Page 1

HP 12C Platinum

Owner’s Handbook

and

Problem-Solving Guide

© Copyright 2003 Hewlett-Packard Development Company, L.P.

Page 2

Introduction

About This Handbook

This HP 12C Platinum Owner’s Handbook and Problem-Solving Guide is

intended to help you get the most out of your investment in your HP 12C

Platinum Programmable Financial Calculator. Although the excitement of

acquiring this powerful financial tool may prompt you to set this handbook aside

and immediately begin “pressing buttons,” in the long run you’ll profit by

reading through this handbook and working through the examples it contains.

Following this introduction is a brief section called Making Financial

Calculations Easy—which shows you that your HP 12C Platinum does just that!

The remainder of this handbook is organized basically into three parts:

z Part I (sections 1 through 7) describes how to use the various financial,

mathematics, statistics, and other functions (except for programming)

provided in the calculator:

z Section 1 is about Getting Started. It tells you how to use the keyboard,

how to do simple arithmetic calculations and chain calculations, and

how to use the storage registers (“memories”).

z Section 2 tells you how to use the percentage and calendar functions.

z Section 3 tells you how to use the simple interest, compound interest,

and amortization functions.

z Section 4 tells you how to do discounted cash flow analysis, bond, and

depreciation calculations.

z Section 5 tells you about miscellaneous operating features such as

Continuous Memory, the display, and special function keys.

z Sections 6 and 7 tell you how to use the statistics, mathematics, and

number-alteration functions.

z Part II (sections 8 through 11) describe how to use the powerful

programming capabilities of the HP 12C Platinum.

z Part III (sections 12 through 16) give you step-by-step solutions to

specialized problems in real estate, lending, savings, investment analysis,

and bonds. Some of these solutions can be done manually, while others

involve running a program. Since the programmed solutions are both selfcontained and step-by-step, you can easily employ them even if you don’t

care to learn how to create your own programs. But if you do start to create

your own programs, look over the programs used in the solutions: they

contain examples of good programming techniques and practices.

2

Page 3

Introduction 3

z The various appendices describe additional details of calculator operation

as well as warranty and service information.

z The Function Key Index and Programming Key Index at the back of the

handbook can be used as a handy page reference to the comprehensive

information inside the manual

Financial Calculations in the United Kingdom

The calculations for most financial problems in the United Kingdom are

identical to the calculations for those problems in the United States – which are

described in this handbook. Certain problems, however, require different

calculation methods in the United Kingdom than in the United States. Refer to

Appendix G for more information.

For More Solutions to Financial Problems

In addition to the specialized solutions found in Sections 12 through 16 of this

handbook, many more are available in the optional HP 12C Platinum Solutions

Handbook. Included are solutions to problems in lending, forecasting, pricing,

statistics, savings, investment analysis, personal finance, securities, Canadian

mortgages, learning curves in manufacturing, and queuing theory. The solutions

handbook is available from your authorized HP dealer.

Page 4

Contents

Introduction ...................................................................................... 2

About This Handbook ..................................................................................... 2

Financial Calculations in the United Kingdom ................................................ 3

For More Solutions to Financial Problems...................................................... 3

Part I: Problem Solving................................................15

Section 1: Getting Started................................................................... 16

Power On and Off......................................................................................... 16

Low-Power Indication ............................................................................. 16

The Keyboard ............................................................................................... 16

Keying in Numbers ................................................................................. 17

Digit Separators...................................................................................... 17

Negative Numbers.................................................................................. 17

Keying in Large Numbers....................................................................... 18

The CLEAR Keys ................................................................................... 18

The RPN and ALG Keys......................................................................... 19

Simple Arithmetic Calculations in RPN Mode............................................... 19

Chain Calculations in RPN Mode ................................................................. 20

Storage Registers......................................................................................... 23

Storing and Recalling Numbers.............................................................. 24

Clearing Storage Registers .................................................................... 25

Storage Register Arithmetic.................................................................... 25

Section 2: Percentage and Calendar Functions............................ 27

Percentage Functions................................................................................... 27

Percentages ........................................................................................... 27

Net amount............................................................................................. 27

Percent Difference.................................................................................. 28

Percent of Total ...................................................................................... 29

Calendar Functions ...................................................................................... 30

Date Format............................................................................................ 30

Future or Past Dates .............................................................................. 31

Number of Days Between Dates ............................................................ 32

Section 3: Basic Financial Functions............................................... 34

The Financial Registers................................................................................ 34

Storing Numbers Into the Financial Registers........................................ 34

Displaying Numbers in the Financial Registers...................................... 34

Clearing the Financial Registers............................................................. 34

Simple Interest Calculations ......................................................................... 35

Financial Calculations and the Cash Flow Diagram ..................................... 36

The Cash Flow Sign Convention ............................................................ 38

The Payment Mode ................................................................................ 38

Generalized Cash Flow Diagrams.......................................................... 39

5

Page 5

6 Contents

Compound Interest Calculations .................................................................. 41

Specifying the Number of Compounding Periods and the Periodic

Interest Rate ........................................................................................... 41

Calculating the Number of Payments or Compounding Periods ............ 41

Calculating the Periodic and Annual Interest Rates............................... 45

Calculating the Present Value ................................................................ 46

Calculating the Payment Amount ........................................................... 48

Calculating the Future Value .................................................................. 49

Odd-Period Calculations......................................................................... 51

Amortization.................................................................................................. 54

Section 4: Additional Financial Functions ...................................... 58

Discounted Cash Flow Analysis: NPV and IRR............................................ 58

Calculating Net Present Value (NPV)..................................................... 59

Calculating Internal Rate of Return (IRR)............................................... 63

Reviewing Cash Flow Entries................................................................. 64

Changing Cash Flow Entries .................................................................. 66

Bond Calculations......................................................................................... 67

Bond Price.............................................................................................. 67

Bond Yield .............................................................................................. 68

Depreciation Calculations............................................................................. 68

Section 5: Additional Operating Features....................................... 70

Continuous Memory ..................................................................................... 70

The Display................................................................................................... 70

Status Indicators..................................................................................... 70

Number Display Formats........................................................................ 71

Scientific Notation Display Format.......................................................... 72

Special Displays ..................................................................................... 73

The

~ Key................................................................................................ 74

The

F Key ............................................................................................... 74

Arithmetic Calculations With Constants.................................................. 75

Recovering From Errors in Digit Entry.................................................... 75

Section 6: Statistics Functions .......................................................... 76

Accumulating Statistics................................................................................. 76

Correcting Accumulated Statistics................................................................ 77

Mean............................................................................................................. 77

Standard Deviation ....................................................................................... 78

Linear Estimation.......................................................................................... 79

Weighted Mean ............................................................................................ 81

Section 7: Mathematics and Number-Alteration Functions ....... 82

One-Number Functions ................................................................................ 82

The Power Function ..................................................................................... 84

Page 6

Contents 7

Part II: Programming....................................................85

Section 8: Programming Basics........................................................ 86

Why Use Programs? .................................................................................... 86

Creating a Program ...................................................................................... 86

Running a Program ...................................................................................... 87

Program Memory.......................................................................................... 88

Identifying Instructions in Program Lines................................................ 89

Displaying Program Lines....................................................................... 90

The

i000 Instruction and Program Line 000..................................... 91

Expanding Program Memory.................................................................. 91

Setting the Calculator to a Particular Program Line ............................... 93

Executing a Program One Line at a Time .................................................... 94

Interrupting Program Execution.................................................................... 95

Pausing During Program Execution ....................................................... 95

Stopping Program Execution .................................................................. 98

Section 9: Branching and Looping................................................. 101

Simple Branching ....................................................................................... 101

Looping....................................................................................................... 101

Conditional Branching ................................................................................ 104

Section 10: Program Editing............................................................. 110

Changing the Instruction in a Program Line............................................... 110

Adding Instructions at the End of a Program.............................................. 111

Adding Instructions Within a Program ........................................................ 112

Adding Instructions by Replacement.................................................... 112

Adding Instructions by Branching ......................................................... 113

Section 11: Multiple Programs......................................................... 117

Storing Another Program............................................................................ 117

Running Another Program.......................................................................... 119

Part III: Solutions........................................................121

Section 12: Real Estate and Lending ............................................. 122

Annual Percentage Rate Calculations With Fees....................................... 122

Price of a Mortgage Traded at a Discount or Premium .............................. 124

Yield of a Mortgage Traded at a Discount or Premium .............................. 125

The Rent or Buy Decision........................................................................... 127

Deferred Annuities...................................................................................... 131

Section 13: Investment Analysis..................................................... 134

Partial-Year Depreciation ........................................................................... 134

Straight-Line Depreciation .................................................................... 134

Declining-Balance Depreciation ........................................................... 137

Sum-of-the-Years-Digits Depreciation.................................................. 139

Full- and Partial-Year Depreciation with Crossover.................................... 141

Excess Depreciation................................................................................... 145

Modified Internal Rate of Return................................................................. 145

Page 7

8 Contents

Section 14: Leasing............................................................................ 148

Advance Payments..................................................................................... 148

Solving For Payment ............................................................................ 148

Solving for Yield.................................................................................... 150

Advance Payments With Residual ............................................................. 152

Solving for Payment ............................................................................. 152

Solving For Yield .................................................................................. 154

Section 15: Savings............................................................................ 156

Nominal Rate Converted to Effective Rate................................................. 156

Effective Rate Converted to Nominal Rate................................................. 157

Nominal Rate Converted to Continuous Effective Rate.............................. 158

Section 16: Bonds............................................................................... 159

30/360 Day Basis Bonds ............................................................................ 159

Annual Coupon Bonds................................................................................ 161

Appendixes ................................................................ 165

Appendix A: RPN and the Stack .................................................... 166

Getting Numbers Into the Stack: The \ Key ......................................... 167

Termination of Digit Entry ..................................................................... 168

Stack Lift............................................................................................... 168

Rearranging Numbers in the Stack ............................................................ 168

The

~ Key........................................................................................ 168

The

d Key.......................................................................................... 168

One-Number Functions and the Stack ....................................................... 169

Two-Number Functions and the Stack ....................................................... 169

Mathematics Functions......................................................................... 169

Percentage Functions........................................................................... 170

Calendar and Financial Functions.............................................................. 171

The LAST X Register and the

Chain Calculations in RPN Mode ............................................................... 172

Arithmetic Calculations with Constants ...................................................... 173

Appendix B: Algebraic Mode (ALG) .............................................. 175

Simple Arithmetic calculations in ALG mode.............................................. 175

Keying in Negative Numbers (

Chain Calculations in ALG mode................................................................ 176

Percentage Functions................................................................................. 176

Percent Difference................................................................................ 177

Percent of Total .................................................................................... 177

The Power Function ................................................................................... 178

Appendix C: More About L ......................................................... 179

Appendix D: Error Conditions ........................................................ 181

Error 0: Mathematics .................................................................................. 181

Error 1: Storage Register Overflow ............................................................ 181

Error 2: Statistics ........................................................................................ 182

Error 3: IRR ................................................................................................ 182

F KEY ................................................... 172

Þ)........................................................... 175

Page 8

Contents 9

Error 4: Memory.......................................................................................... 182

Error 5: Compound Interest........................................................................ 182

Error 6: Storage Registers.......................................................................... 183

Error 7: IRR ................................................................................................ 183

Error 8: Calendar........................................................................................ 184

Error 9: Service........................................................................................... 184

Pr Error ....................................................................................................... 184

Appendix E: Formulas Used ............................................................ 185

Percentage ................................................................................................. 185

Interest........................................................................................................ 185

Simple Interest...................................................................................... 185

Compound Interest ............................................................................... 185

Amortization................................................................................................ 186

Discounted Cash Flow Analysis ................................................................. 187

Net Present Value ................................................................................ 187

Internal Rate of Return ......................................................................... 187

Calendar..................................................................................................... 187

Actual Day Basis .................................................................................. 187

30/360 Day Basis ................................................................................. 188

Bonds ......................................................................................................... 188

Depreciation ............................................................................................... 189

Straight-Line Depreciation .................................................................... 189

Sum-of-the-Years-Digits Depreciation.................................................. 190

Declining-Balance Depreciation ........................................................... 190

Modified Internal Rate of Return................................................................. 190

Advance Payments..................................................................................... 191

Interest Rate Conversions .......................................................................... 191

Finite Compounding ............................................................................. 191

Continuous Compounding.................................................................... 191

Statistics ..................................................................................................... 191

Mean..................................................................................................... 191

Weighted Mean .................................................................................... 192

Linear Estimation.................................................................................. 192

Standard Deviation............................................................................... 192

Factorial................................................................................................ 192

The Rent or Buy Decision........................................................................... 193

Appendix F: Battery, Warranty, and Service Information ........ 195

Battery ........................................................................................................ 195

Low-Power Indication ................................................................................. 195

Installing a New Battery........................................................................ 195

Verifying Proper Operation (Self-Tests) ..................................................... 196

Warranty ..................................................................................................... 198

Service........................................................................................................ 200

Potential For Radio/Television Interference (for U.S.A. Only) .................... 201

Temperature Specifications........................................................................ 201

Noise Declaration ....................................................................................... 201

Regulation applying to The Netherlands .................................................... 202

Page 9

10 Contents

Appendix G: United Kingdom Calculations ................................ 203

Mortgages................................................................................................... 203

Annual Percentage Rate (APR) Calculations............................................. 203

Bond Calculations....................................................................................... 204

Function Key Index ..................................................................... 205

Programming Key Index ............................................................. 208

Subject Index ............................................................................... 211

Page 10

Making Financial

Calculations Easy

Before you begin to read through this handbook, let’s take a look at how easy

financial calculations can be with your HP 12C Platinum. While working

through the examples below, don’t be concerned about learning how to use the

calculator; we’ll cover that thoroughly beginning with Section 1.

Example 1: Suppose you want to ensure that you can finance your daughter’s

college education 14 years from today. You expect that the cost will be about

$6,000 a year ($500 a month) for 4 years. Assume she will withdraw $500 at the

beginning of each month from a savings account. How much would you have to

deposit into the account when she enters college if the account pays 6% annual

interest compounded monthly?

This is an example of a compound interest calculation. All such problems

involve at least three of the following quantities:

z n: the number of compounding periods.

z i: the interest rate per compounding period.

z P

W

: the present value of a compounded amount.

z PMT: the periodic payment amount.

z FV: the future value of a compounded amount.

In this particular example:

z n is 4 years × 12 periods per year = 48 periods.

z i is 6% per year ÷ 12 periods per year = 0.5% per period.

z PV is the quantity to be calculated – the present value when the financial

transaction begins.

z PMT is $500.

z FV is zero, since by the time your daughter graduates she (hopefully!) will

not need any more money.

To begin, turn the calculator on by pressing the ; key. Then, press the keys

shown in the Keystrokes column below.

Note: A battery symbol ( ) shown in the upper-left corner of the

display when the calculator is on signifies that the available battery power

is nearly exhausted. To install new batteries, refer to Appendix F.

1

1.

If you are not familiar with the use of an HP calculator keyboard, refer to the description

on pages 16 and 17.

11

Page 11

12 Making Financial Calculations Easy

The calendar functions and nearly all of the financial functions take some

time to produce an answer. (This is typically just a few seconds, but the

¼, !, L, and S functions could require a half-minute or more.)

During these calculations, the word running flashes in the display to let

you know that the calculator is running.

Keystrokes Display

fCLEARHf2

4gA

6gC

500P

g×

$

a Don’t be concerned now about the minus sign in the display. That and other details will

be explained in Section 3.

Example 2: We now need to determine how to accumulate the required deposit

by the time your daughter enters college 14 years from now. Let’s say that she

has a paid-up $5,000 insurance policy that pays 5.35% annually, compounded

semiannually. How much would it be worth by the time she enters college?

In this example, we need to calculate FV, the future value.

0.00

48.00

0.50

500.00

500.00

–21,396.61

Clears previous data inside the

calculator and sets display to show

two decimal places.

Calculates and stores the number of

compounding periods.

Calculates and stores the periodic

interest rate.

Stores periodic payment amount.

Sets payment mode to Begin.

Amount required to be deposited.

a

Keystrokes (RPN mode) Display

fCLEARG

14\2§w

5.35\2z¼

5000Þ$

M

Example 3: The preceding example showed that the insurance policy will

provide about half the required amount. An additional amount must be set aside

to provide the balance (21,396.61 – 10,470.85 = 10,925.76). Suppose you make

monthly payments, beginning at the end of next month, into an account that pays

–21,396.61

28.00

2.68

–5000.00

10,470.85

Clears previous financial data

inside the calculator.

Calculates and stores the number of

compounding periods.

Calculates and stores the periodic

interest rate.

Stores the present value of the

policy.

Value of policy in 14 years.

Page 12

Making Financial Calculations Easy 13

6% annually, compounded monthly. What payment amount would be required in

order to accumulate $10,925.75 in the 14 years remaining?

Keystrokes Display

fCLEARG

14gA

6gC

10925.76M

gÂ

P

Example 4: Suppose you cannot find a bank that currently offers an account

with 6% annual interest compounded monthly, but you can afford to make

$45.00 monthly payments. What is the minimum interest rate that will enable

you to accumulate the required amount?

In this problem, we do not need to clear the previous financial data inside the

calculator, since most of it is unchanged from the preceding example.

10,470.85

168.00

0.50

10.925.76

10.925.76

–41.65

Clears previous financial data

inside the calculator.

Calculates and stores the number of

compounding periods.

Calculates and stores the periodic

interest rate.

Stores the future value required.

Sets payment mode to End.

Monthly payment required.

Keystrokes Display

45ÞP

¼

12§

This is only a small sampling of the many financial calculations that can now be

done easily with your HP 12C Platinum. To begin learning about this powerful

financial tool, just turn the page.

–45.00

0.42

5.01

Stores payment amount.

Periodic interest rate.

Annual interest rate.

Page 13

Part I

Problem Solving

Page 14

Section 1

Getting Started

Power On and Off

To begin using your HP 12C Platinum, press the ; key1. Pressing ; again

turns the calculator off. If not manually turned off, the calculator will turn off

automatically 8 to 17 minutes after it was last used.

Low-Power Indication

A battery symbol ( ) shown in the upper-left corner of the display when the

calculator is on signifies that the available battery power is nearly exhausted. To

replace the batteries, refer to Appendix F.

The Keyboard

Many keys on the HP 12C Platinum perform two or even three functions. The

primary function of a key is indicated by the characters printed in white on the

upper face of the key. The alternate function(s) of a key are indicated by the

characters printed in gold above the key and the characters printed in blue on the

lower face of the key. These alternate functions are specified by pressing the

appropriate prefix key before the function key.

:

z To specify the alternate function printed in

gold above a key, press the gold prefix key

(f), then press the function key.

z To specify the primary function printed on

the upper face of a key, press the key alone.

z To specify the alternate function printed in

blue on the lower face of a key, press the

blue prefix key (g), then press the

function key.

Throughout this handbook, references to the operation of an alternate function

appear as only the function name in a box (for example, “The L function …”).

References to the selection of an alternate function appear preceded by the

1.

Note that the ; key is lower than the other keys to help prevent its being pressed

inadvertently.

16

Page 15

Section 1: Getting Started 17

appropriate prefix key (for example, “Pressing fL …”). References to the

functions shown on the keyboard in gold under the bracket labeled “CLEAR”

appear throughout this handbook preceded by the word “CLEAR” (for example,

“The CLEAR H function …” or “Pressing fCLEARH …”).

If you press the f or g prefix key mistakenly, you can cancel it by pressing

fCLEAR X. This can also be pressed to cancel the ?, :, and i

keys. (These keys are “prefix” keys in the sense that other keys must be pressed

after them in order to execute the corresponding function.) Since the X key is

also used to display the mantissa (all 10 digits) of a displayed number, the

mantissa of the number in the display will appear for a moment after the X

key is released.

Pressing the f or g prefix key turns on the corresponding status indicator – f

or g – in the display. Each indicator turns off when you press a function key

(executing an alternate function of that key), another prefix key, or

fCLEAR X.

Keying in Numbers

To key a number into the calculator, press the digit keys in sequence, just as if

you were writing the number on paper. A decimal point must be keyed in (using

the decimal point key) if it is part of the number unless it appears to the right of

the last digit.

Digit Separators

As a number is keyed in, each group of three digits to the left of the decimal

point is automatically separated in the display. When the calculator is first turned

on after coming from the factory – or after Continuous Memory is reset – the

decimal point in displayed numbers is a dot, and the separator between each

group of three digits is a comma. If you wish, you can set the calculator to

display a comma for the decimal point and a dot for the three-digit separator. To

do so, turn the calculator off, then press and hold down the . key while you

press ;. Doing so again sets the calculator to use the original digit separators

in the display.

Negative Numbers

To make a displayed number negative – either one that has just been keyed in or

one that has resulted from a calculation – simply press Þ (change sign). When

the display shows a negative number – that is, the number is preceded by a minus

sign – pressing Þ removes the minus sign from the display, making the

number positive.

Page 16

18 Section 1: Getting Started

Keying in Large Numbers

Since the display cannot show more than 10 digits of a number, numbers greater

than 9,999,999,999 cannot be entered into the display by keying in all the digits

in the number. However, such numbers can be easily entered into the display if

the number is expressed in a mathematical shorthand called “scientific notation.”

To convert a number into scientific notation, move the decimal point until there

is only one digit (a nonzero digit) to its left. The resulting number is called the

“mantissa” of the original number, and the number of decimal places you moved

the decimal point is called the “exponent” of the original number. If you moved

the decimal point to the left, the exponent is positive; if you moved the decimal

point to the right (this would occur for numbers less than one), the exponent is

negative. To key the number into the display, simply key in the mantissa, press

Æ (enter exponent), then key in the exponent. If the exponent is negative,

press Þ after pressing Æ.

For example, to key in $1,781,400,000,000, we move the decimal point 12

places to the left, giving a mantissa of 1.7814 and an exponent of 12:

Keystrokes Display

1.7814Æ12

Numbers entered in scientific notation can be used in calculations just like any

other number.

1.7814 12

1,781,400,000,000 entered in

scientific notation.

The CLEAR Keys

Clearing a register or the display replaces the number in it with zero. Clearing

program memory replaces the instructions there with gi000. There are

several clearing operations on the HP 12C Platinum, as shown in the table

below:

Key(s) Clears:

O Display and X-register.

fCLEAR² Statistics registers (R

registers, and display.

fCLEARÎ Program memory (only when pressed in

Program mode).

fCLEARG Financial registers.

fCLEARH Data storage registers, financial registers,

stack and LAST X registers, and display.

through R6), stack

1

Page 17

Section 1: Getting Started 19

The RPN and ALG Keys

The calculator can be set to perform arithmetic operations in either RPN

(Reverse Polish Notation) or ALG (Algebraic) mode.

In reverse polish notation (RPN) mode, the intermediate results of calculations

are stored automatically, hence you do not have to use parentheses.

In algebraic (ALG) mode, you perform addition, subtraction, multiplication, and

division in the traditional way.

To select RPN mode: Press f] to set the calculator to RPN mode. When the

calculator is in RPN mode, the RPN status indicator is lit.

To select ALG mode: Press f[ to set the calculator to ALG mode. When

the calculator is in ALG mode, the ALG status indicator is lit.

Example

Suppose you want to calculate 1 + 2 = 3.

In RPN mode, you enter the first number, press the \ key, enter the second

number, and finally press the arithmetic operator key: +.

In ALG mode, you enter the first number, press +, enter the second number,

and finally press the equals key: }.

RPN mode ALG mode

1 \ 2 + 1 + 2 }

In RPN mode and algebraic mode, the results of all calculations are listed.

However, in RPN mode only the results are listed, not the calculations.

Most examples in this manual (except those in Appendix B) assume that RPN

mode is selected. Some examples will also be correct if you are in ALG mode.

Simple Arithmetic Calculations in RPN Mode

In RPN mode, any simple arithmetic calculation involves two numbers and an

operation – addition, subtraction, multiplication, or division. To do such a

calculation on your HP 12C Platinum, you first tell the calculator the two

numbers, then tell the calculator the operation to be performed. The answer is

calculated when the operation key (+,-,§, or z) is pressed.

The two numbers should be keyed into the calculator in the order they would

appear if the calculation were written down on paper left-to-right. After keying

in the first number, press the \ key to tell the calculator that you have

completed entering the number. Pressing \ separates the second number to

be entered from the first number already entered.

Page 18

20 Section 1: Getting Started

In summary, to perform an arithmetic operation:

1. Key in the first number.

2. Press \ to separate the second number from the first.

3. Key in the second number.

4. Press +,-,§, or z to perform the desired operation.

For example to calculate 13 ÷ 2, proceed as follows:

Keystrokes (RPN mode) Display

13

\

2

z

Notice that after you pressed \, two zeroes appeared following the decimal

point. This is nothing magical: the calculator’s display is currently set to show

two decimal places of every number that has been entered or calculated. Before

you pressed \, the calculator had no way of knowing that you had completed

entering the number, and so displayed only the digits you had keyed in. Pressing

\ tells the calculator that you have completed entering the number: it

terminates digit entry. You need not press \ after keying in the second

number because the +,-,§, and z keys also terminate digit entry. (In fact,

all keys terminate digit entry except for digit entry keys – digit keys, ., Þ,

and Æ – and prefix keys – f, g, ?, :, and (.)

13.

13.00

2.

6.50

Keys the first number into the

calculator.

Pressing \ separates the second

number from the first.

Keys the second number into the

calculator.

Pressing the operation key

calculates the answer.

Chain Calculations in RPN Mode

Whenever the answer has just been calculated and is therefore in the display, you

can perform another operator with this number by simply keying in the second

number and then pressing the operation key: you need not press \ to separate

the second number from the first. This is because when a number is keyed in

after a function key (such as +,-,§,z, etc.) is pressed, the result of that

prior calculation is stored inside the calculator – just as when the \ key is

pressed. The only time you must press the \ key to separate two numbers is

when you are keying them both in, one immediately following the other.

The HP 12C Platinum is designed so that each time you press a function key in

RPN mode, the calculator performs the operation then – not later – so that you

see the results of all intermediate calculations, as well as the “bottom line.”

Page 19

Section 1: Getting Started 21

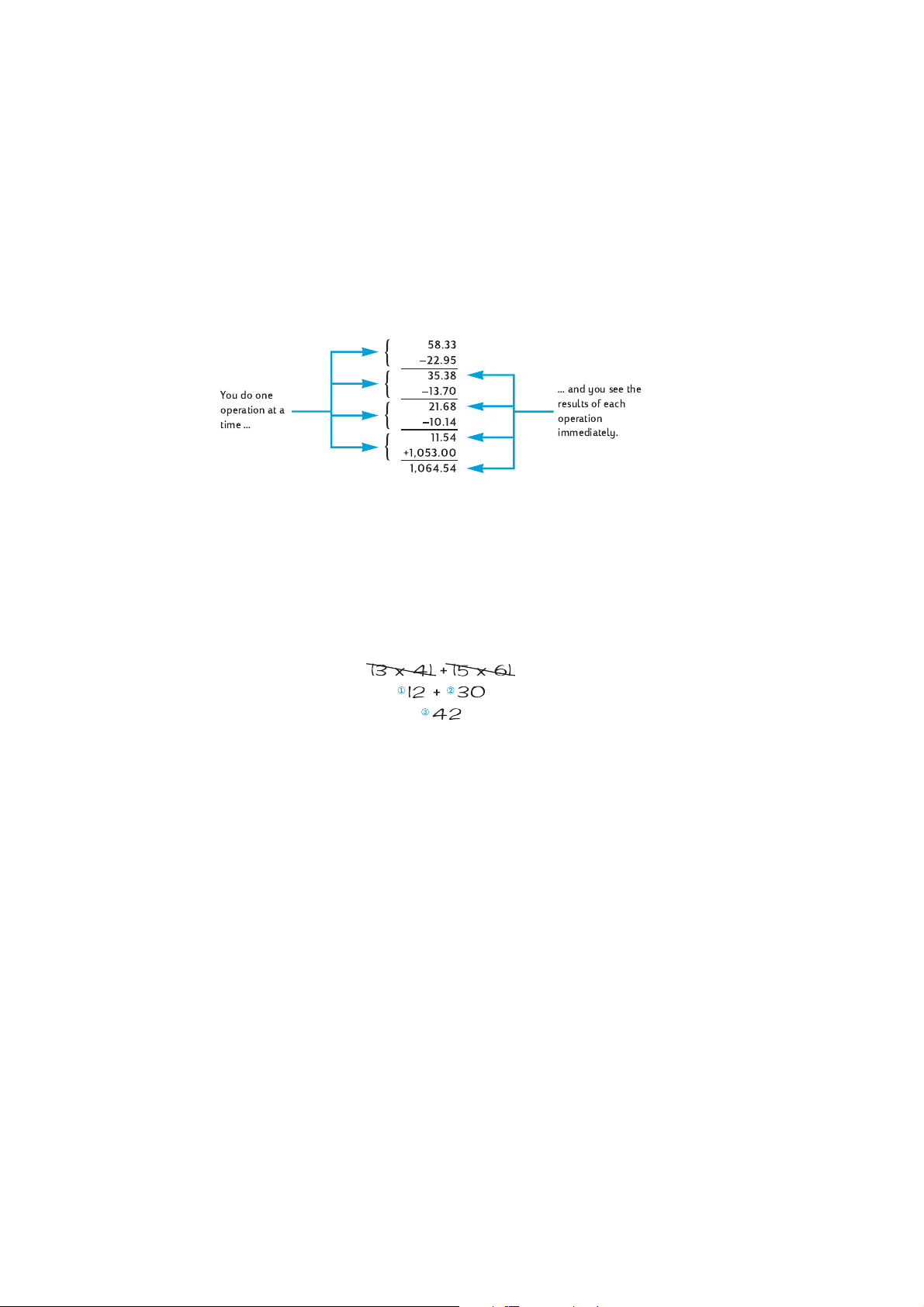

Example: Suppose you’ve written three checks without updating your

checkbook, and you’ve just deposited your paycheck for $1,053.00 into your

checking account. If your latest balance was $58.33 and the checks were written

for $22.95, $13.70, and $10.14, what is the new balance?

Solution: When written down on paper, this problem would read

58.33 – 22.95 – 13.70 – 10.14 + 1053

Keystrokes (RPN mode) Display

58.33

\

22.95

-

13.70

-

10.14-

1053+

58.33

58.33

22.95

35.38

13.70

21.68

11.54

1,064.54

Keys the first number.

Pressing \ separates the second

number from the first.

Keys in the second number.

Pressing - subtracts the second

number from the first. The

calculator displays the result of this

calculation, which is the balance

after subtracting the first check.

Keys in the next number. Since a

calculation has just been

performed, do not press \; the

next number entered (13.70) is

automatically separated from the

one previously in the display

(35.38).

Pressing - subtracts the number

just entered from the number

previously in the display. The

calculator displays the result of this

calculation, which is the balance

after subtracting the second check.

Keys in the next number and

subtracts it from the previous

balance. The new balance appears

in the display. (It’s getting rather

low!)

Keys in the next number – the

paycheck deposited – and adds it to

the previous balance. The new,

current balance appears in the

display.

Page 20

22 Section 1: Getting Started

The preceding example demonstrates how the HP 12C Platinum calculates just

as you would using pencil and paper (except a lot faster!):

Youdoone

operation at a

time ...

... and you see the

results of each

operation

immediately.

Let’s see this happening in a different type of calculation – one that involves

multiplying groups of two numbers and then adding the results. (This is the type

of calculation that would be required to total up an invoice consisting of several

items with different quantities and different prices.)

For example, consider the calculation of (3 × 4) + (5 × 6). If you were doing this

on paper, you would first do the multiplication in the first parentheses, then the

multiplication in the second parentheses, and finally add the results of the two

multiplications:

Your HP 12C Platinum calculates the answer in just the same way:

Keystrokes (RPN mode) Display

3\4§

5\6§

+

12.00

30.00

42.00

Step 1: Multiply the numbers in the

first parentheses.

Step 2: Multiply the numbers in the

second parentheses.

Step 3: Add the results of the two

multiplications.

Notice that before doing step 2, you did not need to store or write down the result

of step 1: it was stored inside the calculator automatically. And after you keyed

in the 5 and the 6 in step 2, the calculator was holding two numbers (12 and 5)

inside for you, in addition to the 6 in the display. (The HP 12C Platinum can hold

a total of three numbers inside, in addition to the number in the display.) After

step 2, the calculator was still holding the 12 inside for you, in addition to the 30

in the display. You can see that the calculator holds the number for you, just as

you would have them written on paper, and then calculates with them at the

Page 21

Section 1: Getting Started 23

proper time, just as you would yourself.2 But with the HP 12C Platinum, you

don’t need to write down the results of an intermediate calculation, and you don’t

even need to manually store it and recall it later.

By the way, notice that in step 2 you needed to press \ again. This is simply

because you were again keying in two numbers immediately following each

other, without performing a calculation in between.

To check your understanding of how to calculate with your HP 12C Platinum, try

the following problems yourself. Although these problems are relatively simple,

more complicated problems can be solved using the same basic steps. If you

have difficulty obtaining the answers shown, review the last few pages.

34+()56+()× 77.00=

27 14–()

-----------------------0.25=

14 38+()

5

--------------------------- 0 . 1 3=

31621++

Storage Registers

Numbers (data) in the HP 12C Platinum are stored in memories called “storage

registers” or simply “registers.” (The singular term “memory” is sometimes used

in this handbook to refer to the entire collection of storage registers.) Four

special registers are used for storing numbers during calculations (these “stack

registers” are described in Appendix A), and another (called the “LAST X”

register) is used for storing the number last in the display before an operation is

performed. In addition to these registers into which numbers are stored

automatically, up to 20 “data storage” registers are available for manual storage

of numbers. These data storage registers are designated R

through R.9. Fewer registers are available for data storage if a program has been

stored in the calculator (since the program is stored in some of those 20

registers), but a minimum of 7 registers is always available. Still other storage

registers – referred to as the “financial registers” – are reserved for numbers used

in financial calculations.

through R9 and R

0

.0

2.

Although you don’t need to know just how these numbers are stored and brought back at just

the right time, if you’re interested you can read all about it in Appendix A. By gaining a more

complete understanding of the calculator’s operation, you’ll use it more efficiently and

confidently, yielding a better return on the investment in your HP 12C Platinum.

Page 22

24 Section 1: Getting Started

Storing and Recalling Numbers

To store the number from the display into a data storage register:

1. Press ? (store).

2. Key in the register number: 0 through 9 for registers R

through .9 for registers R

through R.9.

.0

Similarly, to recall a number from a storage register into the display, press :

(recall), then key in the register number. This copies the number from the storage

register into the display; the number remains unaltered in the storage register.

Furthermore, when this is done, the number previously in the display is

automatically held inside the calculator for a subsequent calculation, just as the

number in the display is held when you key in another number.

Example: Before you leave to call on a customer interested in your personal

computer, you store the cost of the computer ($3,250) and also the cost of a

printer ($2,500) in data storage registers. Later, the customer decides to buy six

computers and one printer. You recall the cost of the computer, multiply by the

quantity ordered, and then recall and add the cost of the printer to get the total

invoice.

Keystrokes (RPN mode) Display

3250?1

2500?2

3,250.00

2,500.00

; Turns the calculator off.

Stores the cost of the computer in

R

.

1

Stores the cost of the printer in R2.

through R9, or .0

0

Later that same day …

Keystrokes (RPN mode) Display

;

:1

6§

:2

+

2,500.00

3,250.00

19,500.00

2,500.00

22,000.00

Turns the calculator back on.

Recalls the cost of the computer to

the display.

Multiplies the quantity ordered to

get the cost of the computers.

Recalls the cost of the printer to the

display.

Total invoice.

Page 23

Section 1: Getting Started 25

Clearing Storage Registers

To clear a single storage register – that is, to replace the number in it with zero –

merely store zero into it. You need not clear a storage register before storing data

into it; the storing operation automatically clears the register before the data is

stored.

To clear all storage registers at once – including the financial registers, the stack

registers, and the LAST X register – press fCLEARH.

3

This also clears the

display.

All storage registers are also cleared when Continuous Memory is reset (as

described on page 70).

Storage Register Arithmetic

Suppose you wanted to perform an arithmetic operation with the number in the

display and the number in a storage register, then store the result back into the

same register without altering the number in the display. The HP 12C Platinum

enables you to do all this in a single operation.

1. Press ?.

2. Press +,-,§, or z to specify the desired operation.

3. Key in the register number.

When storage register arithmetic is performed, the new number in the register is

determined according to the following rule:

number formerly

in register

Storage register arithmetic is possible with only registers R

number in display

through R

0

4

.

Example: In the example on page 21, we updated the balance in your

checkbook. Let’s suppose that because data is stored indefinitely in your

calculator’s Continuous Memory, you keep track of your checking account

balance in the calculator. You could use storage register arithmetic to quickly

update the balance after depositing or writing checks.

3.

CLEARH is not programmable.

Page 24

26 Section 1: Getting Started

Keystrokes Display

58.33?0

22.95?-0

13.70?-0

10.14?-0

1053?+0

:0

58.33

22.95

13.70

10.14

1,053.00

1,064.54

Stores the current balance in

register R

.

0

Subtracts the first check from the

balance in R

. Note that the display

0

continues to show the amount

subtracted; the answer is placed

only in R

.

0

Subtracts the second check.

Subtracts the third check.

Adds the deposit.

Recalls the number in R0 to check

the new balance.

Page 25

Section 2

Percentage and Calendar

Functions

Percentage Functions

The HP 12C Platinum includes three keys for solving percentage problems: b,

à, and Z. You don’t need to convert percentages to their decimal

equivalents; this is done automatically when you press any of these keys. Thus,

4% need not be changed to 0.04; you key it in the way you see and say it: 4b.

Percentages

In RPN mode, to find the amount corresponding to a percentage of a number:

1. Key in the base number.

2. Press \.

3. Key in the percentage.

4. Press b.

For example, to find 14% of $300:

Keystrokes (RPN mode) Display

300

\

14

b

300.

300.00

14.

42.00

Keys in the base number.

Pressing \ separates the next

number entered from the first

number, just as when an ordinary

arithmetic calculation is performed.

Keys in the percentage.

Calculates the amount.

If the base number is already in the display as a result of a previous calculation,

you should not press \ before keying in the percentage – just as in a chain

arithmetic calculation.

Net Amount

A net amount – that is, the base amount plus or minus the percentage amount –

can be calculated easily with your HP 12C Platinum, since the calculator holds

27

Page 26

28 Section 2: Percentage and Calendar Functions

the base amount inside after you calculate a percentage amount. To calculate a

net amount, simply calculate the percentage amount, then press = or -.

Example: You’re buying a new car that lists for $13,250. The dealer offers you a

discount of 8%, and the sales tax is 6%. Find the amount the dealer is charging

you, then find the total cost to you, including tax.

Keystrokes (RPN mode) Display

13250\

8b

6b

=

13,250.00

1,060.00

12,190.00

731.40

12,921.40

Keys in the base amount and

separates it from the percentage.

Amount of discount.

Base amount less discount.

Amount of tax (on $12,190).

Total cost: base amount less

discount plus tax.

Percent Difference

In RPN mode, to find the percent difference between two numbers:

1. Key in the base number.

2. Press \ to separate the other number from the base number.

3. Key in the other number.

4. Press à.

If the other number is greater than the base number, the percent difference will

be positive. If the other number is less than the base number, the percent

difference will be negative. Therefore, a positive answer indicates an increase,

while a negative answer indicates a decrease.

If you are calculating a percent difference over time, the base number is typically

the amount occurring first.

Example: Yesterday your stock fell from 58˝ to 53ď per share. What is the

percent change?

Keystrokes Display

58.5\

53.25

à

The à key can be used for calculations of the percent difference between a

wholesale cost and a retail cost. If the base number entered is the wholesale cost,

58.50

53.25

–8.97

Keys in the base number and

separates it from the other number.

Keys in the other number.

Nearly a 9% decrease.

Page 27

Section 2: Percentage and Calendar Functions 29

the percent difference is called the markup; if the base number entered is the

retail cost, the percent difference is called the margin. Examples of markup and

margin calculations are included in the HP 12C Platinum Solutions Handbook.

Percent of Total

In RPN mode, to calculate what percentage one number is of another:

1. Calculate the total amount by adding the individual amounts, just as in a

chain arithmetic calculation.

2. Key in the number whose percentage equivalent you wish to find.

3. Press Z.

Example: Last month, your company posted sales of $3.92 million in the U.S.,

$2.36 million in Europe, and $1.67 million in the rest of the world. What

percentage of the total sales occurred in Europe?

Keystrokes (RPN mode) Display

3.92\

2.36+

1.67+

2.36

Z

3.92

6.28

7.95

2.36

29.69

Keys in the first number and

separates it from the second.

Adds the second number.

Adds the third number to get the

total.

Keys in 2.36 to find what

percentage it is of the number in the

display.

Europe had nearly 30% of the total

sales.

The HP 12C Platinum holds the total amount inside after a percent of total is

calculated. Therefore, to calculate what percentage another amount is of the

total:

1. Clear the display by pressing O.

2. Key in that amount.

3. Press Z again.

For example, to calculate what percent of the total sales in the preceding

example occurred in the U.S. and what percent occurred in the rest of the world:

Keystrokes (RPN mode) Display

O3.92Z

O1.67 Z

49.31

21.01

The U.S. had about 49% of the total

sales.

The rest of the world had about

21% of the total sales.

Page 28

30 Section 2: Percentage and Calendar Functions

To find what percentage a number is of a total, when you already know the total

number

1. Key in the total number.

2. Press \ to separate the other number from the total number.

3. Key in the number whose percentage equivalent you wish to find.

4. Press Z.

For example, if you already knew in the preceding example that the total sales

were $7.95 million and you wanted to find what percentage of that total occurred

in Europe:

Keystrokes Display

7.95\

2.36

Z

7.95

2.36

29.69

Keys in the total amount and

separates it from the next number.

Keys in 2.36 to find what

percentage it is of the number in the

display.

Europe had nearly 30% of the total

sales.

Calendar Functions

The calendar functions provided by the HP 12C Platinum – D and Ò – can

handle dates from October 15, 1582 through November 25, 4046.

Date Format

For each of the calendar functions – and also for bond calculations (E and

S) – the calculator uses one of two date formats. The date format is used to

interpret dates when they are keyed into the calculator as well as for displaying

dates.

Month-Day-Year. To set the date format to month-day-year, press gÕ. To

key in a date with this format in effect:

1. Key in the one or two digits of the month.

2. Press the decimal point key (.).

3. Key in the two digits of the day.

4. Key in the four digits of the year.

Dates are displayed in the same format.

Page 29

Section 2: Percentage and Calendar Functions 31

For example, to key in April 7, 2004:

Keystrokes Display

4.072004

Day-Month-Year. To set the date format to day-month-year, press gÔ. To

key in a date with this format in effect:

1. Key in the one or two digits of the day.

2. Press the decimal point key (.).

3. Key in the two digits of the month.

4. Key in the four digits of the year.

For example, to key in 7 April, 2004:

4.072004

Keystrokes Display

7.042004

When the date format is set to day-month-year, the D.MY status indicator in the

display is lit. If D.MY is not lit, the date format is set to month-day-year.

The date format remains set to what you last specified until you change it; it is

not reset each time the calculator is turned on. However, if Continuous Memory

is reset, the date format is set to month-day-year.

7.042004

Future or Past Dates

To determine the date and day that is a given number of days from a given date:

1. Key in the given date and press \.

2. Key in the number of days.

3. If the other date is in the past, press Þ.

4. Press gD.

The answer calculated by the D function is displayed in a special format. The

numbers of the month, day, and year (or day, month, and year) are separated by

digit separators, and the digit at the right of the displayed answer indicates the

day of the week: 1 for Monday through 7 for Sunday.

4.

The day of the week indicated by the D function may differ from that recorded in history

for dates when the Julian calendar was in use. The Julian calendar was standard in England

and its colonies until September 14, 1752, when they switched to the Gregorian calendar.

Other countries adopted the Gregorian calendar at various times.

4

Page 30

32 Section 2: Percentage and Calendar Functions

Example: If you purchased a 120-day option on a piece of land on 14 May 2004,

what would be the expiration date? Assume that you normally express dates in

the day-month-year format.

Keystrokes Display

gÔ

14.052004\

120gD

When D is executed as an instruction in a running program, the calculator

pauses for about 1 second to display the result, then resumes program execution.

7.04

14.05

11,09,2004 6

Sets date format to day-monthyear. (Display shown assumes

date remains from preceding

example. The full date is not

now displayed because the

display format is set to show

only two decimal places, as

described in Section 5.)

Keys in date and separates it

from number of days to be

entered.

The expiration date is 11

September 2004, a Saturday.

Number of Days Between Dates

To calculate the number of days between two given dates:

1. Key in the earlier date and press \.

2. Key in the later date and press gÒ.

The answer shown in the display is the actual number of days between the two

dates, including leap days (the extra days occurring in leap years), if any. In

addition, the HP 12C Platinum also calculates the number of days between the

two dates on the basis of a 30-day month. This answer is held inside the

calculator; to display it, press ~. Pressing ~ again will return the original

answer to the display.

Example: Simple interest calculations can be done using either the actual

number of days or the number of days counted on the basis of a 30-day month.

What would be the number of days counted each way, to be used in calculating

the simple interest accruing from June 3, 2004 to October 14, 2005? Assume that

you normally express dates in the month-day-year format.

Page 31

Section 2: Percentage and Calendar Functions 33

Keystrokes Display

gÕ

6.032004\

10.152005gÒ

~

11.09

6.03

498.00

491.00

Sets date format to month-day-year.

(Display shown assumes date

remains from preceding example.)

Keys in earlier date and separates it

from the later date.

Keys in later date. Display shows

actual number of days.

Number of days counted on the

basis of a 30-day month.

Page 32

Section 3

Basic Financial Functions

The Financial Registers

In addition to the data storage registers discussed on page 23, the HP 12C

Platinum has five special registers in which numbers are stored for financial

calculations. These registers are designated n, i, PV, PMT, and FV. The first five

keys on the top row of the calculator are used to store a number from the display

into the corresponding register, to calculate the corresponding financial value

and store the result into the corresponding register, or to display the number

stored in the corresponding register.

Storing Numbers Into the Financial Registers

To store a number into a financial register, key the number into the display, then

press the corresponding key (n, ¼, $, P, or M).

Displaying Numbers in the Financial Registers

5

To display a number stored in a financial register, press : followed by the

corresponding key.

6

Clearing the Financial Registers

Every financial function uses numbers stored in several of the financial registers.

Before beginning a new financial calculation, it is good practice to clear all of

the financial registers by pressing fCLEARG. Frequently, however, you

may want to repeat a calculation after changing a number in only one of the

financial registers. To do so, do not press fCLEARG; instead, simply store

the new number in the register. The numbers in the other financial registers

remain unchanged.

5.

Which operation is performed when one of these keys is pressed depends upon the last

preceding operation performed: If a number was just stored into a financial register (using

n, ¼, $, P, M, A, or C), pressing one of these five keys calculates the

corresponding value and stores it into the corresponding register; otherwise pressing one of

these five keys merely stores the number from the display into the corresponding register.

6.

It’s good practice to press the corresponding key twice after :, since often you may want

to calculate a financial value right after displaying another financial value. As indicated in the

preceding footnote, if you wanted to display FV and then calculate PV, for example, you

should press :MM$. If you didn’t press M the second time, pressing

store FV in the PV register rather than calculating PV, and to calculate PV you would have to

press $ again.

34

$ would

Page 33

Section 3: Basic Financial Functions 35

The financial registers are also cleared when you press fCLEARH and

when Continuous Memory is reset (as described on page 70).

Simple Interest Calculations

The HP 12C Platinum simultaneously calculates simple interest on both a 360day basis and a 365-day basis. You can display either one, as described below.

Furthermore, with the accrued interest in the display, you can calculate the total

amount (principal plus accrued interest) by pressing +.

1. Key in or calculate the number of days, then press n.

2. Key in the annual interest rate, then press ¼.

3. Key in the principal amount, then press Þ$.

4. Press fÏ to calculate and display the interest accrued on a 360-day

basis.

5. If you want to display the interest accrued on a 365-day basis, press

d~.

6. Press + to calculate the total of the principal and the accrued interest now

in the display.

The quantities n, i, and PV can be entered in any order.

Example 1: Your good friend needs a loan to start his latest enterprise and has

requested that you lend him $450 for 60 days. You lend him the money at 7%

simple interest, to be calculated on a 360-day basis. What is the amount of

accrued interest he will owe you in 60 days, and what is the total amount owed?

7

Keystrokes (RPN mode) Display

60n

7¼

450Þ$

fÏ

+

60.00

7.00

–450.00

5.25

455.25

Example 2: Your friend agrees to the 7% interest on the loan from the preceding

example, but asks that you compute it on a 365-day basis rather than a 360-day

7.

Pressing the $ key stores the principal amount in the PV register, which then contains the

present value of the amount on which interest will accrue. The Þ key is pressed first to

change the sign of the principal amount before storing it in the PV register. This is required

by the cash flow sign convention, which is applicable primarily to compound interest

calculations.

Stores the number of days.

Stores the annual interest rate.

Stores the principal.

Accrued interest, 360-day basis.

Total amount: principal plus

accrued interest.

Page 34

36 Section 3: Basic Financial Functions

basis. What is the amount of accrued interest he will owe you in 60 days, and

what is the total amount owed?

Keystrokes (RPN mode) Display

60n

7¼

450Þ$

fÏd~

+

60.00

7.00

–450.00

5.18

455.18

If you have not altered the

numbers in the n, i, and PV

registers since the preceding

example, you may skip these

keystrokes.

Accrued interest, 365-day

basis.

Total amount: principal plus

accrued interest.

Financial Calculations and the Cash Flow Diagram

The concepts and examples presented in this section are representative of a wide

range of financial calculations. If your specific problem does not appear to be

illustrated in the pages that follow, don’t assume that the calculator is not capable

of solving it. Every financial calculation involves certain basic elements; but the

terminology used to refer to these elements typically differs among the various

segments of the business and financial communities. All you need to do is

identify the basic elements in your problem, and then structure the problem so

that it will be readily apparent what quantities you need to tell the calculator and

what quantity you want to solve for.

An invaluable aid for using your calculator in a financial calculation is the cash

flow diagram. This is simply a pictorial representation of the timing and

direction of financial transactions, labeled in terms that correspond to keys on

the calculator.

The diagram begins with a horizontal line, called a time line. It represents the

duration of a financial problem, and is divided into compounding periods. For

example, a financial problem that transpires over 6 months with monthly

compounding would be diagrammed like this:

The exchange of money in a problem is depicted by vertical arrows. Money you

receive is represented by an arrow pointing up from the point in time line when

the transaction occurs; money you pay out is represented by an arrow pointing

down.

Page 35

Section 3: Basic Financial Functions 37

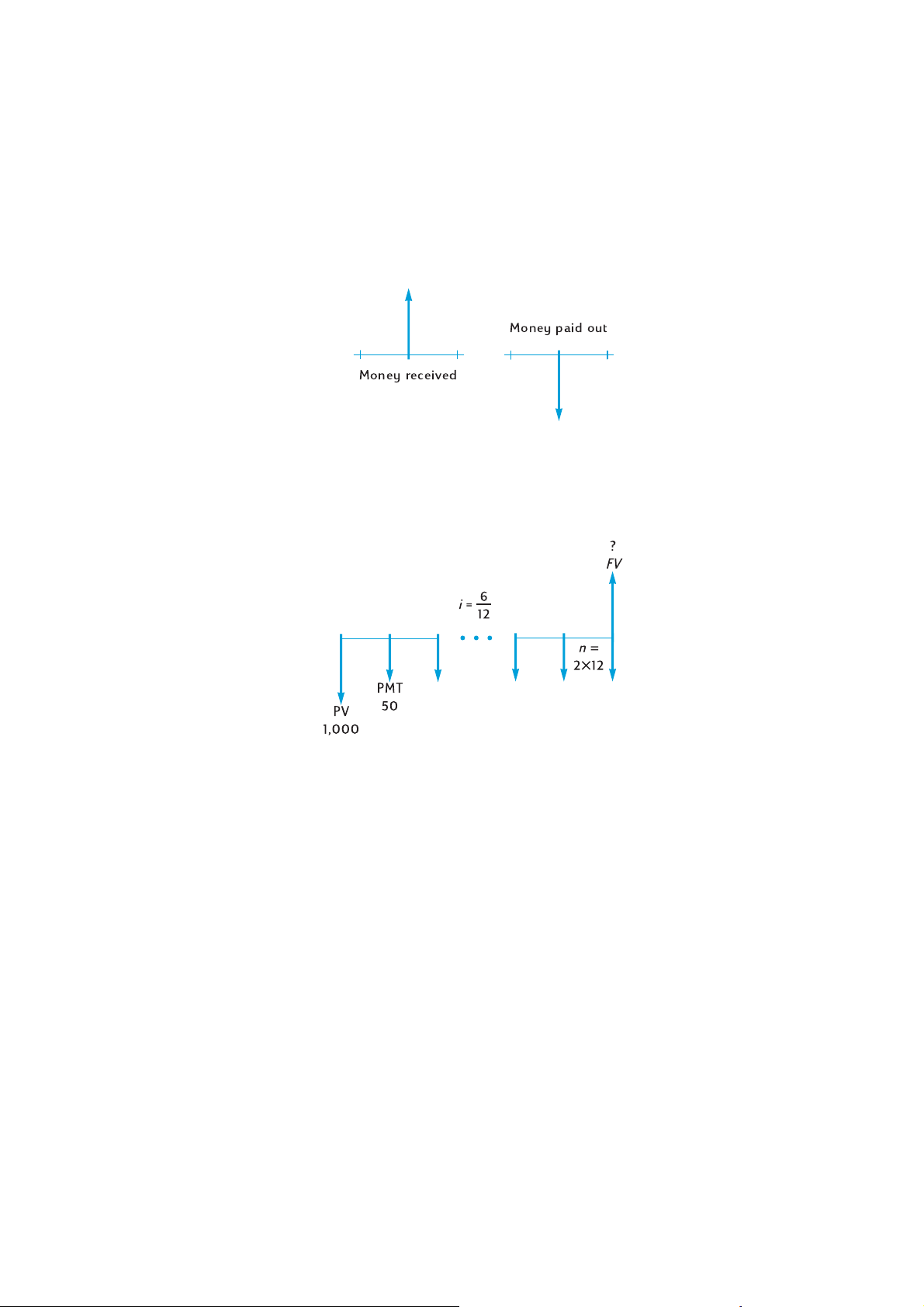

Money paid out

Money received

Suppose you deposited (paid out) $1,000 into an account that pays 6% annual

interest and is compounded monthly, and you subsequently deposited an

additional $50 at the end of each month for the next 2 years. The cash flow

diagram describing the problem would look like this:

The arrow pointing up at the right of the diagram indicates that money is

received at the end of the transaction. Every completed cash flow diagram must

include at least one cash flow in each direction. Note that cash flows

corresponding to the accrual of interest are not represented by arrows in the cash

flow diagram.

The quantities in the problem that correspond to the first five keys on the top row

of the keyboard are now readily apparent from the cash flow diagram.

z n is the number of compounding periods. This quantity can be expressed in

years, months, days, or any other time unit, as long as the interest rate is

expressed in terms of the same basic compounding period. In the problem

illustrated in the cash flow diagram above, n = 2 × 12.

The form in which n is entered determines whether or not the calculator

performs financial calculations in Odd-Period mode (as described on pages

51 through 54). If n is a noninteger (that is, there is at least one nonzero

digit to the right of the decimal point), calculations of i, PV, PMT, and FV

are performed in Odd-Period mode.

Page 36

38 Section 3: Basic Financial Functions

z i is the interest rate per compounding period. The interest rate shown in the

cash flow diagram and entered into the calculator is determined by

dividing the annual interest rate by the number of compounding periods. In

the problem illustrated above, i = 6% ÷ 12.

z PV – the present value – is the initial cash flow or the present value of a

series of future cash flows. In the problem illustrated above, PV is the

$1,000 initial deposit.

z PMT is the period payment. In the problem illustrated above PMT is the

$50 deposited each month. When all payments are equal, they are referred

to as annuities. (Problems involving equal payments are described in this

section under Compound Interest Calculations; problems involving

unequal payments can be handled as described in Section 4 under

Discounted Cash Flow Analysis: NPV and IRR. Procedures for calculating

the balance in a savings account after a series of irregular and/or unequal

deposits are included in the HP 12C Platinum Solutions Handbook.)

z FV – the future value – is the final cash flow or the compounded value of a

series of prior cash flows. In the particular problem illustrated above, FV is

unknown (but can be calculated).

Solving the problem is now basically a matter of keying in the quantities

identified in the cash flow diagram using the corresponding keys, and then

calculating the unknown quantity by pressing the corresponding key. In the

particular problem illustrated in the cash flow diagram above, FV is the unknown

quantity; but in other problems, as we shall see later, n, i, PV, or PMT could be

the unknown quantity. Likewise, in the particular problem illustrated above there

are four known quantities that must be entered into the calculator before solving

for the unknown quantity; but in other problems only three quantities may be

known – which must always include n or i.

The Cash Flow Sign Convention

When entering the PV, PMT, and FV cash flows, the quantities must be keyed

into the calculator with the proper sign, + (plus) or – (minus), in accordance with

…

The Cash Flow Sign Convention: Money received (arrow pointing up) is

entered or displayed as a positive value (+). Money paid out (arrow

pointing down) is entered or displayed as a negative value (–).

The Payment Mode

One more bit of information must be specified before you can solve a problem

involving periodic payments. Such payments can be made either at the beginning

of a compounding period (payments in advance, or annuities due) or at the end of

the period (payments in arrears, or ordinary annuities). Calculations involving

Page 37

Section 3: Basic Financial Functions 39

payments in advance yield different results than calculations involving payments

in arrears. Illustrated below are portions of cash flow diagrams showing

payments in advance (Begin) and payments in arrears (End). In the problem

illustrated in the cash flow diagram above, payments are made in arrears.

Begin

Regardless of whether payments are made in advance or in arrears, the number

of payments must be the same as the number of compounding periods.

To specify the payment mode:

z Press g× if payments are made at the beginning of the compounding

periods.