Page 1

Datafeed Toolbox™ 3

User’s Guide

Page 2

How to Contact The MathWorks

www.mathworks.

comp.soft-sys.matlab Newsgroup

www.mathworks.com/contact_TS.html Technical Support

suggest@mathworks.com Product enhancement suggestions

bugs@mathwo

doc@mathworks.com Documentation error reports

service@mathworks.com Order status, license renewals, passcodes

info@mathwo

com

rks.com

rks.com

Web

Bug reports

Sales, prici

ng, and general information

508-647-7000 (Phone)

508-647-7001 (Fax)

The MathWorks, Inc.

3 Apple Hill Drive

Natick, MA 01760-2098

For contact information about worldwide offices, see the MathWorks Web site.

Datafeed Toolbox™ User’s Guide

© COPYRIGHT 1999–20 10 by The MathWorks, Inc.

The software described in this document is furnished under a license agreement. The software may be used

or copied only under the terms of the license agreement. No part of this manual may be photocopied or

reproduced in any form without prior written consent from The MathW orks, Inc.

FEDERAL ACQUISITION: This provision applies to all acquisitions of the Program and Documentation

by, for, or through the federal government of the United States. By accepting delivery of the Program

or Documentation, the government hereby agrees that this software or documentation qualifies as

commercial computer software or commercial computer software documentation as such terms are used

or defined in FAR 12.212, DFARS Part 227.72, and DFARS 252.227-7014. Accordingly, the terms and

conditions of this Agreement and only those rights specified in this Agreement, shall pertain to and govern

theuse,modification,reproduction,release,performance,display,anddisclosureoftheProgramand

Documentation by the federal government (or other entity acquiring for or through the federal government)

and shall supersede any conflicting contractual terms or conditions. If this License fails to meet the

government’s needs or is inconsistent in any respect with federal procurement law, the government agrees

to return the Program and Docu mentation, unused, to The MathWorks, Inc.

Trademarks

MATLAB and Simulink are registered trademarks of The MathWorks, Inc. See

www.mathworks.com/trademarks for a list of additional trademarks. Other product or brand

names may be trademarks or registered trademarks of their respective holders.

Patents

The MathWorks products are protected by one or more U.S. patents. Please see

www.mathworks.com/patents for more information.

Page 3

Revision History

December 1999 First printing New for MATLAB®5.3 (Release 11)

June 2000 Online only Revised for Version 1.2

December 2000 Online only Revised for Version 1.3

February 2003 Online only Revised for Version 1.4

June 2004 Online only Revised for Version 1.5 (Release 14)

August 2004 Online only Revised for Version 1.6 (Release 14+)

September 2005 Second printing Revised for Version 1.7 (Release 14SP3)

March 2006 Online only Revised for Version 1.8 (Release 2006a)

September 2006 Online only Revised for Version 1.9 (Release 2006b)

March 2007 Third printing Revised for Version 2.0 (Release 2007a)

September 2007 Online only Revised for Version 3.0 (Release 2007b)

March 2008 Online only Revised for Version 3.1 (Release 2008a)

October 2008 Online only Revised for Version 3.2 (Release 2008b)

March 2009 Online only Revised for Version 3.3 (Release 2009a)

September 2009 Online only Revised for Version 3.4 (Release 2009b)

March 2010 Online only Revised for Version 3.5 (Release 2010a)

Page 4

Page 5

Getting Started

1

Product Overview ................................. 1-2

Contents

About Data Servers and Data Service Providers

Supported Data Service Providers

Data Server Connection Requirements

.................... 1-3

................ 1-3

...... 1-3

Communicating with Financial Data Servers

2

Communication Management ....................... 2-2

Communicating with Data Servers

Core Functions

Connecting to the Bloomberg Data Server

Connection Object Properties

How to Retrieve Connection Properties

Example: Retrieving Data on a Security

Disconnecting from Data Servers

................................... 2-2

................... 2-2

............. 2-3

...................... 2-4

................ 2-4

............... 2-5

................... 2-7

Example: Retrieving Bloomberg Data

3

Using blp Methods ................................. 3-2

About This Example

Retrieving Field Data

Retrieving Time Series Data

............................... 3-2

.............................. 3-2

........................ 3-3

v

Page 6

Retrieving Historical Data .......................... 3-3

Datafeed Toolbox Graphical User Interface

4

Introduction ...................................... 4-2

Using the Datafeed Dialog Box

About the Datafeed Dialog Box

Connecting to Data Servers

Retrieving Data

Using the Datafeed Securities Lookup Dialog Box

Setting Overrides

................................... 4-5

................................. 4-8

...................... 4-3

...................... 4-3

......................... 4-4

....... 4-6

Function Reference

5

Bloomberg ........................................ 5-2

Datastream

FactSet

FRED

Haver Analytics

............................................. 5-5

....................................... 5-3

........................................... 5-4

................................... 5-6

vi Contents

Interactive Data Pricing and RemotePlus

Kx Systems

Reuters

........................................ 5-8

........................................... 5-9

............ 5-7

Page 7

Reuters Datascope Tick History .................... 5-10

Reuters Knowledge Direct

Reuters Newscope

Yahoo!

........................................... 5-13

................................. 5-12

.......................... 5-11

Functions — Alphabetical List

6

Examples

A

Communicating with Financial Data Servers ........ A-2

Retrieving Connection Properties

................... A-2

Retrieving Data

................................... A-2

Index

vii

Page 8

viii Contents

Page 9

Getting Started

• “Product Overview” on page 1-2

• “About Data Servers and Da ta Service Providers” on page 1-3

1

Page 10

1 Getting Started

Product Overview

This toolbox, used with the MATLAB®product, effectively turns your

MATLAB workstation into a financial data acquisition terminal. T he toolbox

enables you to:

• Retrieve and analyze a wide variety of security data from financial data

• Access market, time-series, and historical market data in MATLAB.

• Monitor the status and history of each connection to a supported data

• Fetch data fields for multiple securities in a single call.

• Look up security ticker symbols from the toolbox GUI or the MATLAB

servers in MATLAB.

service provider.

command line.

1-2

Page 11

About Data Servers and Data Service Providers

AboutDataServersandDataServiceProviders

In this section...

“Supported Data Service Providers” on page 1-3

“Data Server Connection Requirements” on page 1-3

Supported Data Service Providers

This toolbox supports connections to financial data servers that the following

corporations provide:

• Bloomberg L.P. (

• FactSet Research Systems, Inc. (

• Federal Reserve Economic Data (FRED)

(

http://research.stlouisfed.org/fred2/)

• Haver Analytics (

• Interactive Data Pricing and Reference Data

(

http://www.interactivedata-prd.com/)

• Kx Systems, Inc. (

• Thomson Reuters (

• Yahoo!, Inc. (

http://www.bloomberg.com)

http://www.factset.com)

http://www.haver.com)

http://www.kx.com)

http://www.thomsonreuters.com/)

http://finance.yahoo.com)

Data Server Connection Requirements

To connect to some of these data servers, additional requirements apply.

Additional Software Requirements

The following data service p roviders require you to install proprietary

software on your PC:

• Bloomberg

1-3

Page 12

1 Getting Started

Note You must have a Bloomberg®software licens e for the host on which

the D atafeed Toolbox™ and MATLAB software are running.

• Interactive Data Pricing and Reference Data’s R emote Plus™

• Haver Analytics

• Kx Systems. Inc.

• Reuters

You must have a valid license for required client software on your machine.

If you do not, the following error message appears when you try to connect

toadataserver:

Invalid MEX-file

For more information about how to obtain required software, contact your

data server sales representative.

1-4

Proxy Information Requirements

The following data service providers may require you to specify a proxy host

and proxy port plus a username and password if the user’s site requires

proxy authentication:

• FactSet

• Federal Reserve Economic Data

• Thomson Datastream

• Yahoo!

For information on how to specify these settings, see “Specifying Proxy Server

Settings” in the MATLAB documentation.

FactSet Data Service Requirements

You need a license to use FactSet®FAST technology. For more information,

see the FactSet Web site at

http://www.factset.com.

Page 13

About Data Servers and Data Service Providers

Reuters Data Service Requirements

Configuring Reuters®Connections Using the Reuters Configuration

Editor software. You must use the Reuters Configuration Editor to

configure your connections as follows:

1 In a DOS prompt, set your CLASSPATH environment variable :

set CLASSPATH=%CLASSPATH%; ...

$MATLAB/toolbox/datafeed/datafeed/config_editor.jar

2 Navigate to the Datafeed Toolbox folder:

cd %MATLAB%\toolbox\datafeed\datafeed

3 Enter the followin g command to run the Reuters Configuration Editor:

starteditor

4 Load the sample configuration file.

a Click File > Import > File.

b Select the file

%MATLAB%\toolbox\datafeed\datafeed\sampleconfig.xml.

5 Modify sampleconfig.xml based o n the site-specific settings that you

obtain from Reuters.

6 Define a namespace, a connection, and a session associated with the

connection. The following example adds the session

remoteSession

with the namespace MyNS to the connection list for the connection

remoteConnection.

1-5

Page 14

1 Getting Started

1-6

7 If you are not DACS enabled, disable DACS.

Page 15

About Data Servers and Data Service Providers

a Add the following to your connection configuration:

dacs_CbeEnabled=false

dacs_SbePubEnabled=false

dacs_SbeSubEnabled=false

b If you are running an SSL connection, add the following to your

connection configuration:

dacs_GenerateLocks=false

For more information, see the reuters function reference page.

Troubleshooting Issues with Reuters Configuration Editor. These errors

occur when you attempt to use the Reuters Configuration Editor to configure

connections on a machine on which an XML Parser is not installed.

java com.reuters.rfa.tools.config.editor.ConfigEditor

org.xml.sax.SAXException: System property

org.xml.sax.driver not specified

at org.xml.sax.helpers.XMLReaderFactory.createXMLReader(U nknown

Source)

at com.reuters.rfa.tools.config.editor.rfaConfigRuleDB.rf aConfi

gRuleDB.java:56)

at com.reuters.rfa.tools.config.editor.ConfigEditor.init

(ConfigEditor.java:86)

at (com.reuters.rfa.tools.config.editor.ConfigEditor.

(ConfigEditor.java:61) at

com.reuters.rfa.tools.config.editor.ConfigEditor.main

(ConfigEditor.java:1303)

To address this problem, download an XML parser file, and then include a

path to this file in your

The following example shows how to set your

variable to include the XML parser file

http://xerces.apache.org/xerces-j/index.html):

set CLASSPATH=%CLASSPATH%;...

matlabroot\toolbox\datafeed\datafeed\config_editor.jar;...

c:\xerces.jar

CLASSPATH environment variable.

CLASSPATH environment

C:\xerces.jar (downloaded from

1-7

Page 16

1 Getting Started

Thomson Data Service Requirements

You need the following to connect to Thomson®data servers:

• AlicenseforThomson

• To connect to the Thomson

®

DataWorks®.

®

Datastream®API from the Web, you need a

user name, password, and URL provided by Thomson.

For more information, see the Thomson Web site at

http://www.thomsonreuters.com.

1-8

Page 17

Communicating with

Financial Data S ervers

• “Communication Management” on page 2-2

• “Connection Object Properties” on page 2-4

• “Disconnecting from Data Servers” on page 2-7

2

Page 18

2 Communicating with Financial Data Servers

Communication Management

In this section...

“Communicating with Data Servers” on page 2-2

“Core Functions” on page 2-2

“Connecting to the Bloomberg Data Server” on page 2-3

Communicating with Data Servers

This section uses the Bloomberg financial data server as an example of how to

retrieve data with the Datafeed Toolbox software. You can communicate with

other supported data servers using a similar set of toolbox functions.

Core Functions

The following set of core functions manage communication with each

supported financial data server.

2-2

• To establish a connection to the appropriate data server, use:

- blp

- datastream

- factset

- fred

- haver

- idc

- kx

- reuters

- yahoo

• To retrieve connection properties, use get.

• To terminate a connection, use

close.

Page 19

Communication Management

Connecting to th

This example sho

data server.

Note If you hav

blpapi3.

file

function or ed

ws how to u se the

e not used the

jar

to the MATLAB java classpath. Use the javaaddpath

it your

classpath.txt file.

e Bloomberg Data Server

blp function to connect to the Bloomberg

blp function before you will need to add the

2-3

Page 20

2 Communicating with Financial Data Servers

Connection Object Properties

In this section...

“How to Retrieve Connection Properties” on page 2-4

“Example: Retriev ing Data on a Security” o n page 2-5

The syntax for the Bloomberg V3 connection object constructor is:

b = blp;

How to Retrieve Connection Properties

To retrieve the properties of a connection object, use the get function. This

function returns different values depending upon which data server you are

using.

get(b)

b=

2-4

session: [1x1 com.bloomberglp.blpapi.Session]

ipaddress: 'localhost'

port: 8194.00

You can get the values of the individual properties by using the property

names:

get(b,{'port','session'})

ans =

port: 8194.00

session: [1x1 com.bloomberglp.blpapi.Session]

For example, return just the connection handle with the ipaddress arg u m ent:

ip = get(b,{'ipaddress'})

ip =

localhost

Page 21

Connection Object Properties

Note A single property is not returned as a structure.

Example: Retrieving Data on a Security

Establish a connection, b, to a Bloomberg data server:

b = blp;

Use the blp.timeseries method to return data on a security:

d = timeseries(b,'IBM US Equity','11/16/2009');

d(1:10,:)

ans =

'TRADE' [73409 3.40 ] [127.17] [2802.00]

'TRADE' [73409 3.40 ] [127.05] [ 100.00]

'TRADE' [73409 3.40 ] [127.05] [ 110.00]

'TRADE' [73409 3.40 ] [127.04] [ 100.00]

'TRADE' [73409 3.40 ] [127.04] [ 100.00]

'TRADE' [73409 3.40 ] [127.09] [ 100.00]

'TRADE' [73409 3.40 ] [127.09] [ 100.00]

'TRADE' [73409 3.40 ] [127.09] [ 125.00]

'TRADE' [73409 3.40 ] [127.05] [ 100.00]

'TRADE' [73409 3.40 ] [127.05] [ 200.00]

If the final input argument is not a ran g e it must be a whole date value, i.e.

'11/16/2009' but not '11/16/2009 12:30:00' or 730316 but not 730316.5.

The code

timeseries(b,'IBM US Equity', now) will error. Use one of

MATLAB’s rounding functions to ensure a whole date value:

d = timeseries(b,'IBM US Equity',fl

oor(now));

To return data on a particular field for a range of dates, use the blp.history

method:

data = history(b,'IBM US Equity','Last_Price','07/15/99','08/02/99')

data =

730316.00 122.33

730317.00 122.27

2-5

Page 22

2 Communicating with Financial Data Servers

730320.00 120.81

730321.00 115.09

730322.00 115.77

730323.00 111.17

730324.00 112.01

730327.00 110.38

730328.00 113.30

730329.00 115.21

730330.00 112.51

730331.00 112.79

730334.00 109.71

2-6

Page 23

Disconnecting from Data Servers

To close a data server connection and disconnect, use the close function

with the format:

close(b)

You must have previously created the connection object with one of the

connection functions.

Disconnecting from Data Servers

2-7

Page 24

2 Communicating with Financial Data Servers

2-8

Page 25

Example: Retrieving

Bloomberg Data

3

Page 26

3 Example: Retrieving Bloomberg

Using blp Methods

In this section...

“About This Example” on page 3-2

“Retrieving Field Data” on page 3 -2

“Retrieving Time Series Data” on page 3-3

“Retrieving Historical Data” on page 3-3

About This Example

Thefollowingexampleillustratestheuseoftheblp methods to retrieve data

from a B loomberg data server.

Note If you have not used the blp function before you will need to add the

file

blpapi3.jar to the MATL AB java classpath. Use the javaaddpath

function or edit your classpath.txt file.

®

Data

3-2

Retrieving Field Data

The getdata method obtains Bloombe rg field data. Theentiresetoffielddata

provides statistics for all possible securities, but it does not apply universally

to any one security.

Obtaining Data

To obtain data for specific fields of a given security, use the getdata function

with the following syntax:

d = getdata(Connect, Security, Fields)

For example, use the Bloomberg conne ction object c to retrieve the values

of the fields

d = getdata(c,'IBM US Equ ity' , {'Open';'Last_Price'})

d=

Open and Last_Price:

Open: 126.2500

Last_Price: 125.1250

Page 27

Using blp Methods

Retrieving Time Series Data

The timeseries method returns price and volumedataforaparticular

security on a specified date. Use the following command to return time-series

data for a given security and a specific date:

data = timeseries(Connection, Security, Date)

Date

can be a MATLAB date string or serial date number. If the final input

argumentisnotarangeitmustbeawholedatevalue,i.e.

but not '11/16/2009 12:30:00' or 730316 but not 730316.5.Thecode

timeseries(b,'IBM US Equity', now) will error. Use one of MATLAB’s

rounding functions to ensure a whole date value.

To obtain time-series data for the current day, use the alternate form of the

function:

data = timeseries(Connection, Security, floor(now))

'11/16/2009'

To obtain time-series data for IBM using an existing connection c1,enter

the function:

data = timeseries(c1, 'IBM US Equity ', floor(now));

Retrieving Historical Data

Use the history method to obtain historical data for a specific security.

To obtain historical data for a specified field of a particular security, run:

d = history(Connect,Security,Field,FromDate,ToDate)

history

For instructions on determining valid field names, see .

For example, to obtain the closing price for

to August 2, 1999 using the connection

returns data for the date range from FromDate to ToDate.

IBM for the dates July 15, 1999

c1,enter:

data = history(c1, 'IBM U S Equity', 'Last_Price',...

'07/15/99', '08/02/99');

3-3

Page 28

3 Example: Retrieving Bloomberg

®

Data

3-4

Page 29

4

Datafeed Toolbox Graphical

User Interface

• “Introduction” on page 4-2

• “Using the Datafeed Dialog Box” on page 4-3

Page 30

4 Datafeed Toolbox™ Graphical User Interface

Introduction

You can use the Datafeed Toolbox Graphical User Interface (GUI) to connect

to and retrieve information from some supported data service providers.

This GUI consists of two dialog boxes:

• The Datafeed dialog box. U se this dialog box to connect to and retrieve data

from the following service providers:

- Bloomberg

- Interactive Data Pricing and Reference Data’s RemotePlus

- Yahoo!

For more information on how to use this dialog box, see “Using the Datafeed

Dialog Box” on page 4-3.

• The Securities Lookup dial og box. You can use this dialog box to find the

ticker symbol for a security when you know part of the security name. Use

this d i al og box with connections to the following service providers:

®

4-2

- Bloomberg

- Interactive Data Pricing and Reference Data’s RemotePlus

For more information on how to use this dialog box, see “Using the Datafeed

Securities Lookup Dialog Box” on page 4-6.

Page 31

Using the Datafeed Dialog Box

In this section...

“About the Datafeed Dialog Box” on page 4-3

“Connecting to Data Servers” on p age 4-4

“Retrieving Data” on page 4-5

“Using the Datafeed Securities Lookup Dialog Box” on page 4-6

“Setting Overrides” on page 4-8

About the Datafeed Dialog Box

The Datafeed dialog box establishes the connection with the data server

and manages data retrieva l. To display this dialog b ox , enter the

command in the MATLAB Command Window.

The Datafeed dialog box consists of two tabs:

Using the Datafeed Dialog Box

dftool

• The Connection tab establishes communicationwithadataserver. For

more information, see “Connecting to Data Servers” on page 4-4.

• The Data tab specifies the data request. For more information, see

“Retrieving Data” on page 4-5.

• You can also set overrides for the data you retrieve. For more information,

see “Setting Overrides” on page 4-8.

The following figure summarizes how to connect to data servers and retrieve

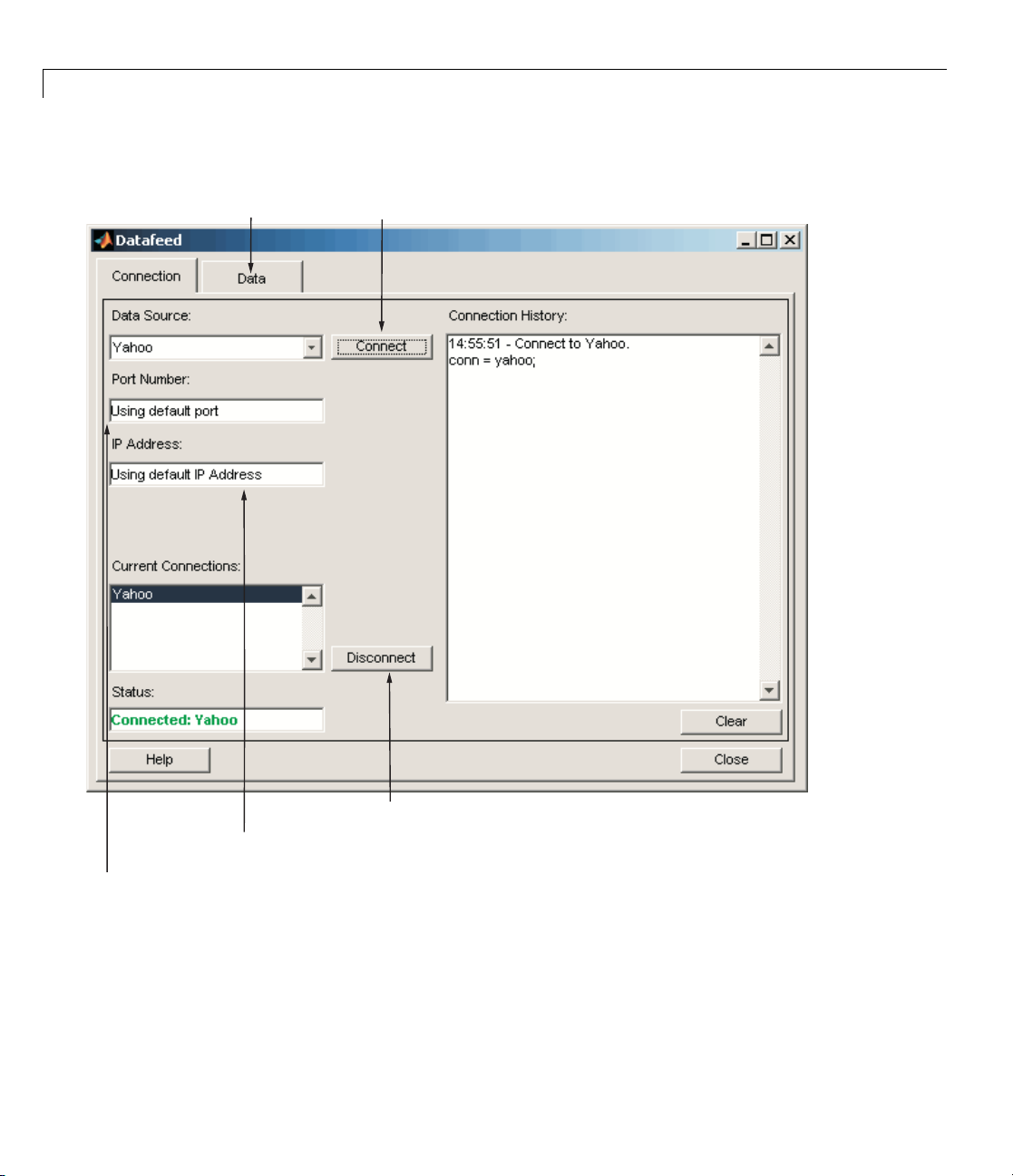

data using the Datafeed dialog box.

4-3

Page 32

4 Datafeed Toolbox™ Graphical User Interface

4. After the connection is made,

click the Data tab to begin

data retrieval.

3. Click to establish a connection to the data server.

1. Enter port number on data server (Bloomberg data

servers only).

The Datafeed Dialog Box

4-4

5. Click to close the highlighted connection.

2. Enter IP address of data server or use the default

values (Bloomberg data servers only).

Connecting to Data Servers

1 Click the Connect button to establish a connection.

Page 33

Using the Datafeed Dialog Box

2 When the Connected message appears in the Status field, click the Data

tab to begin the process of retrieving data from the data server. For more

information, see “Retrieving Data” on page 4-5.

3 Click the Disconnect button to terminate the session highlighted in the

Current Connections box.

For Bloomberg data servers, you must also specify the port number and IP

address of the server:

1 Enter the port number on the data server in the Port Number field.

2 Enter the IP address of the data server in the IP Address field .

3 To establish a connection to the Bloomberg data server, follow steps 1

through 3 above.

Tip You can also connect to the Bloomberg data server by selecting the

Connect button and accepting the default values.

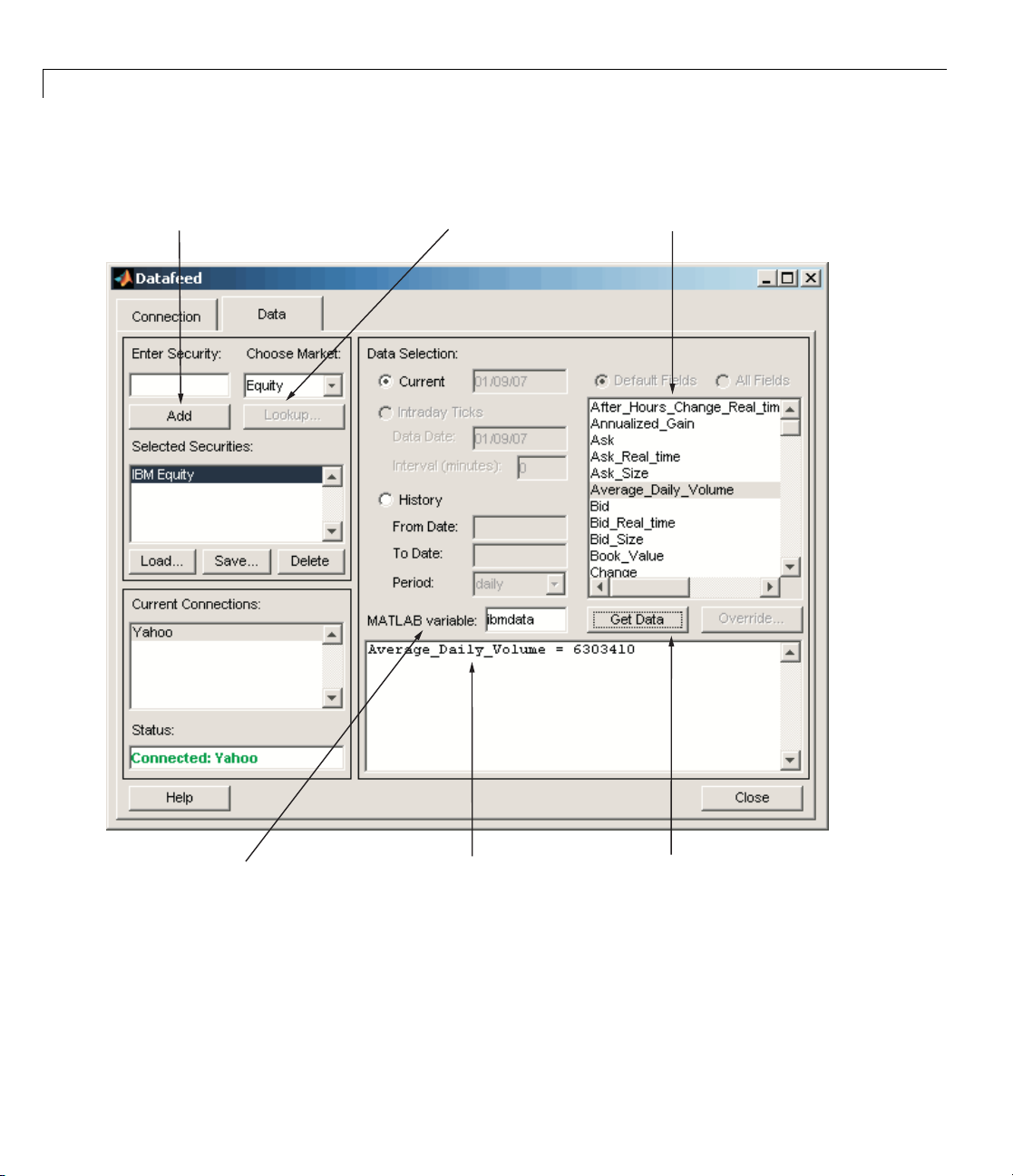

Retrieving Data

The Data tab allows you to retrieve data from the data server as follows:

1 Enter the security symbol in the Enter Security field.

2 IndicatethetypeofdatatoretrieveintheData Selection field.

3 Specify whether you want the default set of data, or the full set:

• Select the Default fields button for the default set of data.

• Select the All fields button for the full set of data.

4 Click the Get Data button to retrieve the data from the data server.

5 (Optional) Click the Override button if you want to set overrides on the

data you request from the data server. For more information, see “Setting

Overrides” on page 4-8.

The following figure summarizes these steps.

4-5

Page 34

4 Datafeed Toolbox™ Graphical User Interface

2. Enter security symbol if known,

or click Add button to add

security to Selected Securities list.

2a. Use to find security symbol, if unknown.

(For Bloomberg and

Interactive Data Pricing and Reference Data

data servers only)

Security fields.

4-6

Variable in MATLAB

workspace.

Using the Datafeed Securities Lookup Dialog Box

When requesting data from Bloomberg or Interactive Data Pricing and

Reference Data’s RemotePlus servers, you can use the Datafee d Securities

Data retrieved

from the connection.

1. Click to retrieve data.

Page 35

Using the Datafeed Dialog Box

Lookup dialog box to obtain the ticker symbol for a given security if you know

only part of the security name.

1 Click the Lookup button on the Datafeed dialog box Data tab. The

Securities Lookup dialog box opens.

2 Specify your choice of market in the Choose Market field.

3 Enter the known part of the security name in the Lookup field.

4 Click Submit. All possible values o f the company name and ticker symbol

corresponding to the security name you sp ecif ied display in the Security

and Symbol list.

5 Select one or more securit ie s from the list, and then click Select.

The s elected securities are added to the Selected Securities list o n the

Data tab.

The following figure summarizes these steps.

4-7

Page 36

4 Datafeed Toolbox™ Graphical User Interface

2. Enter lookup search string.

4. Search results returned from data server.

This field displays all possible

values of company name and ticker

symbol. Select desired securities from

list.

4-8

1. Indicate choice of market.

3. Click to send

request to data

server.

5. Enter selected

securities on Data

tab.

Setting Overrides

To set overrides on retrieved data:

1 Click the Override button. The Override values dialog box opens.

2 Select the field to override from the Override fields selection list.

3 Enter the desired override value in the Override value field.

4 Click Add to add the field to override to the Override field settings list.

5 Click Apply to apply overrides to the current session and keep the Override

values dialog box open, or click OK to apply the overrides and close the

dialog box.

The following figure summarizes these steps.

Page 37

Using the Datafeed Dialog Box

2. Enter desired override value.

3. Click Add to add the field

to the Override field settings list.

Lists data to override.

1. Select field to override.

4a. Apply overrides and close

dialog. Return to previous

dialog box.

4. Apply overrides to current

session.

4-9

Page 38

4 Datafeed Toolbox™ Graphical User Interface

4-10

Page 39

Function Reference

Bloomberg (p. 5-2) Get Bloomberg financial data

Datastream (p. 5-3) Get Thomson Datastream financial

data

FactSet (p. 5-4) Get FactSet financial data

5

FRED (p. 5-5) Get F ederal Reserve Economic Data

(FRED

Haver Analytics (p. 5-6) Get Haver Analytics financial data

Interactive Data Pricing and

RemotePlus (p. 5-7)

Kx Systems (p. 5-8) Get Kx Systems

Reuters (p. 5-9) Get Reuters financial data

Reuters Datascope Tick History

(p. 5-10)

Reuters Knowledge Direct (p. 5-11)

Reuters Newscope (p. 5-12) Retrieve d ata from Reuters

Yahoo! (p. 5-13) Get Yahoo! financial data

Get Interactive Data Pricing and

Reference Data’s RemotePlus

financial data

data

Retrieve data from Reuters

Datascope Tick History file

Establish Reuters Knowledge D irect

connection

Newscope sentiment archive file

®

) financial data

®

, Inc. kdb+ financial

Page 40

5 Function Reference

Bloomberg

blp

blp.close

blp.display

blp.get

blp.getda

blp.hist

blp.realtime

blp.stop

blp.timeseries

ta

ory

Bloomberg V3 communications

server connection

Close connection to Bloomberg V3

data server

Display Bloo

object

Get Bloombe

properties

Current Bl

Bloomberg V3 historical data

Bloomberg V3 realtime data

retrieval

Unsubscribe real time requests for

Bloomberg V3

Bloom

mberg V3 connection

rg V3 connection

oomberg V3 data

berg V3 intraday tick data

5-2

Page 41

Datastream

Datastream

®

datastream

datastream.close

datastream.fetch

datastream.get

datastream.isconnection

Establish connections to Thomson

Datastream API

Close connections to Thomson

Datastream data servers

Request data from Thomson

Datastream data servers

Retrieve properties of Thomson

Datastream connection objects

Verify whether connections to

Thomson Datastream data servers

are valid

5-3

Page 42

5 Function Reference

FactSet

factset

factset.close

factset.fetch

factset.get

factset.isconnection

Establish connections to FactSet

data servers

Close connections to FactSet data

servers

Request data from FactSet data

servers

Retrieve properties of FactSet

connection objects

Verify whether connections to

FactSet data servers are valid

5-4

Page 43

FRED

FRED

®

fred

fred.close

fred.fetch

fred.get

fred.isconnection

Connect to FRED data servers

Close connections to FRED data

servers

Request data from FRED data

servers

Retrieve properties of FRED

connection objects

Verify whether connections to FRED

data servers are valid

5-5

Page 44

5 Function Reference

Haver Analytics

haver

haver.aggregation

haver.close

haver.fetch

haver.get

haver.info

haver.isconnection

haver.nextinfo

havertool

Connect to local Haver Analytics

database

Set Haver Analytics aggregation

mode

Close Haver Analytics database

Request data from Haver Analytics

database

Retrieve properties from Haver

Analytics connection objects

Retrieve information about Haver

Analytics v ariables

Verify whether connections to Haver

Analytics data servers are valid

Retrieve information about next

Haver Analytics variable

Run Haver Analytics graphical u ser

interface (GUI)

5-6

Page 45

Interactive Data Pricing and RemotePlus

Interactive Data Pricing and RemotePlus™

idc

idc.close

idc.fetch

idc.get

idc.isconnection

Connect to Interactive Data Pricing

and Reference Data’s RemotePlus

data servers

Close connections to Interactive

Data Pricing and Reference Data’s

RemotePlus data servers

Request data from Interactive

Data Pricing and Reference Data’s

RemotePlus data servers

Retrieve properties of Interactive

Data Pricing and Reference Data’s

RemotePlus connection objects

Verify whether connections to

Interactive Data Pricing and

Reference Data’s RemotePlus data

servers are valid

5-7

Page 46

5 Function Reference

Kx Systems

kx

kx.close

kx.exec

kx.fetch

kx.get

kx.insert

kx.isconnection

kx.tables

Connect to Kx Systems, Inc. kdb+

databases

Close connections to Kx Systems,

Inc. kdb+ databases

Run Kx Systems, Inc. kdb+

commands

Request data from Kx Systems, Inc.

kdb+ databases

Retrieve Kx Systems, Inc. kdb+

connection o bject properties

WritedatatoKxSystems,Inc. kdb+

databases

Verify whether connections to Kx

Systems, Inc. kdb+ databases are

valid

Retrieve table names from Kx

Systems, Inc. kdb+ databases

5-8

Page 47

Reuters

Reuters

®

reuters

reuters.close

reuters.fetch

reuters.get

reuters.history

reuters.stop

Create Reuters sessions

Release connections to Reuters data

servers

Request data from Reuters data

servers

Retrieve properties of Reuters

session objects

Request data from Reuters Time

Series One

Unsubscr

ibe securities

5-9

Page 48

5 Function Reference

Reuters Datascope Tick History

rdth

rdth.close

rdth.fetch

rdth.get

rdth.isconnection

rdthloader

Connect to Reuters Datascope Tick

History

Close Reuters Datascope Tick

History connection

Request Reuters Datascope Tick

History data

Get Reuters Datascope Tick History

connection properties

Verify whether Reuters Datascope

Tick History connections are valid

Retrieve data from Reuters

Datascope Tick History file

5-10

Page 49

Reuters Knowledge Direct

Reuters®Knowledge Direct

rkd

rkd.close

rkd.fetch

rkd.get

rkd.iscon

nection

Establish Reuters Knowledge D irect

connection

Close Reuters Knowledge Direct

connection

Request Reut

data

Get propert

Data connec

Verify whe

Data conne

ers Knowledge Direct

ies of Reuters Knowledge

tion

ther Reuters Knowledge

ctions are valid

5-11

Page 50

5 Function Reference

Reuters Newscope

rnseloader

Retrieve data from Reuters

Newscope sentiment archive file

5-12

Page 51

Yahoo!

Yaho o !

®

yahoo

yahoo.close

yahoo.fetch

yahoo.get

yahoo.isconnection

Connect to Yahoo! data servers

Close connections to Yahoo! data

servers

Request data from Yahoo! data

servers

Retrieve properties of Yahoo!

connection objects

Verify whether connections to Yahoo!

data servers are valid

5-13

Page 52

5 Function Reference

5-14

Page 53

Functions — Alphabetical

List

6

Page 54

bloomberg

Purpose Connect to Bloomberg data servers

bloomberg is not recommended. Use blp instead.

Syntax c = bloomberg

Description c = bloomberg establishes a connection, c, to a Bloomberg data server.

It uses port number

when you installed the Bloomberg software on your machine.

Examples Establish a connection, c, to a Bloomberg data server:

c = bloomberg

See Also bloomberg.close, bloomberg.fetch, bloomberg.get,

bloomberg.isconnection

8194 and the default internet address provided

6-2

Page 55

bloomberg.close

Purpose Close connections to Bloomberg data servers

bloomberg is not recommended. Use blp instead.

Syntax close(Connect)

Arguments

Connect

Description close(Connect) closes the connection to the Bloomberg data server.

Examples Establish a Bloomberg connection c:

c = bloomberg

Close this connection:

Bloomberg connection object created with the

bloomberg function.

close(c)

See Also bloomberg

6-3

Page 56

bloomberg.fetch

Purpose Request data from Bloomberg data servers

bloomberg.fetch is not recommended. Use blp.getdata,

blp.history, blp.realtime,orblp.timeseries instead.

Syntax data = fetch(Connect, 'Security')

data = fetch(Connect, 'Security', 'HEADER', 'Flag', 'Ident')

data = fetch(Connect, 'Security', 'GETDATA', 'Fields',

'Override', 'Values', 'Ident')

data = fetch(Connect, 'Security', 'TIMESERIES', 'Date',

'Minutes', 'TickField')

data = fetch(Connect, 'Security', 'HISTORY', 'Fields',

'FromDate', 'ToDate', 'Period' , 'Currency', 'Ident')

ticker = fetch(Connect, 'SearchString', 'LOOKUP', 'Market')

data = fetch(Connect, 'Security', 'REALTIME', 'Fields',

'MATLABProg')

data = fetch(Connect, 'Security', 'STOP')

Description For a given security, fetch returns header (default), current,

time-series, real time, and historical data via a connection to a

Bloomberg data server.

6-4

data = fetch(Connect, 'Security') fills the header fields with data

from the most recent date with a bid, ask, or trade.

data = fetch(Connect, 'Security', 'HEADER', 'Flag',

'Ident')

for the specified security type identifiers, based upon the value of

• If

returns data for the most recent date of each individual field

Flag.

'Flag' is 'DEFAULT', fetch fills the header fields with data from

the most recent date with a bid, ask, or trade. Alternatively, you

could use the command

• If

'Flag' is 'TODAY', fetch returns the header field data with data

data = fetch(Connect,'Security').

from today only.

• If

'Flag' is 'ENHANCED', fetch returns the header field data for the

most recent date of each individual field. In this case, for example,

the bid and ask group fields c ou ld come from different dates.

Page 57

bloomberg.fetch

data = fetch(Connect, 'Security', 'GETDATA', 'Fields',

'Override', 'Values', 'Ident')

for the specified fields of the indicated security. You can further specify

the data with the optional

Override, Values and Ident arguments.

Note If a call to the fetch function with the GETDAT A argument

encounters an invalid security in a list of securities to retrieve, it

returns

data = fetch(Connect, 'Security', 'TIMESERIES', 'Date',

'Minutes', 'TickField')

NaN data for the invalid security’s fields.

returns the tick data for a single security

for the specified date. You can further specify data with the optional

Minutes and TickField arguments. If there is no data found in the

specified range,

fetch returns an empty matrix.

returns the current market data

You can specify

TickField = 'Trade' or TickField = 1 returns d ata for ticks of type

Trade. The function dftool('ticktypes') returns the lis t of intraday

tick fields.

TickField as a string or numeric value. For example,

fetch returns intraday tick data requested with an interval

with the following columns:

• Time

• Open

• High

• Low

• Value of last tick

• Volume total value of ticks

• Total value of ticks for the time range

• Number of ticks

fetch fun ction returns columns 7 and 8 only if they make sense for

The

the requested field.

6-5

Page 58

bloomberg.fetch

For today’s tick data, enter the command:

For today’s trade time series aggregated into five-minute intervals,

enter:

data = fetch(Connect, 'Security', 'HISTORY', 'Fields',

'FromDate', 'ToDate', 'Period', 'Currency', 'Ident')

historical data for the specified field for the date range

ToDate. You can set the time period with the optional Period argument

to return a more specific data set. You can further specify returned data

by appending the

Note If a call to the fetch function with the HISTORY argument

encounters an invalid security in a list of securities to retrieve, it

returns no data for any securities in the list.

data = fetch(Connect,'Security', 'TIMESERIES', now)

data = fetch(Connect,'Security','TIMESERIES', ...

now, 5, 'Trade')

returns

FromDate to

Currency or Ident argument.

6-6

ticker = fetch(Connect, 'SearchString', 'LOOKUP', 'Market')

uses SearchSt ring to find the ticker symbol f or a security trading in a

designated market. The output

ticker is a column vector of possible

ticker values.

Note If you supply Ident without a period or currency, enter [] for

the missing values.

data = fetch(Connect, 'Security', 'REALTIME', 'Fields',

'MATLABProg')

subscribes to a given security or list of securities,

requesting the indicated fields, and runs any specified MATLAB

Page 59

Arguments

bloomberg.fetch

function. See pricevol, showtrades,orstockticker for information

on the data returned by asynchronous Bloomberg events.

data = fetch(Connect, 'Security', 'STOP') unsubscribes the list

of securities from processing Bloomberg real-time events.

Connect

'Security'

'Flag'

'Currency'

'Ident'

Bloomberg connection object cre ate d with the bloomberg function.

A MATLAB string containing the name of a security, or a cell array of

strings containing a list of securities, specified in a format recognizable by

the B loomberg server. You can substitute a

CUSIP number for a security

name as needed. You can only call a single security when using the

TIMESERIES flag as well.

Note This argument is case sensitive.

AMATLABstringindicatingthedatesfor which to retrieve data. Possible

values are:

•

DEFAULT: Data from most recent bid, ask, or trade. If you do not specify

a

Flag value, fetch uses the default value of 'DEFAULT'.

TODAY: Today’s data only.

•

ENHANCED: Data from most recent date of each individual field.

•

(Optional) Currency in which the fetc h function returns historical data.

A list of valid currenciesappearsinthefile

Default =

[].

@bloomberg/bbfields.mat.

(Optional) Security type identifier. A list of valid security type identifiers

appears in the file

@bloomberg/bbfields.mat.Default=[].

6-7

Page 60

bloomberg.fetch

'Fields'

'Override'

'Values'

'Date'

'Minutes'

'TickField'

'FromDate'

'ToDate'

'Period'

A MATLAB string or cell array of strings specifying specific fields for

which you request data. A list of valid field names appears in the file

@bloomberg/bbfields.mat. The variable bbfieldnames contains the list

of field names. D efault =

[].

(Optional) String or cell array of strings containing override field list.

Default =

[].

(Optional) String or cell array of strings containing override field values.

Date string, serial date number, or cell array of dates that specifies dates

for the time-series data. Specify

now to retrieve today’s time-series data.

(Optional) Numeric value for tick interval in minutes.

(Optional) You can specify a string or numeric value for this field. For

example,

of type

TickField = 'Trade' or TickField = 1 return data for ticks

Trade.Usethecommanddftool('ticktypes') to return the

list of intraday tick fields.

Beginning date for historical data.

Note You can specify dates in any of the formats supported by datestr

and datenum that display a year, month, and day.

End date for historical data.

(Optional) Period of the data. A MATLAB three-part string w ith the

format:

6-8

'Frequency Days Data'

Frequency

•

d: Daily (default)

w:Weekly

•

m:Monthly

•

q:Quarterly

•

Values:

Page 61

bloomberg.fetch

• s: Semiannually

y:Yearly

•

Days Values:

•

o: Omit all days for which there is no data (default)

i: Include all trading days

•

a: Include all calendar days

•

Data Values:

•

b: Report missing data using Bloomberg (default)

s: Show missing data as last found value

•

n: Report missing data as NaN

•

For example, 'dan' returns daily data for all calendar days, reporting

missing values as

value.

NaN.Ifavalueisunspecified,fetch returns a default

'Currency'

Note If you do not specify a value for Period, fetch uses default values.

(Optional) Currency type. The file @bloomberg/bbfields.mat lists

supported currencies.

6-9

Page 62

bloomberg.fetch

'Market'

A MATLAB string indicating the market in which a particular security

trades. Possible values are:

•

Comdty: (Commodities)

Corp: (Corporate bonds)

•

Equity:(Equities)

•

Govt: (Government bonds)

•

Index:(Indexes)

•

M-Mkt:(MoneyMarketsecurities)

•

Mtge: Mortgage-backed securities)

•

Muni: (Municipal bonds)

•

Pfd: (Preferred stocks)

•

'MATLABProg'

A string that is the name of any valid MATLAB program.

Examples Retrieving Header Data

Retrieve header data for a United States equity with ticker ABC:

D = fetch(C,'ABC US Equit y')

6-10

Retrieving Opening and Closing Prices

Retrieve the opening and closing prices:

D = fetch(C,'ABC US Equit y',' GETDATA',...

{'Last_Price';'Open'})

Retrieving Override Fields

Retrieve the requested fields, given override fields and values:

D = fetch(C, '3358ABCD4 Corp', 'GETDATA',...

Page 63

bloomberg.fetch

{'YLD_YTM_ASK', 'ASK', 'OAS_SPREAD_ASK', 'OAS_VOL_ASK'},...

{'PX_ASK', 'OAS_VOL_ASK'}, {'99.125000', '14.000000'})

Retrieving Time Series Data

Retrieve today’s time series:

D = fetch(C, 'ABC US Equity', 'TIMESERIES', now)

Retrieving Time Series Data, Aggregated into Time Intervals

Retrieve today’s trade time series for the given security, aggregated

into five-minute intervals:

D = fetch(C, 'ABC US Equity', 'TIMESERIES', now, 5,'Trade')

Retrieving Time Series Default C losing Price

Retrieve the closing price for the given dates, using the default period

of the data:

D = fetch(C, 'ABC US Equity', 'HISTORY', 'Last_Price', ...

'8/01/99', '8/10/99')

Retrieving Monthly Closing Price

Retrieve the monthly closing price for the specified dates:

D = fetch(C, 'ABC US Equity', 'HISTORY', 'Last_Price', ...

'8/01/99', '9/30/00', 'm')

See Also bloomberg, bloomberg.close, bloomberg.get,

bloomberg.isconnection

6-11

Page 64

bloomberg.get

Purpose Retrieve Bloomberg connection object properties

bloomberg.get is not recommended. Use blp.get instead.

Syntax value = get(Connect, 'PropertyName')

value = get(Connect)

Arguments

Connect

Bloomberg connection object created with the

bloomberg function.

PropertyName

(Optional)AMATLABstringorcellarrayofstrings

containing property names. Property names are:

•

'Connection'

• 'IPAddress'

• 'Port'

• 'Socket'

• 'Version'

Description value = get(Connect, 'PropertyName') returns a MATLAB

structure containing the value of the specified properties for the

Bloomberg connection o bject.

value = get(Connect) returns the value for all properties.

Examples Establish a connection, c, to a Bloomberg data server:

c = bloomberg

Retrieve this connection’s properties:

p = get(c, {'Port', 'IPAddress'})

p=

port: 8194

6-12

Page 65

ipaddress: 111.222.33.444

See Also bloomberg, bloomberg.close, bloomberg.fetch,

bloomberg.isconnection

bloomberg.get

6-13

Page 66

bloomberg.getdata

Purpose Current Bloomberg data

Syntax d = getdata(b,s,f)

d = getdata(b,s,f,o,ov)

Description d = getdata(b,s,f) returns the data for the fields f for the security

list

s. This method uses the Bloomberg ActiveX

not support overrides. For more robust functionality, refer to the

bloomberg.fetch method.

d = getdata(b,s,f,o,ov) returns the data for the fields f for the

security list

values,

s using the override fields o with corresponding override

ov.

®

interface and does

Examples The command

d = getdata(c,'ABC US Equ ity' ,{'LAST_PRICE';'OPEN'})

returns the today’s current and open price of the given security.

The command

d = getdata(c,'3358ABCD4 Corp',...

{'YLD_YTM_ASK','ASK','OAS_SPREAD_ASK','OAS_VOL_ASK'},...

{'ASK','OAS_VOL_ASK'},{'99.125000','14.000000'})

returns the requested fields given override fields and values.

See Also bloomberg.fetch, bloomberg.history, bl oomberg.lookup,

bloomberg.realtime, bloomberg.timeseries

6-14

Page 67

bloomberg.history

Purpose Historical Bloomberg data

bloomberg.history is not recommended. Use blp.history instead.

Syntax d = history(c,s,f,fromdate,todate)

d = history(c,s,f,fromdate,todate,per)

d = history(c,s,f,fromdate,todate,per,cur)

Description d = history(c,s,f,fromdate,todate) returns the historical data for

the security list

This method uses the Bloomberg ActiveX interface. For more robust

functionality, refer to the

d = history(c,s,f,fromdate,todate,per) returns the historical

data for the field,

period of the data:

s for the fields f for the dates fromdate to todate.

bloomberg.fetch method.

f, for the dates fromdate to todate. per specifies the

'd'

'w'

'm'

'q'

'y'

'o'

'i'

'a'

'b'

's'

'n'

For example,

reporting missing data as

Daily.

Weekly.

Monthly.

Quarterly.

Yearly.

Omit all days for which there is no data.

Include all trading days.

Include all calendar days.

Report missing data u sing Bloomberg default.

Show missing data as last found value.

Report missing data as Nan.

per = 'dan' returns daily data for all calendar days

NaN’s. per = ' n' returns the data using the

default periodicity and default calendar reporting missing data as

If you do not specify

per, the method uses default period for the data.

NaN’s.

6-15

Page 68

bloomberg.history

d = history(c,s,f,fromdate,todate,per,cur) returns the

historical data for the security list

fromdate to todate based on the given currency, cur.Loadthefile

bloomberg/bbfields to see the list of supported currencies.

Examples Example 1

The command

d = history(c,'ABC US Equ ity' ,'LAST_PRICE','8/01/99',...

'8/10/99')

returns the closing price for the given dates for the given security using

the default period of the data.

Example 2

The command

D = HISTORY(c,'ABC US Equ ity' ,'LAST_PRICE','8/01/99',...

'8/10/99','m')

s for the fields f for the dates

6-16

returns the monthly closing price for the given dates for the given

security.

Example 3

The command

D = HISTORY(c,'ABC US Equ ity' ,'LAST_PRICE','8/01/99',...

'8/10/99','m','USD')

returns the monthly closing price converted to US dollars for the given

dates for the given security.

Example 4

The command

D = HISTORY(c,'ABC US Equ ity' ,'LAST_PRICE','8/01/99',...

'8/10/99',[],'USD')

Page 69

bloomberg.history

returns the closing p rice converted t o US dollars for the given dates for

the g iven security using the default period of the data.

6-17

Page 70

bloomberg.isconnection

Purpose Verify whether con ne ctions to Bloomberg data servers are valid

bloomberg is not recommended. Use blp instead.

Syntax x = isconnection(Connect)

Arguments

Connect

Description x = isconnection(Connect) returns x=1iftheconnectiontothe

Bloomberg data server is valid, and

Examples Establish a connection, c, to a Bloomberg data server:

c = bloomberg

Verify that c is a valid connection:

Bloomberg connection object created with the

bloomberg function.

x=0otherwise.

x = isconnection(c)

x=1

See Also bloomberg, bloomberg.close, bloomberg.fetc h, bloomberg.get

6-18

Page 71

bloomberg.isfield

Purpose Verify if valid Bloomberg field

bloomberg is not recommended. Use blp instead.

Syntax x = isfield(b,f)

Description x = isfield(b,f) returns true if specified field, f, is a valid B loomberg

field and false otherwise.

Bloomberg connection handle.

Examples x = isfield(b,{'LAST_PRICE','VOLUME','OPEN','HIGH'})

returns

x= 1111

See Also bloomberg.close, bloomberg.fetch, bloomberg.get,

bloomberg.isconnection

f can be a cell array of strings. b is the

6-19

Page 72

bloomberg.lookup

Purpose Bloomberg security search

bloomberg is not recommended. Use blp instead.

Syntax d = lookup(b,s,market)

Description d = lookup(b,s,market) returns the list of matching securities given

the security search string

Bloomberg ActiveX interface.

Examples The command

D = LOOKUP(C,'Intl Bus Ma c',' Equity')

returns the securities along with their ticker symbols matching the

search string

types are:

•

Comdty: (Commodities)

'Intl Bus Mac' for the Equity market. Valid market

s and market m. This method uses the

Corp: (Corporate bonds)

•

Equity:(Equities)

•

Govt: (Government bonds)

•

Index:(Indexes)

•

M-Mkt: (Money Market securities)

•

Mtge: Mortgage-backed securities)

•

Muni: (Municipal bonds)

•

Pfd: (Preferred stocks)

•

See Also bloomberg.fetch, bloomberg.getdata

6-20

Page 73

bloomberg.realtime

Purpose Bloomberg realtime data retrieval

bloomberg.realtime is not recommended. Use blp.realtime instead.

Syntax realtime(c,s,f,api)

Description realtime(c,s,f,api) subscribes to a given security or list of securities

s requesting the fields f and runs the specified function by api.Seethe

function

by asynchronous Bloomberg events.

Examples The command

subscribes to the security ABC US Equity requesting the fields

Last_Trade and Volume to update in realtime running the function

stockticker.

bloomberg.showtrades for information on the data returned

realtime(c,'ABC US Equity',{'Last_Trade','Volume'},...

'stockticker')

See Also bloomberg.fetch, bloomberg.getda ta, bloomberg.pricevol,

bloomberg.stop, bloomberg.stockticker, bloomberg.showtrades

6-21

Page 74

bloomberg.pricevol

Purpose Price and volume (demonstration)

bloomberg is not recommended. Use blp instead.

Syntax pricevol(InputList)

Arguments

InputList

Description pricevol(InputList) demonstrates the Bloomberg real-time data

import functionality, where

described in the following table.

InputList is an input list of elements as

Fields from which you request

real-time data.

InputList(1) =

COM.Bloomberg.Data.1

InputList(2) = 1

InputList(3) = ('Security')

InputList(4) = 1

InputList(5) = 2

InputList(6) = {[43.58]}

InputList(7) = 0

InputList(8)

InputList(9) = 'Data'

The input argument

to process real-time events.

InputList(8) contains the information required

Bloomberg handle

Event ID

Security string

Cookie

Field number ID

Return data for the given tick

Status

Structure containing the previous

fields

Event type

Examples Display the most recent Trade and Volume values in a figure window

and show the most recent trade with volumes:

b = bloomberg;

d = fetch(b, 'ABC US Equity', 'REALTIME', ...

6-22

Page 75

bloomberg.pricevol

{'Last_Trade', 'Volume'}, 'pricevol');

See Also bloomberg.showtrades, bloomberg.stockticker

6-23

Page 76

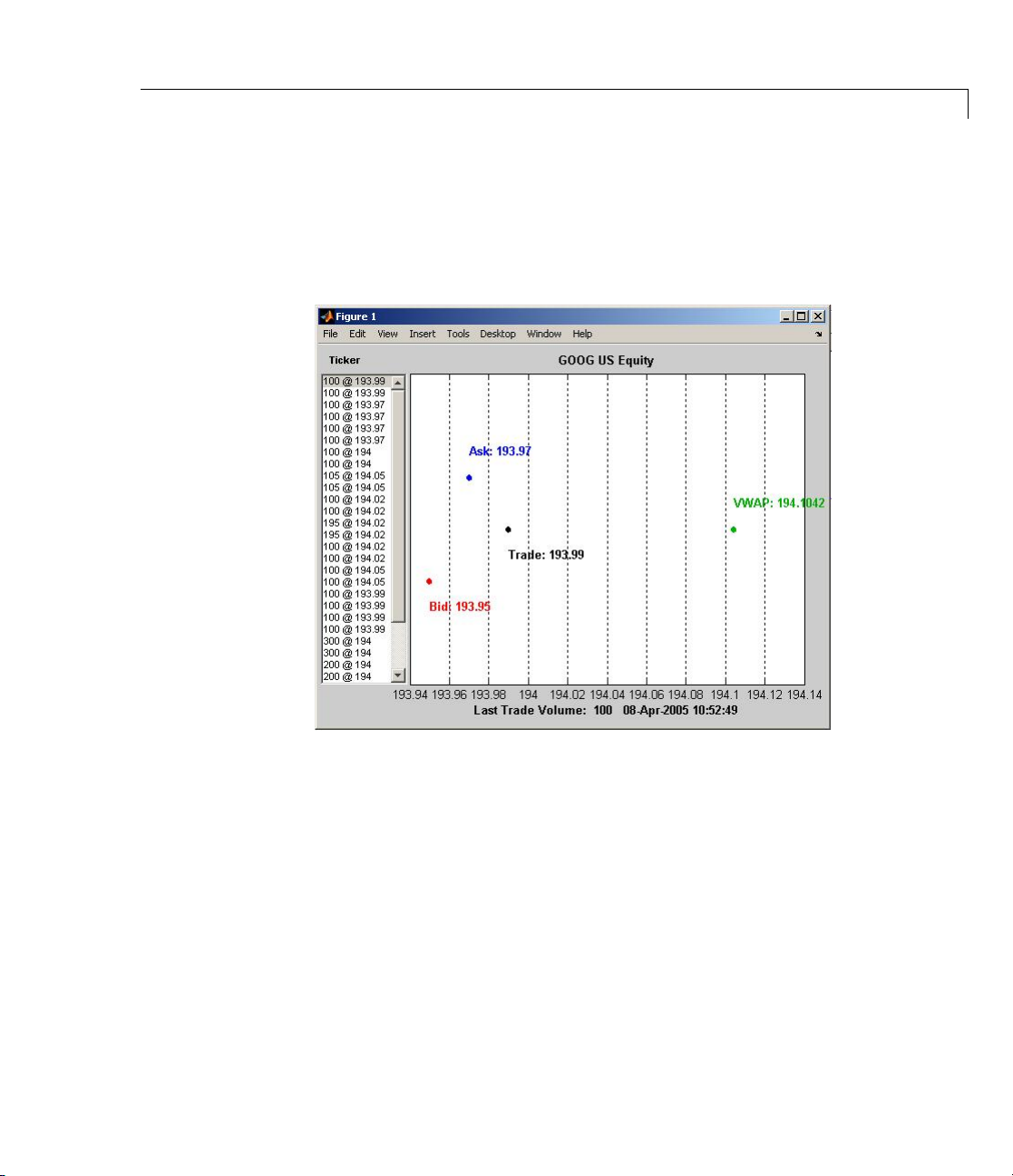

bloomberg.showtrades

Purpose Recent trade data (demonstration)

bloomberg is not recommended. Use blp instead.

Syntax showtrades(InputList)

Arguments

InputList

Description showtrades(InputList) demonstrates the Bloomberg real-time data

import functionality, where

described in the following table:

InputList is an input list of elements as

Fields from which you request

real-time data.

InputList(1) =

COM.Bloomberg.Data.1

InputList(2) = 1

InputList(3) = ('Security')

InputList(4) = 1

InputList(5) = 2

InputList(6) = {[43.58]}

InputList(7) = 0

InputList(8)

InputList(9) = 'Data'

The input argument

to process real-time events.

InputList(8) contains the information required

Bloomberg handle

Event ID

Security string

Cookie

Field number ID

Return data for the given tick

Status

Structure containing the above

fields

Event type

Examples Establish a connection, c, to a Bloomberg data server:

c = bloomberg;

6-24

Page 77

bloomberg.showtrades

Display the most recent Trade, Bid, Ask,andVWAP (volume-weighted

adjusted price), and a list of the most recent trades with volu m es:

d = fetch(c, 'GOOG US Equity', 'REALTIME', ...

{'Last_Trade','Bid','Ask','Volume','VWAP'},'showtrades');

See Also bloomberg.pricevol, bloomberg.stockticker

6-25

Page 78

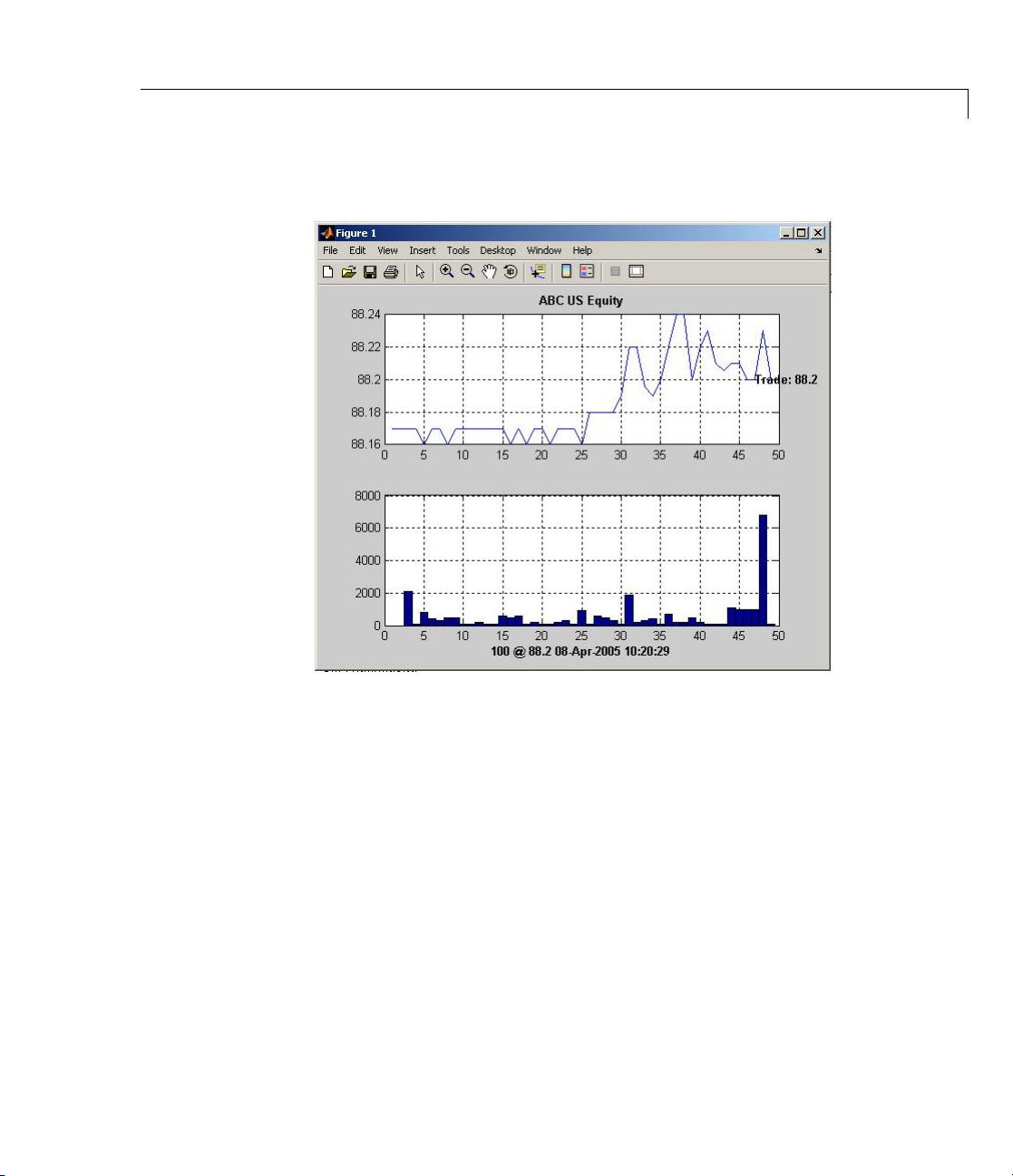

bloomberg.stockticker

Purpose Trades with volumes (demonstration)

bloomberg is not recommended. Use blp instead.

Syntax stockticker(InputList)

Arguments

InputList

Description stockticker(InputList) demonstrates the Bloomberg real-time data

import functionality, where

described in the following table.

InputList is an input list of elements as

Fields from which you request

real-time data.

InputList(1) =

COM.Bloomberg.Data.1

InputList(2) = 1

InputList(3) = ('Security')

InputList(4) = 1

InputList(5) = 2

InputList(6) = {[43.58]}

InputList(7) = 0

InputList(8)

Bloomberg handle

Event ID

Security string

Cookie

Field number ID

Return data for the given tick

Status

Structure containing the above

fields

InputList(9) = 'Data'

The input argument

InputList(8) contains the information required

Event type

to process real-time events.

Examples Retrieve a list of trades with volumes for each requested security:

b = bloomberg;

d = fetch(b, {'IBM US Equity', 'EMC US Equity', 'NTAP US Equity'}, ...

'REALTIME', {'Last_Trade', 'Volume'}, 'stockticker');

6-26

Page 79

bloomberg.stockticker

** EMC US Equity ** 0 @ 12.65 08-Apr-2005 10:24:57

** IBM US Equity ** 0 @ 88.17 08-Apr-2005 10:24:57

** NTAP US Equity ** 0 @ 29.02 08-Apr-2005 10:24:57

** EMC US Equity ** 200 @ 12.66 08-Apr-2005 10:24:58

** EMC US Equity ** 1400 @ 12.65 08-Apr-2005 10:24:58

** EMC US Equity ** 3100 @ 12.66 08-Apr-2005 10:25:00

** IBM US Equity ** 1300 @ 88.17 08-Apr-2005 10:25:00

.

.

.

See Also bloomberg.pricevol, bloomberg.showtrades

6-27

Page 80

bloomberg.stop

Purpose Stop Bloomberg realtime data retrieval

bloomberg is not recommended. Use blp instead.

Syntax stop(c,s)

stop(c,s,api)

Description stop(c,s) desubscribes a given security or l ist of securities s.Data

events for the security no longer process.

stop(c,s,api) desubscribes a given security or list of securities s and

unregisters the specified callback

To desubscribe all securities and turn off data event handling, use

close(c).

The Bloomberg connection is now closed.

Examples Example 1

The command

api.

6-28

stop(C,'ABC US Equity')

desubscribes from the security ABC US Equity.

Example 2

The command

stop(C,'ABC US Equity','stockticker')

desubscribes from the security ABC US Equity and turns off data event

handling by the function

stockticker.

Example 3

The command

STOP(C,'','STOCKTICKER')

turns off data event handling by the function stockticker.

Page 81

bloomberg.stop

See Also bloomberg.fetch, bloomberg.getda ta, bloomberg.pricevol,

bloomberg.realtime, bloomberg.st ockt icker,

bloomberg.showtrades

6-29

Page 82

bloomberg.timeseries

Purpose Bloombergintradaytickdata

bloomberg.timeseries is not recom m e nd ed. Use blp.timeseries

instead.

Syntax d = timeseries(c,s,f,t)

d = timeseries(c,s,f,{startdate,enddate})

d = timeseries(c,s,f,t,b)

Description d = timeseries(c,s,f,t) returns the tick data for the security s for

the date

robust functionality, refer to the

d = timeseries(c,s,f,{startdate,enddate}) returns the tick data

for the security

d = timeseries(c,s,f,t,b) returns the tick data for the security s for

the date

requested with an interval is returned with the columns representing

Time, Open, High, Low, Last Price and Volume of the ticks in the bar.

t. This method uses the BloombergActiveX interface. F or more

bloomberg.fetch method.

s for the date range defined by startdate and enddate.

t in intervals of b minutes for the field, f.Intradaytickdata

Examples Example 1

The command

returns today’s time series for the given security with the timestamp

and tick value.

Example 2

The command

returns today’s Last Price series for the given security aggregated into

5-minute intervals minute intervals.

Example 3

The command

6-30

d = timeseries(c,'ABC US Equity','Last Price',floor(now))

d = timeseries(c,'ABC US Equity','Last Price',floor(now),5)

Page 83

bloomberg.timeseries

d = timeseries(c,'ABC US Equity','Last Price',...

{'12/08/2008 00:00:00','12/10/2008 23:59:59.99'},5)

returns the Last Price series for 12/08/2008 and 12/10/2008 for the

given security, aggregated into 5-minute intervals.

See Also bloomberg.fetch, bloomberg.getdata, bloomberg.history

6-31

Page 84

blp

Purpose Bloomberg V3 communications server connection

Syntax c = blp

Description c = blp makes a connection to the local Bloomberg V3 communications

server.

Examples Establish a connection, c, to a Bloomberg data server:

c=blp

See Also blp.close, blp.getdata, blp.his tory, blp.realtime,

blp.timeseries

6-32

Page 85

Purpose Close connection to Bloomberg V3 data server

Syntax close(C)

Description close(C) closes the connection, C, to the Bloomberg V3 session.

blp.close

6-33

Page 86

blp.display

Purpose Display Bloomberg V3 connection object

Syntax disp = display(c)

Description disp = display(c) displays the Bloomberg V3 connection object.

6-34

Page 87

Purpose Get Bloomberg V3 connection properties

Syntax V = get(C,'PropertyName')

V = get(C)

Description V = get(C,'PropertyName') returns the value of the specified

properties for the Bloomberg V3 connection object.

string or cell array of strings containing property names. The property

names are

V = get(C) returns a structure where each field name is the name of a

property of

session, ipaddress,andport.

C an d each field contains the value of th a t property.

'PropertyName' is a

See Also blp.getdata, blp.history, blp.realt ime, blp.timeseries

blp.get

6-35

Page 88

blp.getdata

Purpose Current Bloomberg V3 data

Syntax D = getdata(B,S,F)

D = getdata(B,S,F,O,OV)

Description D = getdata(B,S,F) returns the data for the fields F for the security

list

S for the Bloomberg V3 connection object B

D = getdata(B,S,F,O,OV)

security list

values

S using the override fields O with corresponding override

OV.

returns the data for the fields F for the

Examples D = getdata(C,'ABC US E quit y',{'LAST_PRICE';'OPEN'}) returns

today’s current and open price of the given security.

D = fetch(C,'3358ABCD4

Corp','GETDATA',{'YLD_YTM_ASK','ASK','OAS_SPREAD_ASK','OAS_VOL_ASK'},

{'ASK','OAS_VOL_ASK'},{'99.125000','14.000000'})

requested fields given override fields and values.

returns the

See Also blp, blp.history, blp.realtime, blp.timeseries

6-36

Page 89

blp.history

Purpose Bloomberg V3 historical data

Syntax D = history(S,F,FromDate,ToDate)

D = history(C,S,F,FromDate,ToDate,Per)

D = history(S,F,FromDate,ToDate,Per,Cur)

Description D = history(S,F,FromDate,ToDate) returns the historical data for

the security list

D = history(C,S,F,FromDate,ToDate,Per) returns the historical

data for the field,

the period of the data. For example,

returns daily data for all calendar days reporting missing data as NaN.

Per = {'actual'} returns the data using the default periodicity and

default calendar reporting missing data as

Per are as follows:

Value Time Period

daily

S for the fields F for the dates FromDate to ToDate.

F, for the dates FromDate to ToDate. Per specifies

Per = {'daily','calendar'}

NaN. The possible values of

Daily

weekly

monthly

quarterly

semi_annually

yearly

actual

calendar

fiscal

non_trading_weekdays

all_calendar_days

active_days_only

Weekly

Monthly

Quarterly

Semi annually

Yearly

Anchor date specification

Anchor date specification

Anchor date specification

Non trading weekdays

Return all calendar days

Active trading days only

6-37

Page 90

blp.history

Value Time Period

previous_value

nil_value

D = history(S,F,FromDate,ToDate,Per,Cur) returns the

historical data for the security list

FromDate to ToDate based on the given currency, Cur.Loadthefile

bloomberg/bbfields to see the list of supported currencies.

Examples D = history(C,'ABC US E quit y',...

'LAST_PRICE','8/01/99','8/10/99')

given dates for the given security using the default period of the data.

D = history(C,'ABC US E quit y',...

'LAST_PRICE','8/01/99','8/10/99','monthly')

monthly closing price for the given dates for the given security.

D = history(C,'ABC US E quit y',...

'LAST_PRICE','8/01/99','8/10/99','monthly','USD')

monthly closing price converted to US dollars for the given dates for

the given security.

Fill missing values with previous

values

Fill missing values with NaN

S for the fields F for the dates

returns the closing price for the

returns the

returns the

D = history(C,'ABC US E quit y',...

'LAST_PRICE','8/01/99','8/10/99',

{'daily','actual','all_calendar_days', 'nil_value'},'US D')

returns the daily closing price converted to US dollars for the given

dates for the given security.

D = history(C,'ABC US E quit y',...

'LAST_PRICE','8/01/99','8/10/99',[],'USD')

price conv erted to US dollars for the given dates for the given security

using the default period of the data.

See Also blp, blp.realtime, blp.timeseries

6-38

returns the closing

Page 91

blp.realtime

Purpose Bloomberg V3 realtime data retrieval

Syntax [SUBS,T] = realtime(C,S,F,API)

Description [SUBS,T] = realtime(C,S,F,API) subscribes to a given security or

list of securities

by

API. It returns the subscription list, SUBS and the timer T associated

with the real time callback for the subscriptionlist. Runtheexample

v3showtrades for information on the data returned by asynchronous

Bloomberg events. Type

example.

Examples realtime(C,'ABC US

Equity',{'Last_Trade','Volume'},'v3stockticker')

the security

and Volume to update in realtime while running the

function

v3stockticker.

See Also blp, blp.history, blp.timeseries

S requesting the fields F and runs the specified function

help v3showtrades for information on the

subscribes to

ABC US Equity requesting the fields Last_Trade

6-39

Page 92

blp.stop

Purpose Unsubscribe real time requests for Bloomberg V3

Syntax stop(B,SUBS,T)

stop(B,SUBS,T,S)

Description stop(B,SUBS,T)unsubscribes all real time requests associated with

the Bloomberg connection,

associated with the real time callback for the subscription list.

stop(B,SUBS,T,S)unsubscribes all real time requests associated with

the Bloomberg unsubscribes real time r equests for each security,

the subscription list,

callback for the subscription list.

B, and subscription list, S UBS.T is the timer

SUBS. T is the timer associated with the real time

S,on

6-40

Page 93

blp.timeseries

Purpose Bloomberg V3 intraday tick data

Syntax D = timeseries(C,S,T)

D = timeseries(C,S,{StartDate,EndDate})

D = timeseries(C,S,T,B,F)

Description D = timeseries(C,S,T) returns the raw tick data for the security S

for the date T.

D = timeseries(C,S,{StartDate,EndDate}) returns the raw tick

data for the security

EndDate.

D = timeseries(C,S,T,B,F)returns the tick data for the security S for

the date

requested with an interval is returned with the columns representing

Time, Open, High, Low, Last Price, number of ticks and Volume of

the ticks in the bar.

T in intervals of B minutes for the field, F.Intradaytickdata

Examples D = timeseries(C,'ABC US Equity',FLOOR(NOW)) returns today’s

time series for the given security. The timestamp and tick value are

returned.

S for the date range defined by StartDate and

D = timeseries(C,'ABC US Equity',FLOOR(NOW),5,'Trade')

returns today’s Trade tick series for the given security aggregated into

5 minute intervals.

D = timeseries(C,'ABC US Equity',{'12/08/2008

00:00:00','12/10/2008 23:59:59.99'},5,'Trade')

Trade tick series for 12/08/2008 and 12/10/2008 for the given security

aggregated into 5 minute intervals.

See Also blp, blp.history, blp.realtime

returns the

6-41

Page 94

datastream

Purpose Establish connections to Thomson Datastream API

Syntax Connect = datastream('UserName', 'Password', 'Source', 'URL')

Arguments

'UserName'

'Password'

'Source'

'URL'

Note Thomson assigns the values for you to enter for each argume nt.

EnterallargumentsasMATLABstrings.

User name.

User password.

To connect to the Thomson Datastream API, enter

'Datastream' in this field.

Web URL.

Description Connect = datastream('UserName', 'Password', 'Source',

'URL')

provides access to Thomson Datastream software content.

makes a connection to the Thomson Datastream API, w hich

Examples Establish a connection to the Thomson Datastream API:

Connect = datastream('User1', 'Pass1', 'Datastream', ...

'http://dataworks.thomson.com/Dataworks/Enterprise/1.0')

See Also datastream.close, datastream.fetch, datastream.get,

datastream.isconnection

6-42

Page 95

datastream.close

Purpose Close connections to Thomson Datastream data servers

Syntax close(Connect)

Arguments

Connect

Thomson Datastream connection object created with

the

datastream function.

Description close(Connect) closes a connection to a Thomson Datastream data

server.

See Also datastream

6-43

Page 96

datastream.fetch

Purpose Request data from Thomson Datastream data servers

Syntax data = fetch(Connect, 'Security')

data = fetch(Connect, 'Security', 'Fields')

data = fetch(Connect, 'Security', 'Fields', 'Date')

data = fetch(Connect, 'Security', 'Fields', 'FromDate',

'ToDate')

data = fetch(Connect, 'Security', 'Fields', 'FromDate',

'ToDate', 'Period')

data = fetch(Connect, 'Security', 'Fields', 'FromDate',

'ToDate', 'Period', 'Currency')

Arguments

Connect

'Security'

'Fields'

'Date'

'FromDate'

Thomson Datastream connection

object created with the

datastream function.

MATLAB string containing the

name of a security, or cell array

of strings containing names of

multiple securities. This data

is in a format recognizable by

the Thomson Datastream data

server.

(Optional) MATLAB string or cell

array of strings indicating the

data fields for which to retrieve

data.

(Optional) MATLAB string

indicating a specific calendar date

for which you request data.

(Optional) Start date for historical

data.

6-44

Page 97

datastream.fetch

'ToDate'

(Optional) End date for historical

data. If you specify a value for

'ToDate', 'FromDate' cannot be

an empty value.

Note You can specify dates in

any of the formats supported by

datestr and datenum that show

a year, month, and day.

'Period'

'Currency'

(Optional) Period within a date

range.

•

•

•

Period values are:

'd': daily values

'w':weeklyvalues

'm': monthly values

(Optional) Currency in which

fetch returns the data.

Note You can enter the optional arguments 'Fields', 'FromDate',

'ToDate', 'Period',and'Currenc y' as MATLAB strings or empty

arrays (

[]).

Description data = fetch(Connect, 'Security') returns the default time series

for the indicated security.

data = fetch(Connect, 'Security', 'Fields') returns data for

the specified security and fields.

data = fetch(Connect, 'Security', 'Fields', 'Date') returns

data for the specified secu r ity and fields on a particu lar da t e.

6-45

Page 98

datastream.fetch

data = fetch(Connect, 'Security', 'Fields', 'FromDate',

'ToDate')

indicated date range.

data = fetch(Connect, 'Security', 'Fields', 'FromDate',

'ToDate', 'Period')

with the indicated period.

data = fetch(Connect, 'Security', 'Fields', 'FromDate',

'ToDate', 'Period', 'Currency')

which to report the data.

Note The Thomson Datastream interface returns all data as strings.

For example, it returns

array of strings within the structure. There is no way to determine the

data type from the Datastream

Examples Retrieving Time Series Data

returns data for the specified s ecurity and fields for the

returns instrument data for the g iven range

also specifies the currency in

Price data to the MATLAB workspace as a cell

®

interface.

6-46

Return the trailing one-year price time series for the instrument

'P', which is the default value for the 'Fields' argument using the

command:

data = f

etch(Connect, 'ICI')