounding, RefRates,

RefEndTimes, RefStartTimes, EndTimes, StartTimes);

Use this alternate version of ratetimes to find the spot rates again. In this

case, you must first find the time factors of the reference curve. Use

for this.

StartDates and EndDates vectors. As with the

date2time

Interest Rate Environment

RefEndTimes = date2time(ValuationDate, RefEndDates, Compounding)

RefEndTimes =

1

2

3

4

5

RefStartTimes = date2time(ValuationDate, RefStartDates,...

Compounding)

RefStartTimes =

0

These are the expected values, given semiannual discounts (as denoted by a

value of 2 in the variable

Compounding), end dates separated by six-month

periods, and the valuation date equal to the date marking beginning of the first

period (time factor = 0).

Now call

EndTimes

ratetimes with the alternate syntax.

[Rates, EndTimes, StartTimes] = ratetimes(Compounding,...

RefRates, RefEndTimes, RefStartTimes, EndTimes, StartTimes);

Rates =

0.0500

0.0620

0.0680

0.0801

0.1155

and StartTimes have, as expected, the same values they had as input

arguments.

2-11

2 Using Financial Derivatives

Times = [StartTimes, EndTimes]

Times =

0 1

1 2

2 3

3 4

4 5

Interest Rate Term Structure

The Financial Derivatives Toolbox includes a set of functions to encapsulate

interest rate term information into a single structure. These functions present

a convenient way to package all information related to interest rate terms into

a common format, and to resolve interdependencies when one or more of the

parameters is modified. For information, see:

• “Creation or Modification (intenvset)” on page 2-12 for a discussion of how to

create or modify an interest rate term structure (

intenvset function.

• “Obtaining Specific Properties (intenvget)” on page 2-14 for a discussion of

how to extract specific properties from a

RateSpec.

RateSpec) using the

2-12

Creation or Modification (intenvset)

The main function to create or modify an interest rate term structure RateSpec

(rates specification) is intenvset. If the first argument to this function is a

previously created

specification and returns a new one. Otherwise, it creates a new

other

intenvset arguments are property-value pairs, indicating the new value

for these properties. The properties that can be specified or modified are:

Compounding

•

• Disc

• Rates

RateSpec, the function modifies the existing rate

RateSpec. The

Interest Rate Environment

• EndDates

• StartDates

• ValuationDate

• Basis

• EndMonthRule

To learn about the properties EndMonthRule and Basis, type

help ftbEndMonthRule and help ftbBasis or see the Financial Toolbox

User's Guide.

Consider again the original table of interest rates.

From To Rate

15 Feb 2000 15 Aug 2000 0.05

15 Feb 2000 15 Feb 2001 0.056

15 Feb 2000 15 Aug 2001 0.06

15 Feb 2000 15 Feb 2002 0.065

15 Feb 2000 15 Aug 2002 0.075

Use the information in this table to populate the

StartDates = ['15-Feb-2000'];

EndDates = ['15-Aug-2000';

'15-Feb-2001';

'15-Aug-2001';

'15-Feb-2002';

'15-Aug-2002'];

Compounding = 2;

ValuationDate = ['15-Feb-2000'];

Rates = [0.05; 0.056; 0.06; 0.065; 0.075];

rs = intenvset('Compounding',Compounding,'StartDates',...

StartDates, 'EndDates', EndDates, 'Rates', Rates,...

'ValuationDate', ValuationDate)

RateSpec structure.

2-13

2 Using Financial Derivatives

rs =

FinObj:'RateSpec'

Compounding:2

Disc:[5x1 double]

Rates:[5x1 double]

EndTimes:[5x1 double]

StartTimes:[5x1 double]

EndDates:[5x1 double]

StartDates:730531

ValuationDate:730531

Basis: 0

EndMonthRule: 1

Some of the properties filled in the structure were not passed explicitly in the

call to

RateSpec. The values of the automatically completed properties depend

upon the properties that are explicitly passed. Consider for example the

StartTimes and EndTimes vectors. Since the StartDates and EndDates vectors

are passed in, as well as the

needed to calculate

StartTimes and EndTimes. Hence, these two properties are

ValuationDate, intenvset has all the information

read only.

2-14

Obtaining Specific Properties (intenvget)

The complementary function to intenvset is intenvget. This function obtains

specific properties from the interest rate term structure. The syntax of this

function is

ParameterValue = intenvget(RateSpec, 'ParameterName')

To obtain the vector EndTimes from the RateSpec structure, enter

EndTimes = intenvget(rs, 'EndTimes')

EndTimes =

1

2

3

4

5

Interest Rate Environment

To obtain Disc, the values for the discount factors that were calculated

automatically by

Disc = intenvget(rs, 'Disc')

Disc =

0.9756

0.9463

0.9151

0.8799

0.8319

intenvset, type

These discount factors correspond to the periods starting from StartDates and

ending in

EndDates.

Note Although you can directly access these fields within the structure

instead of using

intenvget, we strongly advise against this. The format of the

interest rate term structure could change in future versions of the toolbox.

Should that happen, any code accessing the

RateSpec fields directly would

stop working.

Now use the

RateSpec structure with its functions to examine how changes in

specific properties of the interest rate term structure affect those depending

upon it. As an exercise, change the value of

Compounding from 2 (semiannual)

to 1 (annual).

rs = intenvset(rs, 'Compounding', 1);

Since StartTimes and EndTimes are measured in units of periodic discount, a

change in

Compounding from 2 to 1 redefines the basic unit from semiannual to

annual. This means that a period of six months is represented with a value of

0.5, and a period of one year is represented by 1. To obtain the vectors

StartTimes and EndTimes, enter

StartTimes = intenvget(rs, 'StartTimes');

EndTimes = intenvget(rs, 'EndTimes');

2-15

2 Using Financial Derivatives

Times = [StartTimes, EndTimes]

Times =

0 0.5000

0 1.0000

0 1.5000

0 2.0000

0 2.5000

Since all the values in StartDates are the same as the valuation date, all

StartTimes values are zero. On the other hand, the values in the EndDates

vector are dates separated by six-month periods. Since the redefined value of

compounding is 1,

EndTimes becomes a sequence of numbers separated by

increments of 0.5.

2-16

Pricing and Sensitivity from Interest Rate Term Structure

Pricing and Sensitivity from Interest Rate Term Structure

The Financial Derivatives Toolbox contains a family of functions that finds the

price and sensitivities of several financial instruments based on interest rate

curves. For information, see:

• “Pricing” on page 2-18 for a discussion on using the

price a portfolio of instruments based on a set of zero curves.

• “Sensitivity” on page 2-20 for a discussion on computing delta and gamma

sensitivities with the

The instruments can be presented to the functions as a portfolio of different

types of instruments or as groups of instruments of the same type. The current

version of the toolbox can compute price and sensitivities for four instrument

types using interest rate curves:

• Bonds

• Fixed Rate Notes

• Floating Rate Notes

• Swaps

In addition to these instruments, the toolbox also supports the calculation of

price and sensitivities of arbitrary sets of cash flows.

Note that options and interest rates floors and caps are absent from the above

list of supported instruments. These instruments are not supported because

their pricing and sensitivity function require a stochastic model for the

evolution of interest rates. The interest rate term structure used for pricing is

treated as deterministic, and as such is not adequate for pricing these

instruments.

intenvsens function.

intenvprice function to

The Financial Derivatives Toolbox additionally contains functions that use the

Heath-Jarrow-Morton (HJM) and Black-Derman-Toy (BDT) models to

compute prices and sensitivities for financial instruments. These models

support computations involving options and interest rate floors and caps. See

“Pricing and Sensitivity from HJM” on page 2-35 and “Pricing and Sensitivity

from BDT” on page 2-63 for information on computing price and sensitivities of

financial instruments using HJM and BDT models.

2-17

2 Using Financial Derivatives

Pricing

The main function used for pricing portfolios of instruments is intenvprice.

This function works with the family of functions that calculate the prices of

individual types of instruments. When called,

portfolio contained in

InstSet by instrument type, and calls the appropriate

pricing functions. The map between instrument types and the pricing function

intenvprice calls is

bondbyzero: Price bond by a set of zero curves

fixedbyzero: Price fixed rate note by a set of zero curves

floatbyzero: Price floating rate note by a set of zero curves

swapbyzero: Price swap by a set of zero curves

Each of these functions can be used individually to price an instrument.

Consult the reference pages for specific information on the use of these

functions.

intenvprice takes as input an interest rate term structure created with

intenvset, and a portfolio of interest rate contingent derivatives instruments

created with

instadd. To learn more about instadd, see “Creating and

Managing Instrument Portfolios” on page 1-6, and to learn more about the

interest rate term structure see “Interest Rate Environment” on page 2-3.

intenvprice classifies the

2-18

The syntax for using

Price = intenvprice(RateSpec, InstSet)

intenvprice to price an entire portfolio is

where:

•

RateSpec is the interest rate term structure.

•

InstSet is the name of the portfolio.

Example: Pricing a Portfolio of Instruments

Consider this example of using the intenvprice function to price a portfolio of

instruments supplied with the Financial Derivatives Toolbox.

The provided MAT-file

variable

structure

instdisp.

ZeroInstSet. The MAT-file also contains the interest rate term

ZeroRateSpec. You can display the instruments with the function

deriv.mat stores a portfolio as an instrument set

Pricing and Sensitivity from Interest Rate Term Structure

load deriv.mat;

instdisp(ZeroInstSet)

Index Type CouponRate Settle Maturity Period Basis...

1 Bond 0.04 01-Jan-2000 01-Jan-2003 1 NaN...

2 Bond 0.04 01-Jan-2000 01-Jan-2004 2 NaN...

Index Type CouponRate Settle Maturity FixedReset Basis...

3 Fixed 0.04 01-Jan-2000 01-Jan-2003 1 NaN...

Index Type Spread Settle Maturity FloatReset Basis...

4 Float 20 01-Jan-2000 01-Jan-2003 1 NaN...

Index Type LegRate Settle Maturity LegReset Basis...

5 Swap [0.06 20] 01-Jan-2000 01-Jan-2003 [1 1] NaN...

Use intenvprice to calculate the prices for the instruments contained in the

portfolio

ZeroInstSet.

format bank

Prices = intenvprice(ZeroRateSpec, ZeroInstSet)

Prices =

98.72

97.53

98.72

100.55

3.69

The output Prices is a vector containing the prices of all the instruments in the

portfolio in the order indicated by the

Consequently, the first two elements in

Index column displayed by instdisp.

Prices correspond to the first two

bonds; the third element corresponds to the fixed rate note; the fourth to the

floating rate note; and the fifth element corresponds to the price of the swap.

2-19

2 Using Financial Derivatives

Sensitivity

The Financial Derivatives Toolbox can calculate two types of derivative price

sensitivities, namely delta and gamma. Delta represents the dollar sensitivity

of prices to shifts in the observed forward yield curve. Gamma represents the

dollar sensitivity of delta to shifts in the observed forward yield curve.

The

intenvsens function computes instrument sensitivities as well as

instrument prices. If you need both the prices and sensitivity measures, use

intenvsens. A separate call to intenvprice is not required.

Here is the syntax

[Delta, Gamma, Price] = intenvsens(RateSpec, InstSet)

where, as before:

RateSpec is the interest rate term structure.

•

InstSet is the name of the portfolio.

•

Example: Sensitivities and Prices

Here is an example of using intenvsens to calculate both sensitivities and

prices.

2-20

format long

load deriv.mat;

[Delta, Gamma, Price] = intenvsens(ZeroRateSpec, ZeroInstSet);

Display the results in a single matrix in long format.

All = [Delta Gamma Price]

All =

1.0e+003 *

-0.27264034403478 1.02984451401241 0.09871593902758

-0.34743857788527 1.62265027222659 0.09753338552637

-0.27264034403478 1.02984451401241 0.09871593902758

-0.00104445683331 0.00330878190894 0.10055293001355

-0.28204045553455 1.05962355119047 0.00369230914950

Pricing and Sensitivity from Interest Rate Term Structure

To view the per-dollar sensitivity, divide the first two columns by the last one.

[Delta./Price, Gamma./Price, Price]

ans =

1.0e+002 *

-0.02761867503065 0.10432403562759 0.98715939027581

-0.03562252822561 0.16636870169834 0.97533385526369

-0.02761867503065 0.10432403562759 0.98715939027581

-0.00010387134748 0.00032905872643 1.00552930013547

-0.76385926561057 2.86981265188338 0.03692309149502

2-21

2 Using Financial Derivatives

Heath-Jarrow-Morton (HJM) Model

The Heath-Jarrow-Morton (HJM) model is one of the most widely used models

for pricing interest rate derivatives. The model considers a given initial term

structure of interest rates and a specification of the volatility of forward rates

to build a tree representing the evolution of the interest rates, based upon a

statistical process. For further explanation, see the book “Modelling Fixed

Income Securities and Interest Rate Options” by Robert A. Jarrow.

Building an HJM Forward Rate Tree

The HJM tree of forward rates is the fundamental unit representing the

evolution of interest rates in a given period of time. This section explains how

to create the HJM forward rate tree using the Financial Derivatives Toolbox.

The MATLAB function that creates the HJM forward rate tree is hjmtree. This

function takes three structures as input arguments:

• The volatility model

(VolSpec)” on page 2-23.)

• The interest rate term structure

Rate Term Structure (RateSpec)” on page 2-25.)

• The tree time layout

(TimeSpec)” on page 2-26.)

VolSpec. (See “Specifying the Volatility Model

RateSpec. (See “Specifying the Interest

TimeSpec. (See “Specifying the Time Structure

Creating the HJM Forward Rate Tree (hjmtree)

Calling the function hjmtree creates the structure, HJMTree, containing time

and forward rate information for a bushy tree.

This structure is a self-contained unit that includes the HJM tree of rates

(found in the

specifications used in building this tree.

The calling syntax for

HJMTree = hjmtree(VolSpec, RateSpec, TimeSpec)

FwdTree field of the structure), and the volatility, rate, and time

hjmtree is

2-22

Heath-Jarrow-Morton (HJM) Model

where:

•

VolSpec is a structure that specifies the forward rate volatility process.

VolSpec is created using the function hjmvolspec. The hjmvolspec function

supports the specification of multiple factors. It handles five models for the

volatility of the interest rate term structure:

- Constant

- Stationary

- Exponential

- Vasicek

- Proportional

Incorporating multiple factors allows you to specify different types of shifts

in the shape and location of the interest rate structure. A one-factor model

assumes that the interest term structure is affected by a single source of

uncertainty.

•

RateSpec is the interest rate specification of the initial rate curve. This

structure is created with the function

intenvset. (See “Interest Rate Term

Structure” on page 2-12.)

•

TimeSpec is the tree time layout specification. This variable is created with

the function

hjmtimespec. It represents the mapping between level times

and level dates for rate quoting. This structure determines indirectly the

number of levels of the tree generated in the call to

hjmtree.

Specifying the Volatility Model (VolSpec)