EDD EMPLOYEE’S WITHHOLDING ALLOWANCE User Manual

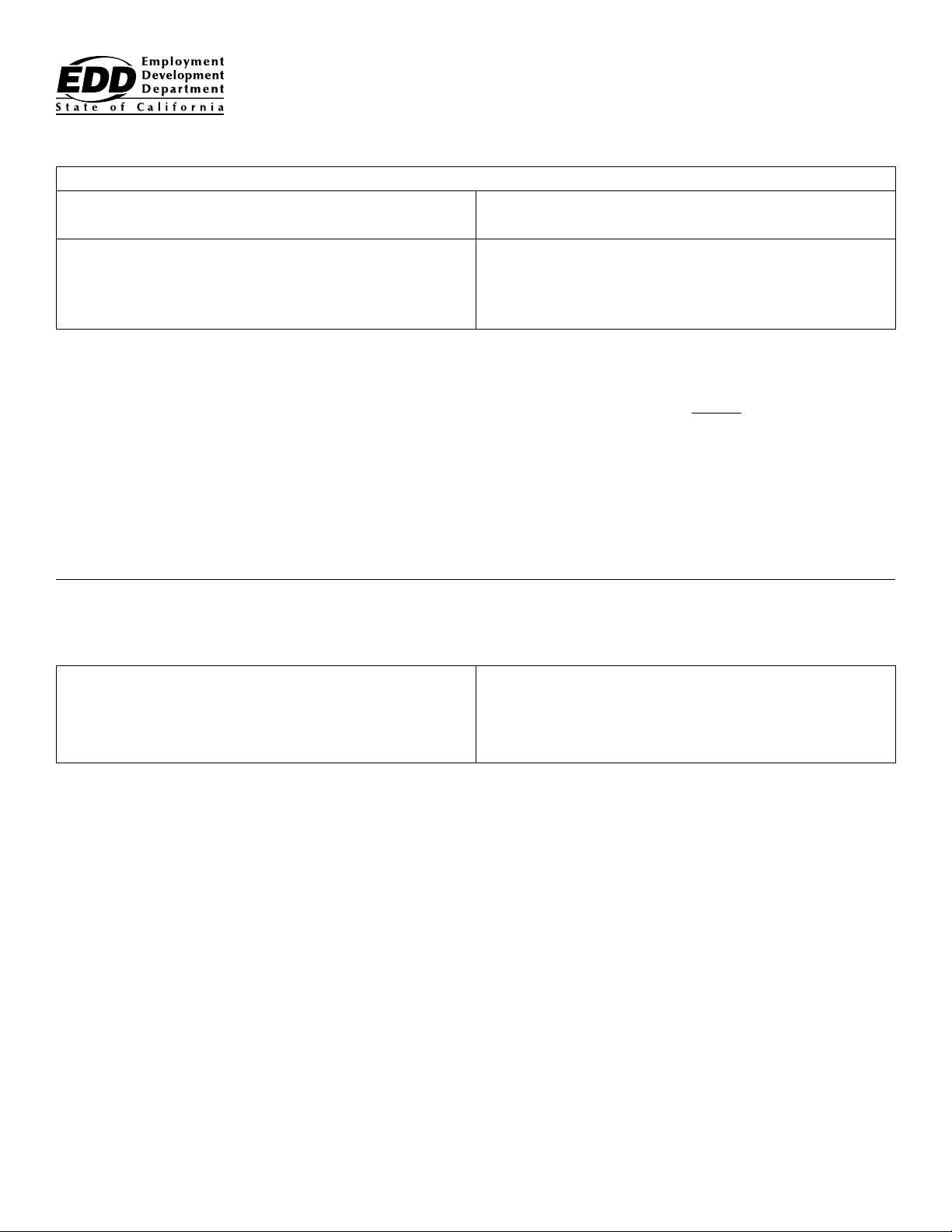

EMPLOYEE’S WITHHOLDING ALLOWANCE CERTIFICATE

Clear Form

Complete this form so that your employer can withhold the correct California state income tax from your paycheck.

Enter Personal Information

First, Middle, Last Name Social Security Number

Address

Filing Status

SINGLE or MARRIED (with two or more incomes)

City, State, and ZIP Code

MARRIED (one income)

HEAD OF HOUSEHOLD

1. Use Worksheet A for Regular Withholding allowances. Use other worksheets on the following pages as applicable.

1a. Number of Regular Withholding Allowances (Worksheet A) _______

1b. Number of allowances from the Estimated Deductions (Worksheet B, if applicable.) _______

1c. Total Number of Allowances you are claiming

2. Additional amount, if any, you want withheld each pay period (if employer agrees), (Worksheet C)

OR

Exemption from Withholding

3. I claim exemption from withholding for 2021, and I certify I meet both of the conditions for exemption. (Check box here)

OR

4. I certify under penalty of perjury that I am not subject to California withholding. I meet the conditions set

forth under the Service Member Civil Relief Act, as amended by the Military Spouses Residency Relief Act

and the Veterans Benefits and Transition Act of 2018. (Check box here)

Under the penalties of perjury, I certify that the number of withholding allowances claimed on this certificate does not exceed the number

to which I am entitled or, if claiming exemption from withholding, that I am entitled to claim the exempt status.

Employee’s Signature ____________________________________________________________ Date

Employer’s Section: Employer’s Name and Address California Employer Payroll Tax Account Number

PURPOSE: This certificate, DE 4, is for California Personal

Income Tax (PIT) withholding purposes only. The DE 4 is used to

compute the amount of taxes to be withheld from your wages,

by your employer, to accurately reflect your state tax withholding

obligation.

Beginning January 1, 2020, Employee’s Withholding Allowance

Certificate (Form W-4) from the Internal Revenue Service (IRS) will

be used for federal income tax withholding only. You must file the

state form Employee’s Withholding Allowance Certificate (DE 4)

to determine the appropriate California Personal Income Tax (PIT)

withholding.

If you do not provide your employer with a withholding certificate,

the employer must use Single with Zero withholding allowance.

CHECK YOUR WITHHOLDING: After your DE 4 takes effect,

compare the state income tax withheld with your estimated total

annual tax. For state withholding, use the worksheets on this form.

EXEMPTION FROM WITHHOLDING: If you wish to claim

exempt, complete the federal Form W-4 and the state DE 4. You

may claim exempt from withholding California income tax if you

meet both of the following conditions for exemption:

DE 4 Rev. 50 (1-21)

1. You did not owe any federal/state income tax last year, and

2. You do not expect to owe any federal/state income tax this

year. The exemption is good for one year.

If you continue to qualify for the exempt filing status, a new DE 4

designating EXEMPT must be submitted by February 15 each year

to continue your exemption. If you are not having federal/state

income tax withheld this year but expect to have a tax liability

next year, you are required to give your employer a new DE 4 by

December 1.

Member Service Civil Relief Act: Under this act, as provided by the

Military Spouses Residency Relief Act and the Veterans Benefits and

Transition Act of 2018, you may be exempt from California income

tax withholding on your wages if

(i) your spouse is a member of the armed forces present in

California in compliance with military orders;

(ii) you are present in California solely to be with your spouse;

and

(iii) you maintain your domicile in another state.

If you claim exemption under this act, check the box on Line 4.

You may be required to provide proof of exemption upon request.

CUPage 1 of 4(INTERNET)

The California Employer’s Guide (DE 44) (edd.ca.gov/pdf_pub_ctr/de44.pdf) provides the income tax withholding tables.

This publication may be found by visiting Payroll Taxes - Forms and Publications (edd.ca.gov/Payroll_Taxes/Forms_and_

Publications.htm). To assist you in calculating your tax liability, please visit the Franchise Tax Board (FTB) (ftb.ca.gov).

If you need information on your last California Resident Income Tax Return (FTB Form 540), visit the FTB (ftb.ca.gov).

NOTIFICATION: The burden of proof rests with the

employee to show the correct California income

tax withholding. Pursuant to section 4340-1(e) of

Title 22, California Code of Regulations (CCR) (govt.westlaw.

com/calregs/Search/Index), the FTB or the EDD may, by

special direction in writing, require an employer to submit

a Form W-4 or DE 4 when such forms are necessary for the

administration of the withholding tax programs.

DE 4 Rev. 50 (1-21)

Page 2 of 4(INTERNET)

PENALTY: You may be fined $500 if you file, with no

reasonable basis, a DE 4 that results in less tax being withheld

than is properly allowable. In addition, criminal penalties

apply for willfully supplying false or fraudulent information

or failing to supply information requiring an increase in

withholding. This is provided by section 13101 of the

California Unemployment Insurance Code (leginfo.legislature.

ca.gov/faces/codes.xhtml) and section 19176 of the

Revenue and Taxation Code (leginfo.legislature.ca.gov/faces/

codes).xhtml).

Loading...

Loading...